February 2022 - Monthly Market Update

/Monthly Update || February 2022

“When other investors are unworried, we should be cautious; when investors are panicked, we should turn aggressive.”

Opening Remarks

Greetings from Ikigai Asset Management¹ headquarters. We welcome the opportunity to bring to you our forty-first Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that already has and will continue to fundamentally change the world – continuing to create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

To that end, crypto prices moved lockstep with traditional markets in January as the US stock market got off to its worst start of the year ever in the first three weeks of 2022, before recovering some into month-end. A “Tightening Tantrum” was the culprit for this price action, as investors fled risk assets in response to a Fed that appears hell bent on stopping CPI inflation by any means necessary – a topic we dive into in detail below.

For years now I’ve offered the simple rule of thumb that “Bitcoin loves QE and detests QT”. That adage has been on display since November 30th when Powell said it was time to retire the word transitory during his Senate Banking Committee testimony. Since then, Bitcoin and crypto have been DownOnly and in January equities fell into the same trend.

In January as Bitcoin was trading tick-for-tick with the NASDAQ, crypto was also working through a stream of headlines on the regulatory and “government relations” front. See the Monthly Highlights below - lots of moving pieces here. There are potential outcomes on the regulatory front that would be significantly detrimental to the value proposition of crypto broadly. We’ve talked about that risk factor numerous times before here. In October 2021 I said –

That’s still how I see this setup. Bitcoin/Web3 will be on the ballot for mid-terms this year at the local, state and national level to a degree not previously seen. In the meantime, various interest groups are slugging it out over crypto behind the scenes in the swamp. This manifests in public as different government agencies fighting each other over who gets to regulate the space. It’s an opaque situation that’s difficult to get a clear view on, but the totality of what I’ve observed on this factor leads me to believe that the likelihood of a very bad outcome remains low. Yes, regulations will come, and the government is always going to want their taxes and want KYC/AML, but they seem willing to strike a balance that doesn’t stifle innovation too much and allows for the US to be in a position to benefit greatly from the rise of crypto and Web3. The exact timeline of how and when this plays out continues to be difficult to gauge and continuously sliding to the right, so we may not see as much progress on this broad front in 2022 as it might appear at the moment. Overall, it remains a dynamic situation and certainly worth paying close attention to.

While public crypto prices oscillate with macro and regulations, capital continues to plow into private crypto deals with a fervor unlike anything the venture landscape has ever seen in any industry. Crypto is the hottest sector on planet Earth right now, Fed rate hikes be damned. The push and pull of those two factors looks to be one of the defining features of crypto in 2022.

Invest

Ikigai is currently fielding interest from new investors globally. We are open to international investors and qualified accredited U.S. investors (including self-directed IRAs).

We accept new investors on the 1ˢᵗ and 15ᵗʰ of every month.

Contact us to see if you qualify.

January Highlights

Bill Miller Holds 50% of His Net Worth in Bitcoin

FTX Raises $2bn Venture Fund

FTX Raises $400mm Series C at $32bn Valuation from Temasek, Ontario Teachers, et al

FTX US Raises $400mm at $8bn Valuation from Softbank, et al

Blockdaemon Raises $207mm at $3.25bn Valuation from Tiger Global, et al

NFT Platform Autograph Raises $170mm Series B from a16z, et al

Smart Contract Platform Near Raises $150mm Ecosystem Fund

Swiss Digital Asset Banking Platform SEBA Raises $119mm Series C

Solana Wallet Phantom Raises $109mm Series B at $1.2bn Valuation

CoinTracker Raises $100mm Series A from Accel Partners, et al

Serum Raises $100mm from Tiger Global, et al

The Graph Protocol Raises $50mm from Tiger Global, et al

Solana NFT Platform Metaplex Raises $46mm

Paradigm and Sequoia Invest $1.15bn in Citadel Securities at $22bn Valuation

Apple CEO Tim Cook “Sees a Lot of Potential in Metaverse, Investing Accordingly”

Nike Hiring Director of Metaverse

Cash App Begins Offering Lightning Network Access to Users

Google Hires Former PayPal Executive to Run Payments Division, Push into Crypto

Twitter Blue Launches Feature for Users to Display NFTs

Facebook and Instagram Preparing Feature to Allow Users to Display NFTs

Robinhood Begins Testing Crypto Wallet

Crypto Execs from CMS Holdings, Framework Ventures, FTX, Skybridge, et al Launch $20mm PAC to Deploy Towards Crypto Lobbying in 2022

Presidents Working Group Plans Executive Order on Crypto for February

SEC Proposes Rule with Wide-ranging Language That Could Be Adversely Applied to Numerous Crypto Projects

Fed, Treasury Warm to Private Stablecoins While Still Open to Digital Dollar

US Representative Tom Emmer Introduces Bill Prohibiting Fed from Issuing CBDC Directly to Individuals

Gary Gensler Appoints Senate Aide Corey Frayer as Senior Advisor on Crypto

CFTC Fines Polymarket $1.4mm for Unregistered Swaps

Russia Calls for Full-scale Ban on Crypto Trading, Mining and Payments, Then Walks Back Statement

China Plans to Legalize NFTs and Prepares Separate Laws from Crypto

Former CFTC Chair Chris Giancarlo Joins Coinfund Board of Directors

Mayor of Rio De Janeiro Moves 1% of City Treasury into Bitcoin

Facebook Stablecoin Project Diem Winds Down, Prepares for Asset Sale

Crypto.com Has 400 Accounts Hacked for $19mm

Crypto Trading Firm Tantra Labs Goes Bankrupt After GBTC Discount Widens

American Express Considering Allowing Points to Be Redeemed for Crypto

| Asset Class | Jan | Q4-21 | Dec | Nov | Oct | Q3-21 | Q2-21 | Q1-21 | 2021 | 2020 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | -17% | 6% | -19% | -7% | 40% | 25% | -41% | 103% | 60% | 303% | BTC |

| NASDAQ | -9% | 11% | 1% | 2% | 8% | 1% | 11% | 2% | 27% | 48% | QQQ |

| S&P 500 | -5% | 11% | 4% | -1% | 7% | 0% | 8% | 6% | 27% | 16% | SPX |

| Total World Equities | -5% | 5% | 3% | -3% | 5% | -2% | 6% | 6% | 16% | 14% | VT |

| Emerging Market Equity | 0% | -3% | 0% | -4% | 1% | -9% | 3% | 4% | -5% | 15% | EEM |

| Gold | -2% | 4% | 3% | -1% | 1% | -1% | 3% | -10% | -4% | 25% | GLD |

| High Yield | -3% | -1% | 2% | -1% | -1% | -1% | 1% | 0% | 0% | -1% | HYG |

| Emerging Market Debt | -3% | -1% | 1% | -2% | 0% | -2% | 3% | -6% | -6% | 1% | EMB |

| Bank Debt | -1% | 0% | 1% | -1% | 0% | 0% | 0% | -1% | -1% | -2% | BKLN |

| Industrial Materials | 3% | 8% | 7% | -2% | 3% | 2% | 8% | 8% | 29% | 16% | DBB |

| USD | 1% | 1% | 0% | 2% | 0% | 2% |

-1% | 4% | 6% | -7% | DXY |

| Volatility Index | 44% | -26% | -37% | 67% | -30% | 46% |

-18% | -15% | -24% | 66% | VIX |

| Oil | 15% | 3% | 13% | -16% | 9% | 5% | 23% | 23% | 64% | -68% | USO |

Source: TradingView. As of 1/31/22.

The Fed Who Cried Tightening

It wasn’t even six months ago that the Fed was projecting one rate hike at best in 2022. In the last two months of 2021, the chorus of Fed officials and Wall St executives began “The Great Jawboning” of accelerating tightening to fight inflation. Futures markets went from pricing in one rate hike in 2022 to three or four before the New Year rang and a month later, we’re sitting at five or six hikes in 2022.

Source: CME. As of 1/31/22.

But it’s not just rate hikes starting in March we’re talking about and we’re way past the tapering discussion. Just this month, balance sheet reduction via principal repayment rolloff was put on the table. At this point, most Wall St research expects balance sheet rolloff to begin in July at $50bn/month, quickly ramping up to $100bn/month. There have even been whispers of not just balance sheet runoff but actual selling of assets. So yeah, that escalated quickly.

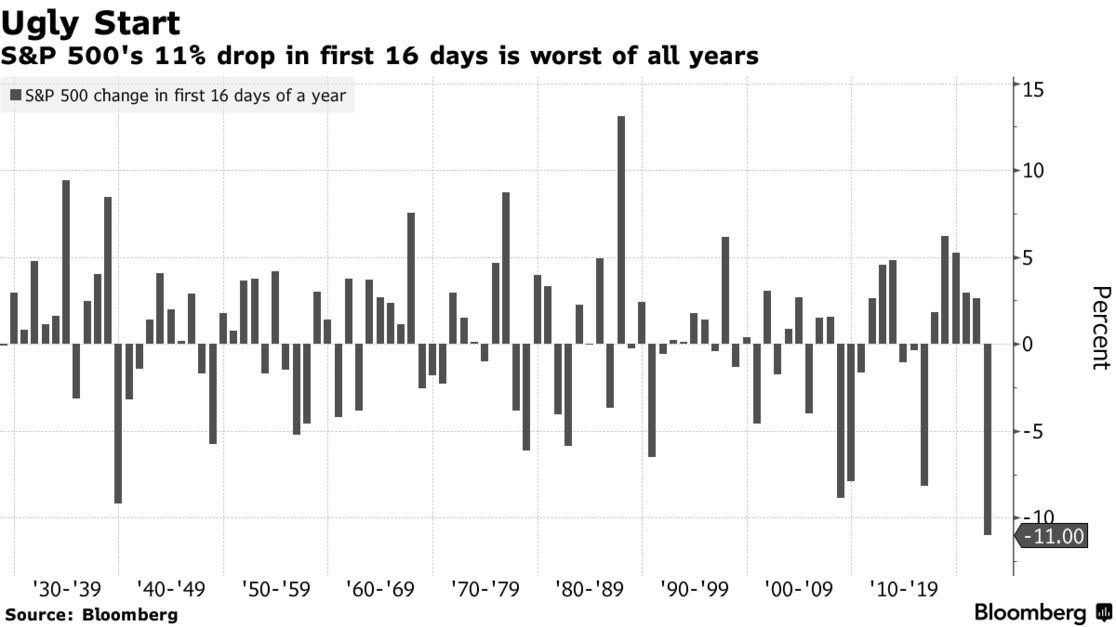

Equities responded in kind. SPX had its worst start ever through 16 days -

Source: Bloomberg. As of 1/24/22.

NASDAQ fared worse, down more than 16% at the lows of the month.

Source: TradingView. As of 1/31/22.

I highlighted Q4-18 on the chart above as a somewhat comparable period from a macro perspective. The Q4-18 dumpster fire for risk assets was about Fed tightening back then too, except the Fed Funds was at 2.2% then, not zero like it is currently. And the Fed was nine months into shrinking the balance sheet at $50bn/month, instead of still doing QE like they are currently. So the analogy of the drug addict may hold to understand this setup – when you first start using hard drugs, just a little bit gets you really high. After a decade of hard drug use, it takes a huge amount just to feel a little buzz, and if you try and wean off just a little it’s gonna hurt bad. That’s where the Fed finds itself.

There are numerous considerations to factor in when assessing this situation – what has the Fed done historically? What can they do? What are they incentivized to do? Thus, what are they likely to do?

What Has the Fed Done Historically?

Historically the Fed has jawboned more hawkishness than they actually delivered. Granted, we’ve only had one tightening cycle since The Greatest Monetary Experiment in Human History (QE while running increasingly larger deficits on top of increasingly untenable debt levels). And you can certainly make the case that comparing the current setup to any period prior to T.G.M.E.I.H.H. is a fool’s errand. If that’s the case then we have Q4-18 alone to compare as a period of “overtightening policy error”. Looking back, the stress was bad but not all THAT bad in Q4-18.

BBB spreads widened some.

Source: TradingView. As of 1/31/22.

CCC widened a bit more.

Source: TradingView. As of 1/31/22.

HYG declined a sharp 8% before bouncing into year-end 2018.

Source: TradingView. As of 1/31/22.

The new issuance market for high yield in Q4-18 did seize up, including a very rare zero issuances in December 2018, which likely played a part in the Fed’s decision to pause. But overall, financial conditions only saw mild tightening.

Source: TradingView. As of 1/31/22

Perhaps the Fed got above 2% on the Fed Funds and the market just told them that was enough, and they agreed?

Source: FRED. As of 1/31/22

Without a doubt, political pressure played a significant role in Q4-18, as it does today, just in a different form.

What Can They Do?

So that’s a bit about what they have done historically. What about what they can do now?

They can hike 25bps every quarter starting in March. They could hike every month or every other month but they haven’t hiked more than once a quarter since 2006. They could in theory hike 50bps at a meeting, but they’ve never done that.

They can roll off the balance sheet at $50bn/month like 2018 or accelerate it further, perhaps to $100bn/month. Those potential trajectories are shown below.

Source: Reuters. As of 1/26/22.

There are two new tools in the Fed’s toolkit this time around that might allow them to roll off the balance sheet faster than they otherwise would – the Standing Repo Facility and the Reverse Repo Facility. In short, these mechanisms allow for a more fluid exchange of short-term liquidity between the Fed and large banks. Reverse repo balances currently stand at more than $1.5tn, suggesting a faster pace of tightening may be possible without disturbing short-term funding markets.

Source: Reuters. As of 1/26/22.

What Are They Incentivized to Do?

This is where it gets interesting. I’ve long been a big fan of incentive structures. It’s a form of applied game theory. If you want to understand why someone is doing something or not doing something, look at what they’re incentivized to do, or not do. When it comes to potential Fed actions, they have a unique set of incentives. First off, none of these officials are elected. They are appointed and re-appointed. They have political allegiances. Specifically when it comes to Powell, he is a Democrat that is beholden to former Fed Chair and current Treasury Secretary Janet Yellen. It might as well be Yellen running the Fed too, because Powell takes his orders from her.

How are things going for Democrats at the moment?

Not great for Biden.

Source: Pewresearch.org. As of 1/24/22.

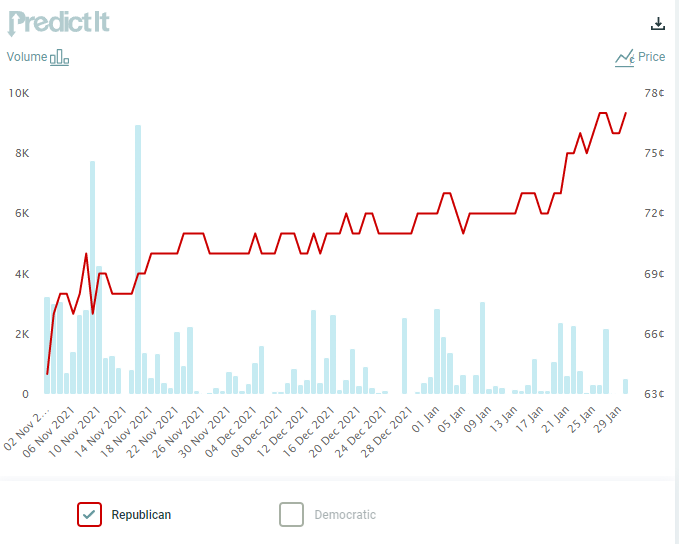

Not great for the House mid-terms.

Source: Predictit.org. As of 1/30/22.

And not great for the Senate mid-terms either.

Source: Predictit.org. As of 1/30/22.

So the Democrats need a gameplan for this November, and they need one fast. Polls are telling them voters care about inflation. The Fed is the throttle by which to control inflation, and Democrats have significant influence over the Fed, so they wield that influence. There’s an incentive structure.

In order to gauge this next part, you need to have some view on the near-term trajectory of CPI inflation. Y/Y CPI growth jumped from 2.6% in March 2021 to 4.2% April 2021 due to base effects. So when April 2022 comes around, that same base effect works in the opposite direction, showing a decline in Y/Y inflation growth even if M/M growth stays at the currently elevated levels. If you assume M/M CPI growth returns to a level halfway between 1) the three years prior to the pandemic and 2) the post-pandemic crash (representing some sustained higher inflation), the September 2022 print (last one before mid-terms) would be ~5% Y/Y, down from 7% currently. Will that be enough for the Democrats mid-term playbook? Possibly not. Which makes The Great Jawboning all that much more sincere! They really want CPI to chill out. But do they want it to chill out so much that it brings GDP growth rate to a halt? No they don’t. Do they want CPI to chill out so much the NASDAQ goes -23% from the top like Q4-18? Honestly yeah they’d probably take it, but much lower than that for very long is probably a no-go. The incentives aren’t in place to force an outcome like that. Boomers are their constituents, and they own all the stuff. Influential Boomers want all their stuff to be expensive.

Source: Federal Reserve. As of 2019

Is the Fed really incentivized to torch financial markets and in turn the economy while 10,000 Boomers hit retirement age every day between now and 2030? Seems unlikely. Incentives aren’t there. You could talk about those analog-native folks being replaced in the workplace by digitally-native folks and what that means for crypto, but that what be a separate point entirely. And you could talk about the wealth transfer that occurs as those Boomers pass along assets to the next generation and what that means for crypto, but that would be a separate point still.

For now, the worst outcome for Democrats come November would be stubbornly high inflation with a stock market down 20% YTD and leading economic indicators flashing a recession.

Speaking of flashing recessions, great segue into the Eurodollar futures curve that has nearly inverted. This was the same indicator that told the Fed it was wrong about tightening in summer 2018, months before the Q4-18 mess and the following dovish capitulation.

Source: TradingView. As of 1/31/22.

The Fed is incentivized to be seen as having fought inflation and won. They are not incentivized to make a beeline for a market crash and push into a recession. So the Fed is incentivized to thread the needle. To Goldilocks it. Not too hot, not too cold. This is exactly what they did for years after the Financial Crisis. Goldilocks the three phases of QE and the Operation Twist. Goldilocks the rate hikes. Goldilocks the balance sheet runoff. Until they couldn’t Goldilocks it anymore and they threw in towel in January 2019. That’s what they’re incentivized to do and that’s what they can do and that’s what they’ve done before.

Thus, What Are They Likely to Do?

When you add it all up, the Goldilocks outcome seems most likely. If that’s true, perhaps we’re not currently comparable to Q4-18 but actually late 2015/early 2016 – the exact time the Fed hiked for a second time to 75bps (after staying flat at 50bps for a year). Amazingly, the NASDAQ had a very similar 16% pullback on increased rate hikes before bottoming and heading much much higher before the Q4-18 rollover.

Source: TradingView. As of 1/31/22.

With the aforementioned cash sloshing around the repo facilities and plenty of dry powder domestically and abroad looking to store their wealth in the US stock market, there’s reason to believe US equities and in turn crypto, can be somewhat resilient in the face of a Goldilocks tightening scenario. This “6 or 7 hikes” in 2022 is bananas.

Source: Yahoo Finance. As of 1/14/22

Dimon is a joker. I’ll place my bets with The Bond King.

Source: @zerohedge. As of 1/11/22.

The setup for this “less-hawkish-than-jawboned” Goldilocks outcome doesn’t really start for another few months because of those CPI base effects. And last week Powell certainly didn’t seem to be fussed at all about the market dump thus far YTD. So the next couple months could be choppy for equities and thus choppy for crypto. But the setup is there for a very tradeable rally in late spring/summer and potentially beyond. Should we prove to be in Q4-15 rather than Q4-18 for macro, new ATH’s in equities are on deck for later this year, just in time for mid-terms. If that were to occur, it would be difficult for me to imagine crypto not rallying significantly.

Market Update – Liquid Crypto Asset Investing

| Symbol | Jan | Q4-21 | Dec | Nov | Oct | Q3-21 | Q2-21 | Q1-21 | 2021 | 2020 | 2019 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| BTC | -17% | 6% | -19% | -7% | 40% | 25% | -41% | 103% | 60% | 303% | 92% |

| ETH | -27% | 23% | -20% | 8% | 43% | 32% | 19% | 160% | 399% | 469% | -3% |

| XRP | -26% | -10% | -17% | -10% | 20% | 31% | 23% | 161% | 278% | 14% | -45% |

| BCH* | -32% | -13% | -23% | -5% | 21% | -6% | -11% | 45% | 6% | 71% | 30% |

| EOS | -23% | -23% | -24% | -13% | 18% | -5% | -14% | 85% | 17% | 1% | 0% |

| BNB | -27% | 32% | -18% | 19% | 35% | 28% | 0% | 708% | 1269% | 172% | 123% |

| XTZ | -20% | -28% | -21% | -13% | 4% | 100% | -37% | 142% | 116% | 49% | 192% |

| XLM | -25% | -4% | -20% | -10% | 34% | -1% | -31% | 220% | 108% | 184% | -60% |

| LTC | -25% | -4% | -30% | 8% | 25% | 6% | -27% | 58% | 17% | 202% | 36% |

| TRX | -22% | -16% | -22% | -5% | 13% | 31% | -26% | 244% | 181% | 101% | -29% |

| Aggregate Mkt Cap | -20% | 13% | -17% | 0% | 36% | 33% | -23% | 146% | 186% | 301% | 51% |

| Aggregate DeFi* | -27% | 29% | -7% | 6% | 31% | 64% | -27% | 339% | 581% | 1177% | 77% |

| Aggr Alts Mkt Cap | -22% | 19% | -15% | 5% | 33% | 40% | 1% | 246% | 479% | 274% | -1% |

Source: CoinMarketCap. As of 1/31/22. BCH includes SV. Aggregate DeFi from Coingecko.

Driven by macro tapering fears, Bitcoin was down 17% in January, it’s worst start since 2018. Alts broadly fared worse, some much worse. You can see from the chart below BTC lost several major areas of support this month in DownOnly fashion before bouncing from deeply oversold levels at a major volume node, short of testing the yearly range lows at $29k.

Source: TradingView. As of 1/31/22.

At the low on January 20th, BTC was -51% in 2 ½ months with no bounce, and bulls stepped in. Note the volume profile at the low – a good chunk of coin changed hands sub-$37k. At the moment, after this recent bounce, BTC is now retesting a prior point of control and coming into this steep downtrend. Given the chop I expect in the coming months for macro, I would be surprised if BTC teleports a lot higher and stays there. We may chop heavily in the $29k-$45k range for the next few months. I don’t think BTC necessarily HAS to retest the yearly range lows sub-$30k, but it wouldn’t surprise me.

ETHBTC is in a tricky spot - failing into resistance at a major point of control spanning back more than four years and barely hanging on to a trendline that frankly may no longer be valid.

Source: TradingView. As of 1/31/22.

It’s still my base case ETH will act as beta to BTC, so as BTC goes, so goes ETHBTC. ETH 2.0 will be a strong narrative later on this year, but if BTC chops heavily with equities, ETHBTC likely chops heavier. Honestly, in a vacuum price action since May looks distributive at the moment. I can’t help but wonder if we’re seeing our old friend Wyckoff. If BTC were to test sub-$30k, this ETHBTC distribution could certainly play out.

Source: Stockcharts and TradingView. As of 1/31/22.

The Layer1 wars got pretty ugly in January with last year’s darlings SoLunAvax taking the brunt of the damage.

Source: TradingView. As of 1/31/22.

Both Luna and Solana had significant problems in January, albeit of differing natures. Luna got wrapped up in a rather scandalous dump of a next-gen ponzi project called, I shit you not - Magic Internet Money. You can read more about the situation here and here. I do not have a deeply informed view of this situation at the moment but my layman’s view makes me think there’s real “peg risk” there. I don’t know how to price that risk and when I run across big, hard-to-price risks like that in crypto I have historically just had a tendency to stay away.

Solana went through a different sort of headache in January. It experienced degraded blockchain performance as transaction throughout was bogged down significantly for an extended period of time. This situation was well-covered on Twitter by knowledgeable people. SOL price went down a lot while this was ongoing and at the low on January 21st SOL was -52% MTD and down 69% from early November highs. No one at Ikigai has the distributed systems expertise to accurately assess this problem and its “fixability”. I talk to some people that do though. And the leaders of the Solana project talked a lot about the situation openly. So you can listen to the folks that know a lot and make a call based on what they say. You can also look at the teams and assess their capabilities. While the FTX/Alameda crew get a lot of airtime in this regard (as they should), another organization that is deeply committed to the Solana ecosystem often gets overlooked –

Source: The Block. As of 1/21/22.

Jump Trading, if you haven’t heard of them, have an impeccable reputation in the traditional markets. They are one of the most successful HFT firms of all time. Jump has been around in the crypto markets for many years, mostly in “market making”, but over the last 18 months have massively ramped up their commitment to investing in and helping build new crypto projects. They are all-in crypto. Jump’s VC arm has been one of the most active investors in the space in the last six months, and it’s clear which Layer 1 is their main horse. When I look at the team of builders at Solana, FTX/Alameda and Jump, that’s a group that I have about as high a degree of confidence in as possible in this space. This bodes well for Solana’s long-term future.

One more factor worth mentioning – the NFT Summer we experienced last year is looking less and less like a flash in the pan. Note OpenSea volumes below.

Source: OpenSea. As of 2/1/22.

OpenSea isn’t the only NFT marketplace doing major volume. January saw the emergence of a new liquidity mining driven NFT marketplace called LooksRare. LooksRare is wash trading by design, and while long term success of the project looks unlikely, it’s put up some big numbers. So have other NFT marketplaces.

Source: DappRadar. As of 2/1/22.

Closing Remarks

Rate hikes. Repo facilities. Mid-terms. It’s gonna be a macro year for Bitcoin and thus, crypto. But that’s only to speak of prices. The macro will matter much less or not at all for the pace of evolution of projects in the crypto ecosystem. That will continue moving at a breakneck pace regardless of whether the Eurodollar futures curve inverts in 2022. Whether BTC is +50% or -50% in 2022 will be a meaningfully macro analysis, but it will only have marginal influence over the pace of permanent capital flooding into crypto this year. That number is going to be big either way.

All the pieces are in place for this Cambrian Explosion of innovation to accelerate to a degree never previously seen. Bitcoin will continue pushing for acceptance as pristine collateral at the global financial system level. Layer 1’s will innovate to increase throughput. They will fight for popular dApps to drive network activity. Those dApps themselves will innovate on multiple fronts to attract users. Metaverse, P2E and gaming will be full steam ahead all year. DAOs will continue their early stages of innovation “in production”. The “middleware” to hold all this together will continue to innovate behind the scenes. Web3 is starting to win the battle against Big Tech for top talent, a crucial component for the future of innovation for the space in the years to come.

Here at Ikigai we will be innovating in our own ways as well. “What got us here won’t take us there”. Generating attractive risk-adjusted returns in an ethical manner is our core value proposition to our investors. How exactly you go skin that cat is a wide open question – there’s no playbook for this wild world of crypto investing. We knew from the beginning, nearly four years ago, that we would need to be agile in our deployment of capital. There remains ample opportunity for 1) beta value creation; 2) alpha value capture; and 3) negative alpha value destruction. We are focused on gaining exposure to 1 & 2 while avoiding 3 and making the world a better place along the way. We appreciate you taking that journey with us.

“We’re fool’s whether we dance or not, so we might as well dance.”

– Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2021 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS