July 2022 - Monthly Market Update

/Monthly Update || July 2022

“When risk bearing doesn’t work, it really doesn’t work, and people are reminded what risk’s all about.”

Opening Remarks

Greetings from Ikigai Asset Management¹ headquarters. We welcome the opportunity to bring to you our forty-sixth Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that already has and will continue to fundamentally change the world – continuing to create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

To that end, June was the worst month for Bitcoin since September 2011, down 38%. Q2 was the second worst quarter ever, behind only Q3-11. That price action came on the back of very challenged macro and historically bad micro. The price crash was the result of the largest Shadow Leverage Daisy Chain (“SLDCU”) unwind ever: starting with Terra Luna, metastasizing to Celsius, crescendoing with the Madoff-style blowup of Three Arrows Capital, and then knocking-on to blow up or significantly damage virtually every borrow/lending business in crypto, multiple exchanges and hundreds of projects and funds. It was the largest nominal blowup in crypto history. This was a risk I’ve been talking about for well over a year. That risk came to fruition in the last two months and wiped more than a trillion of market cap in the process.

The exact extent of the damage remains unclear at the moment. Millions of retail depositors to Celsius, Babel, and possibly other centralized borrow/lending platforms are likely stuck and impaired. Lawsuits stemming from the last two months will likely drag on for many years. The equity of dozens of crypto companies is wiped out or severely impaired.

$20k BTC in July 2022 is certainly not the outcome I would have guessed and not the outcome any of us were hoping for, but here we are. Ikigai is not in any way deterred and thankfully we have navigated the last few months reasonably well. This asset class is still incredibly attractive, and this technology still has a tremendous opportunity to make the world a better place. That is why we are here, and we are very well-positioned for the coming quarters and years. Frankly, I can’t believe this market is giving me another shot on goal from $20k and $1k but that’s where we are and I’m salivating at the opportunity.

I don’t know what price is going to do in the near term. Crypto is dealing with bad macro and bad micro right now. This is the worst macro backdrop Bitcoin has ever experienced, except for maybe a few weeks in March 2020 before the Fed ripped $3tn of QE in six weeks. On top of that, the micro for crypto is very challenged in the near term, although the worst may be behind us or nearly behind us at the moment.

Many crypto funds over the years have lost enormous percentages of their AUM, but the Three Arrows Capital blowup is nearly unimaginable in its scale and surprise. These were guys that were in the Top 10 of everyone’s list for the best investors in crypto. 3AC was a group that virtually everyone strived to be more like, at least from an investing perspective. It felt like they were playing a different game than the rest of us. The strength of 3AC’s reputation made us all examine how we could be better at our jobs. It was that reputation that allowed them to leverage their collateral to unthinkable levels and blow up in movie-worthy fashion. It now appears they have liabilities which exceed their assets by billions of dollars and there is a good chance criminal charges will be levied against them.

It is an incredible fall and I’d be lying if I said it hasn’t messed with my head some. Ikigai has been at this for 3 ½ years and throughout that time I’ve often found myself thinking we’re doing an “okay” job at generating attractive risk-adjusted returns for our investors. I will hear about this firm or that firm that crush our returns and the FOMO is real, I don’t care how Zen you are. But then we get into situations like the one we find ourselves in and I am reminded that “through-cycle” returns really are crucial. Producing top decile returns in the bull market and blowing up in the bear is not a good outcome for investors.

For our investors, those that joined us in 2019 have outperformed BTC by hundreds of percent; those that joined us in 2020 have outperformed by ~100%; and those that joined us since 2021 have still outperformed by meaningful double digits. Bitcoin price is flat since November 2020 and we’ve generated ~70% returns net of our fees. It’s not the outcome any of us were playing for, but we think in a vacuum it’s a fine outcome from a returns perspective. We’re currently sitting on a lot of cash, as we have been for several months, watching closely for signs of a cyclical bottom, or at least a playable rally.

The market is fraught with risk right now, but prices are very depressed. Where the industry as a whole goes from here is somewhat unclear. While Bitcoin the network has performed perfectly, Bitcoin the asset faces a narrative challenge. It did not work as an inflation hedge. It did not work as an uncorrelated asset. It did not work as collateral. Within crypto, Bitcoin did not act as a safe haven, as Bitcoin Dominance remains only slightly above its all-time lows. The “Toxic Bitcoin Maximalist” crowd has turned to bitter infighting and lashing out in a way that is damaging to Bitcoin.

Retail-focused centralized borrow/lending platforms may never recover, at least not without significant regulation. While leverage will almost certainly never leave the crypto market entirely, the nature of leverage will change. The duration mismatch inherent in the retail depositor (on open-term length) / institutional borrower (with fixed-term length) business model is likely now apparent enough that it will never happen again to the same extent. Duration mismatches have blown up hundreds of financial firms over the last 100 years. Crypto just had its own Lehman moment – apparently we had to learn that one the hard way. More institutionally focused, centralized borrow/lending platforms will likely remain, albeit with tighter risk parameters. It is now clear that the manner and degree of communication across the largest borrow/lending platforms was not as high as you might expect or hope for with firms that had hundreds of millions of dollars of counterparty exposure to a single firm. I would guess this will change going forward, hopefully enough to prevent the same sort of thing from happening again.

It remains to be seen how the DeFi sector will emerge from this carnage. In a lot of ways, the value proposition for DeFi was on display the last two months. Things generally worked like they were supposed to, even with Terra Luna! To be clear, the SLDCU certainly had DeFi leverage closely intertwined with it, but DeFi was NOT the cause of the SLDCU. To the contrary, it was centralized borrow/lending platforms, with their inherent opacity, that enabled the undercollateralized and uncollateralized lending that caused the SLDCU. To be sure, leverage in DeFi was high. But it was all collateralized, and when those smart contracts hit liquidation levels, the protocols executed the liquidations to save the collateral, mostly as designed. Everything happened on-chain.

You could imagine a crypto world (or dare I say, real world) where all borrow/lending happened transparently in DeFi. All borrowing was overcollateralized, and if you hit your liquidation level due to price declines, your collateral was liquidated to save the lender. This is actually the foundational principal for centralized Perpetual Swaps, albeit with exchange counterparty risk, instead of the smart contract risk in DeFi.

It might be wishful thinking to assume the opacity of the centralized borrow/lending market is about to go away forever. These things move in pendulums and greed has an incredible W/L record. So opaque leverage in crypto will likely tighten for time (it already has significantly), but eventually it will likely widen back out. That’s just the nature of these things. Do I believe one day, years or decades from now, we will achieve the transparency that an entirely DeFi financial world promises? Yeah maybe, it could happen. It would certainly be good for humanity, to prevent these sorts of things from happening over and over again for thousands of years. I’d like to work on making that a reality. But first we gotta stop tripping over our own two feet.

Invest

Ikigai is currently fielding interest from new investors globally. We are open to international investors and qualified accredited U.S. investors (including self-directed IRAs).

We accept new investors on the 1ˢᵗ and 15ᵗʰ of every month.

Contact us to see if you qualify.

June Highlights

Three Arrows Capital Blows Up Madoff-Style, Likely Committed Crimes, Knock-On Effects Severely Damage Many Large Crypto Companies, Many Billions Lost

Celsius Halts Withdrawals on June 13th, Engages with Restructuring Legal and Financing Teams, Likely Heading to Bankruptcy, Customer Assets Likely Stuck and Impaired

BlockFi Loses Hundreds of Millions on Bad Loans to 3AC and Others, Receives Emergency $250mm Loan from FTX, FTX Likely Acquiring Entire Company For $275mm Assumption of Debt

Publicly Traded Crypto Platform Voyager Digital Nearly Blows Up on 3AC Contagion, Receives Emergency $500mm Loan from Alameda Research, Alameda Likely Acquiring Controlling Stake

Babel Finance Blows Up From 3AC Contagion, Loses A Billion or More

SEC Rejects Grayscale Spot Bitcoin ETF, Grayscale Files Suit Against SEC the Same Day

Crypto Exchange CoinFlex Loses $47mm on Bad Loan to Roger Ver, Issues Token with Claim to Future Recovery

CEO and CFO of Compass Mining Resign

Solana Announces Plan for Smartphone

MicroStrategy Buys $10mm of Bitcoin

Ronaldo Partners with Binance for NFT Collection

PayPal Enables Transfer of BTC, ETH, BCH and LTC to External Wallets

Binance VC Arm Binance Labs Raises $500mm Venture Fund

London VC Firm Felix Capital Raises $600mm Web3 Fund

NFT Marketplace Magic Eden Raises $130mm at $1.6bn Valuation

FalconX Raises $150mm at $8bn Valuation

PrimeTrust Raises $105mm Series B

US Prosecutors Charge OpenSea's Nathaniel Chastain with Insider Trading

CFTC Claims Gemini Lied to Regulators About Giving Market Maker Rebates

DOJ Publishes Response to Biden Executive Order on Digital Assets

Senators Lummis and Gillibrand Announce 69-page Responsible Financial Innovation Act, a Bill Creating Thorough Regulatory Framework for Digital Assets

Coinbase Cuts 18% of Employees

ProShares Launches Short Bitcoin ETF

NYDFS Issues Stablecoin Guidance

DeFi Protocols Generally Perform Well During Market Stress

Coinbase Introduces Increased KYC For Outgoing Transactions in Some Jurisdictions

Nexo Offers to Acquire Qualifying Assets from Celsius

Citadel Partnering with Virtu to Build Crypto Trading Marketplace

| Asset Class | June | May | Apr | Q2-22 | Q1-22 | YTD | Q4-21 | Q3-21 | Q2-21 | Q1-21 | 2021 | 2020 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | -38% | -16% | -17% | -57% | -2% | -57% | 6% | 25% | -41% | 103% | 60% | 303% | BTC |

| NASDAQ | -9% | -2% | -14% | -23% | -9% | -30% | 11% | 1% | 11% | 2% | 27% | 48% | QQQ |

| S&P 500 | -8% | 0% | -9% | -16% | -5% | -21% | 11% | 0% | 8% | 6% | 27% | 16% | SPX |

| Total World Equities | -9% | 0% | -8% | -16% | -6% | -21% | 5% | -2% | 6% | 6% | 16% | 14% | VT |

| Emerging Market Equity | -6% | 1% | -6% | -11% | -8% | -18% | -3% | -9% | 3% | 4% | -5% | 15% | EEM |

| Gold | -2% | -3% | -2% | -7% | 6% | -1% | 4% | -1% | 3% | -10% | -4% | 25% | GLD |

| High Yield | -7% | 1% | -5% | -11% | -5% | -15% | -1% | -1% | 1% | 0% | 0% | -1% | HYG |

| Emerging Market Debt | -6% | 0% | -7% | -13% | -10% | -22% | -1% | -2% | 3% | -6% | -6% | 1% | EMB |

| Bank Debt | -4% | -2% | -1% | -7% | -1% | -8% | 0% | 0% | 0% | -1% | -1% | -2% | BKLN |

| Industrial Materials | -15% | -3% | -8% | -25% | 16% | -13% | 8% | 2% | 8% | 8% | 29% | 16% | DBB |

| USD | 3% | -1% | 5% | 7% | 3% | 10% | 1% | 2% |

-1% | 4% | 6% | -7% | DXY |

| Volatility Index | 9% | -21% | 64% | 40% | 19% | 67% | -26% | 46% |

-18% | -15% | -24% | 66% | VIX |

| Oil | -6% | 11% | 4% | 8% | 36% | 48% | 3% | 5% | 23% | 23% | 64% | -68% | USO |

Source: TradingView. As of 6/30/22.

Macro and Blockchain in Focus

Guest Author: Ikigai Principal Hans Hauge

Many of our readers are familiar with the work of Lyn Alden, who has presented a unique and compelling look at macro drivers with her newsletters, charts and interviews. In the most recent newsletter, there was one chart in particular that caught my attention.

Source: https://www.lynalden.com/june-2022-newsletter/.

Shown above is ~13 years of data comparing the Fed’s balance sheet and the Wilshire 5000 equity index. The reason I find this chart so interesting is that it encapsulates a very important concept in a simple image - “money printer go brrrr.” When the Fed’s balance sheet is on the rise, so are equity prices. And when the Fed’s balance sheet is flat or being contracted, equity prices tend to fall or just chop. So is it any coincidence that the latest balance sheet roll-off has coincided with the latest decline in equities and in turn produced a crypto winter?

Source: FRED.

In the same way we look to macroeconomic precedent from the past to inform us on some potential outcomes for equities, I believe that we can use data from the blockchain to give us some color on what crypto is going through. To do this, we’re going to look at a few of my favorite blockchain-based models that focus primarily on Bitcoin, due to its scale and the fact that Bitcoin has the longest-running historical data to analyze.

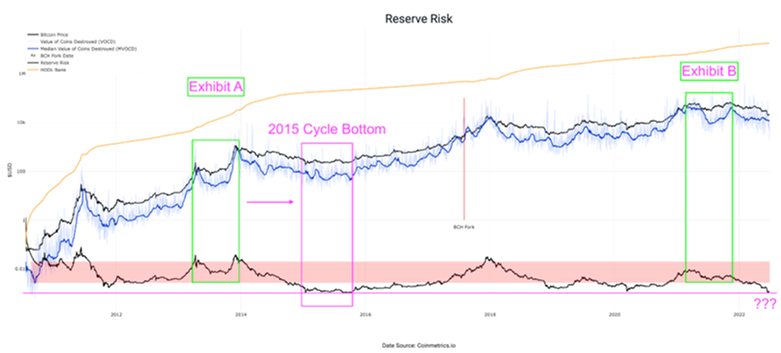

In May of 2019, I introduced the Reserve Risk model via the Valuation Depot on our Kana and Katana blog. The purpose of the model was to identify cyclical tops and bottoms in the market in order to improve entry and exit timing. Under the hood, the model used an esoteric concept called “Bitcoin Days Destroyed” to categorize market participants. Put plainly, if the most experienced and well-capitalized players are cashing out near a top, you might want to think about doing the same. If you flip this on its head, whales scooping up coins and putting them into long-term storage after a large decline in price could (and has in the past) signaled a cyclical bottom, which makes for an attractive entry point.

Source: Ikigai, CoinMetrics.

It’s interesting to note that since this model was created in 2019, the math hasn’t changed. The black line at the bottom is the Reserve Risk. The lower this line is, the better of an entry point you have, historically speaking. As you can see, the Reserve Risk hasn’t measured this low since 2015. And it’s to that year I would like to draw your attention because I see several similarities between that year and 2022. In 2013 we had two tops for the Bitcoin price - one in the mid-$100 range and the next just over $1,000. 2014 was a long bear market for Bitcoin, and in 2015 BTC found its floor and bounced off it a couple of times at or around $200. Fast Forward to 2021 and again Bitcoin formed a double top, even though it was somewhat less pronounced. 2022 has been bearish, and as we can see the Reserve Risk levels are now back where they were in 2015 when the price was around $200; only now, the price is 100x where it was back then at ~$20,000.

I have spent less time building blockchain models recently, but I do still keep an eye on a few of them as I think they can be useful for cycle identification even if the market is constantly changing. Of the models I do still look at, there are several similarities worth mentioning. The first is the MVRV model, or Market Value to Realized Value ratio.

MVRV was an extension of the “Realized Cap'' metric release by the Coinmetrics team, specifically Nic Carter and Antoine Le Calvez. The idea of Realized Cap is that if you were to value each Bitcoin at the price it was trading at the last time it moved, you would have something similar to the accounting value, or book value of the tokens if you treated them as inventory items. It was Willy Woo that gets most of the credit for popularizing MVRV, which was conceived by Murad Mahmudov & David Puell. The simple idea was to make a ratio of Bitcoin's market cap to the realized cap. The chart below is just that, the MVRV ratio.

Source: charts.woobull.com

I have taken the liberty of drawing the pink boxes around the points in time where the MVRV ratio has dropped below 1. As you can see, these times have been historically great buying opportunities. Another observation that you might have already picked up on is that time spent in the pink boxes can vary from as short as seven days to as long as ten months. So unfortunately, we cannot jump to the conclusion that by hitting the 1 level that we’re immediately out of the woods. Indeed, if 2015 contained a single lesson for the crypto market - it would be that bottoms are not always short and violent. But it’s not all bad if that was the lesson. Long bottoms have two very positive corollaries.

The first thing to bear in mind is that after the drawn out bottoming of 2015, we had a very long bull cycle, where prices of nearly all cryptos went up for about two years straight. The second thing to remember is that long bottoms give people more confidence that price discovery has taken place to such a degree that the market can “feel” satisfied in capital allocation decisions. Any teams left still building after surviving a brutal bear are leaner and stronger than they ever could have become in a raging bull market.

Another blockchain analyst that I think is clear-eyed and well-spoken about the market goes by the handle Checkmatey from Glassnode. If you’re not subscribed to their market updates, I highly recommend them. Recently, Checkmatey pointed out in Falling Dominoes: Capitulations Across the Board, that several other on-chain metrics are also showing signs of stress that generally tend to occur at or near market bottoms. For example, the Bitcoin Hash Ribbon model which tracks the computing power of the Bitcoin network is back in the red.

Source: @caprioleio.

These red zones highlight changes in hash power, indicating that Bitcoin miners are under pressure and even turning off some of their machines. These changes should not be seen as a red flag, however. Generally speaking, Bitcoin miners are found all over the globe and each organization has their own cost structure and levels of profitability. For example, most Bitcoin miners have some older equipment and some newer equipment. If the price falls to a certain level, the older machines aren’t profitable to run anymore. So the logical course of action is to switch them off and only use energy on the newer, more efficient models. In extreme cases, entire mining operations with high marginal costs could be liquidated and purchased by more efficient market participants. This kind of turnover is both important and necessary for the mining industry to be profitable and sustainable in the long-run.

The reason looking at hash-power models makes sense is that miners have a long time-preference and often have deployed many millions of dollars in Capex to set up their operations. This involves making deals with local energy producers, ASIC manufacturers, leasing buildings, and doing many of the same things you would expect of a modern data center. So when players that are large and sophisticated make changes, and it shows up in the data, it’s worth keeping an eye on.

As Travis has said recently, there’s a decent possibility that a change in the Fed’s policy or even a hint that they’re thinking about changing their direction could broadly coincide with a pivot for equities and other markets which are even more sensitive to Fed actions - like crypto. While the Fed is committed to crushing inflation, their tools are blunt enough that shock therapy might be the best metaphor. This bludgeoning of the economy and global markets via tightening monetary conditions has been on display this year as we witness record levels of wealth destruction going back 40-years or more.

How much is enough? I don’t think anyone can say exactly - but at least for now, our fates are intertwined - crypto and macro. I wish I had blockchain data going back forty years as well so we could conduct even deeper research. But alas, that is not the case. The path of least resistance seems like a crab-style market with heightened risk on many fronts. Recall that the last time we had commodity prices at levels near where they are now, we ended up with the Arab Spring.

Macro/geopolitical twists coming from an angle you don’t expect are what keep me up at night. You must consider those types of risks in conjunction with a host of micro information, which I believe includes Bitcoin valuation metrics. Many of those metrics indicate BTC is currently “cheap” on a historical basis, or at the least an attractive price to DCA. Risk is something that can never be done away with. Somehow, we also need to find the courage to swing the bat when the ball lines up with home plate. Certainly doesn’t mean you’re going to hit the ball every time - sometimes you swing too early, or too late. But swinging at good-looking pitches is an accurate metaphor for a big part of what we do at Ikigai. We’re honored and excited to be in the batter’s box.

Market Update – Liquid Crypto Asset Investing

Guest Author: Ikigai Trader Asher Montague-Warr

| Symbol | June | May | Apr | Q2-22 | Q1-22 | YTD | Q4-21 | Q3-21 | Q2-21 | Q1-21 | 2021 | 2020 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BTC | -38% | -16% | -17% | -57% | -2% | -57% | 6% | 25% | -41% | 103% | 60% | 303% |

| ETH | -45% | -29% | -17% | -67% | -11% | -71% | 23% | 32% | 19% | 160% | 399% | 469% |

| XRP | -21% | -28% | -28% | -59% | -2% | -60% | -10% | 31% | 23% | 161% | 278% | 14% |

| BCH* | -39% | -26% | -27% | -67% | -13% | -71% | -13% | -6% | -11% | 45% | 6% | 71% |

| EOS | -33% | -32% | -28% | -67% | -7% | -70% | -23% | -5% | -14% | 85% | 17% | 1% |

| BNB | -32% | -15% | -12% | -49% | -16% | -57% | 32% | 28% | 0% | 708% | 1269% | 172% |

| XTZ | -32% | -17% | -32% | -62% | -14% | -67% | -28% | 100% | -37% | 142% | 116% | 49% |

| XLM | -25% | -11% | -26% | -51% | -15% | -58% | -4% | -1% | -31% | 220% | 108% | 184% |

| LTC | -22% | -29% | -22% | -57% | -16% | -63% | -4% | 6% | -27% | 58% | 17% | 202% |

| TRX | -23% | 34% | -15% | -12% | -2% | -14% | -16% | 31% | -26% | 244% | 181% | 101% |

| Aggregate Mkt Cap | -32% | -23% | -19% | -58% | -5% | -60% | 13% | 33% | -23% | 146% | 186% | 301% |

| Aggregate DeFi* | -31% | -51% | -23% | -74% | -8% | -76% | 29% | 64% | -27% | 339% | 581% | 1177% |

| Aggr Alts Mkt Cap | -28% | -28% | -20% | -58% | -7% | -61% | 19% | 40% | 1% | 246% | 479% | 274% |

Source: CoinMarketCap. As of 6/30/22. BCH includes SV. Aggregate DeFi from Coingecko.

After one of the biggest deleveraging events in crypto history, we are currently beginning to see the aftermath of the tsunami. 3AC, one of the largest pools of capital in the space, being liquidated from their degen longs. Saylor being down more than $1bn on his Bitcoin purchases. Numerous other fractures happening in the crypto sphere - from lending protocols to on-chain models like Vitalik dismantling S2F. Amid all of this, BTC has broken records in terms of consecutive weekly red candles. BTC is still closely correlated to risk-on assets. The SPX had its worse H1 since 1962. Nasdaq had its worst 1H ever.

Source: @charliebilello. As of 6/30/22.

This month was a stark reminder that even with all the historical data, BTC still has the ability to surprise us. As we currently sit below the previous all-time high, we are experiencing a hangover from the recent crash. This is largely due to liquidations, weak miners capitulating and redemptions from various funds. Ultimately, the market crash we just experienced was due to an environment of too much leverage in the system. This increased risk of macro contagion as first world economies globally showed weakening economies and continued very high inflation.

Another interesting factor of this recent market crash is that it seems to be institutions that have this time lost very badly in numerous ways, whereas in past crashes retail bore the brunt of the losses. I actually interpret this factor as an indicator of the massive levels of interest in crypto from some very deep pockets. That is unprecedented.

With that said, I believe we will soon reach the period of “despair”, and this is by far the most opportunistic moment to look to reposition ourselves back in the market. We have an array of indicators that are signaling to us we are currently extremely oversold. So the question becomes, how long will the market stay down for? And is there more pain ahead? To quote Howard Marks, “being too far ahead of your time is indistinguishable from being wrong”. So timing is often imperative for survival and while I think the bottom is close, there may not be any significant bull market rally until all the weak hands have been rattled out.

Key Points

Bitcoin miners are selling out of necessity due to bad debt/high opex; this usually signifies the last leg of the bear market cycle.

One of the largest leverage wipe-outs in crypto history with large institutions being the primary driver.

Open interest has shown significant reduction in contracts, but room for more downside to achieve a full leverage washout.

Likely in the early phase of an accumulation schematic; patience will give us clarity on the bottoming structure.

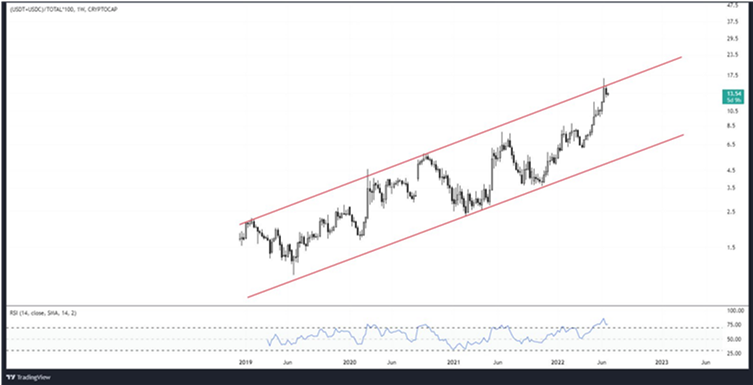

USDC and USDT relative market cap at historical highs, indicating huge amount of capital on the sidelines ready to be deployed back into the market.

Market may not be in complete despair yet as BTC Dominance is falling; market participants seem to still be finding hope in Alts.

Source: @caprioleio as of 06/29/22.

Hash Ribbons are shown above. Bitcoin miners have been forced into selling their BTC reserves or turn off inefficient machines to cover debts and operational expenses. The longer we stay down here in this depressed price range, the weaker miners are forced out of business and older machines are being turned off. Thus, we can see ~11% decline in hash rate between June 12th and June 29th -

Source: Blockchain.com. As of 6/29/22.

Historically miner capitulations have been a result of the final leg down in a BTC bear market. Once the weak miners have been flushed out, it significantly reduces sell pressure.

Source: @caprioleio As of 06/29/22.

At the current time of writing, we are sitting at electric production cost and below the 200 weekly MA. Show above, we have historically bottomed at these levels.

Source: Tradingview. As of 6/29/22.

The chart above shows the total market cap of the two most dominant stable coins in the market relative to the entire crypto market cap. Think of it as “Stablecoin Dominance”. I use it like a kind of fear and greed index. It is showing the majority of market participants are sidelined, waiting for re-entry. Historically, prices have bottomed when we reach the top of the channel - as market confidence has stabilized. One way of identifying accumulation would be to see this declining as market participants start deploying back into crypto assets.

Source: Coinalyze. As of 6/29/22.

Shown above, Binance Perp Open Interest has finally come back down to the July 2021 bottom. While this is reassuring, it may not be enough as Aggregate Open Interest still has more room to the downside. In order for this to happen, we would need to chop around heavily until longs and shorts get exhausted and begin closing positions. If not, price likely needs to decline further.

Source: Tradingview. As of 6/29/22.

The chart above is Bitcoin Dominance. Since Bitcoin is the index, we need to see it reclaim its throne before the markets can truly bottom. As the main collateral foundation for crypto, BTC has been uniquely punished in the recent leverage unwind. My confidence in a true market bottom will likely come with a large spike higher in Dominance. For now, that may be some time off.

Based off the data in front of me, I am expecting a bottom similar to the December 2018 and probably dragging on until October or November of this year. My base case is drawn out below, with a Bitcoin bottom around $15-16k.

Source: Tradingview. As of 6/29/22.

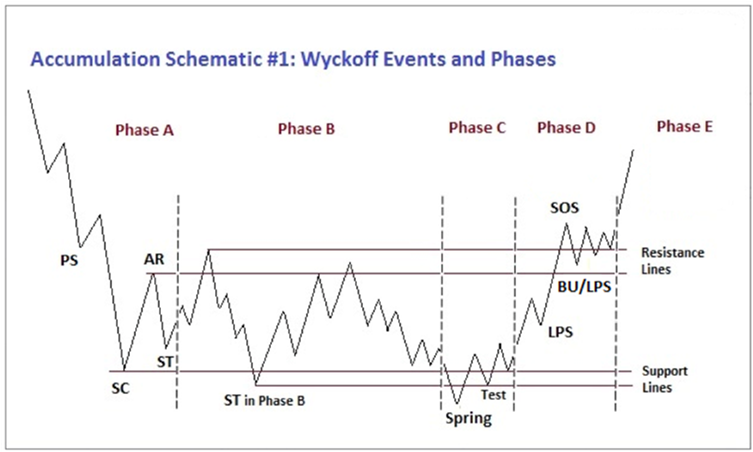

Alternatively, the pessimistic scenario and the most painful would be a full leverage washout. This would see us capitulating down further in price. At this point, we have to wait for an accumulation pattern to form like the one shown below before making any trading decisions. Ultimately, patience will pay off.

Source: school.stockcharts.com.

On the above chart, we are currently likely either at the PS or the SC. More price action in the coming weeks should give us more information about the range we are in.

Summary

Bitcoin is creating a bottom according to technical indicators, but the continued downward pressure from fund redemptions and liquidations is going to keep the price pinned down for now. Confidence has been rocked and I can’t imagine it will bounce back really quickly unless there is some kind of catalyst coming from the Fed, or perhaps another fundamental BTC-centric event like a spot ETF approval (although that looks rather slim). Our best bet is to wait for an accumulation schematic to form and then wait for inflation to show some signs of slowing down. Once that happens, there’s a high chance the Fed may begin to consider a pivot in policy. So for now, we will be sitting comfortably in a good chunk of cash, waiting for the right moment to present itself.

Closing Remarks

Tough month all around. That said, nearly every long-term indicator (price-based and on-chain-based) is signaling that the coming months are a great time to accumulate BTC. That doesn’t necessarily mean price will immediately rocket higher from here and in fact I would be surprised if it does. It also doesn’t mean that Bitcoin can’t act in a way it has never acted before, because it can, and it recently has, and certainly could again.

The macro picture appears set for more pain, until inflation rolls over or something in the global financial markets legitimately breaks. And that might happen. Treasury volatility, EU peripheral debt, JGBs/Yen, credit spreads. Something in the system could break in the coming months. I believe the most significant upside risk would be a credible move towards a Ukraine treaty. This would likely push commodity prices down, inflation expectations down, Fed tightening expectations down, equities up and crypto up.

So the near-term presents a lot of risk. But when I look at the totality of the macro and the micro, I don’t see anything that makes me seriously question the viability of this asset class and this technology over any medium/long term. As long as the Fed is tightening, I would expect the valuations of all assets to struggle, crypto included. But this too shall pass and crypto is in pole position to move the hardest off the bottom once monetary policy eases. In fact, that would be my base case.

I understand many of you are facing significant losses in your overall portfolio, crypto and otherwise. The US economy appears to be rocketing towards a recession and the real estate market is already correcting and likely to correct further. I believe right now is generally a bad time to decrease your exposure to crypto. I believe now is an outstanding time to be averaging into increasing your exposure to crypto, especially through an investment in Ikigai. I believe we will manage through whatever cyclical bottom may present itself in the coming months and have a good chance to crush this next cycle. Buying tops and selling bottoms is how you lose money in crypto. Leverage is the other way. We hope we have earned the trust of our investors to be stewards of their capital in this wacky world.

“One who smiles rather than rages is always the stronger.”

– Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2021 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS