August 2022 - Monthly Market Update

/Monthly Update || August 2022

“The superior investor is mature, rational, analytical, objective and unemotional.”

Opening Remarks

Greetings from Ikigai Asset Management¹ headquarters. We welcome the opportunity to bring to you our forty-seventh Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that already has and will continue to fundamentally change the world – continuing to create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

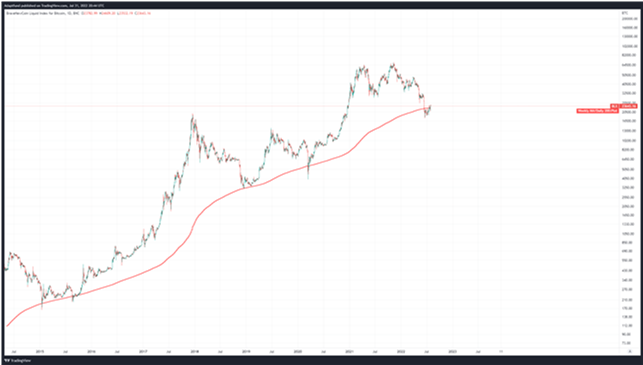

To that end, July brought a relief rally in risk assets across the board after an extremely rough 1H-22. SPX was +9% after being -6% in Q2. NASDAQ was +13% after being -23% in Q2. VIX was -26% after being +40% in Q2. Bitcoin followed suit, +18% after being -57% in Q2 and ETH, with its merge narrative starting to properly heat up, was +58% after being -67% in Q2.

I present those stats bundled together as such because crypto continues to be entirely beholden to macro. Over the last several months, crypto has been dealing with very bad micro alongside very challenged macro. All things considering, BTC -50% through July with the NASDAQ -21% is pretty good. The micro got better in July relative to June, but it would have been nearly impossible for that not to have been the case, given how rough June was. My expectation is the micro will trend better in August, even if that just means a lack of epic blowups/bankruptcies. Which will leave us again just beholden to macro, because this is what the last six weeks looked like-

Source: TradingView. As of 8/1/22.

Which is a bummer but it speaks to the strength of “don’t fight the Fed” and “it’s all one trade”, factors we’ve been talking about for a long time here and factors I went into at length on a recent Bankless episode.

This is Jay’s world at the moment and crypto is going to live and die by him, along with every other asset on planet Earth. We can look at an array of macroeconomic indicators and financial asset prices to try and glean what Jay might do and we can dissect his every word at press conferences to read the tea leaves (lying constantly is part of his job description). Hate it or love it, that will probably be time well spent if you’re trying to guess the price of Bitcoin over the next couple of months.

At the moment, most indicators would tell you we’re racing towards a recession in the United States. Technically, we’re already in one. The housing market looks to be heading towards its worst pullback since 08. Most Fed surveys are at levels they’ve never reached and not entered a recession. A variety of manufacturing and inventory indexes and surveys are flashing at recessionary levels. Even Google Trends-

Source: Google. As of 8/1/22.

There are some indicators that are not yet implying a recession but most of them are known to be lagging not leading - namely the labor market. Jobs have remained relatively strong, although there has already been a trend shift there. I would expect the labor market to weaken meaningfully through year-end and into 1H-23.

Source: TradingView. As of 8/1/22.

While a recession is bad news for Americans for obvious reasons, as it relates to the near-term trajectory for asset prices, I believe this is actually good news. Powell wants a recession to crush demand to get inflation under control. He’s raising interest rates and rolling off the Fed balance sheet for that exact reason. That’s quite a blunt tool but it’s all he has in his toolshed, and he’s made it clear he’s willing to use it. That tool appears to be working, and from the Fed’s stance of “data dependent”, the jobs market and inflation are the only indicators still holding reasonably strong (and I think that’s about to change). I believe this was the backdrop that had Jay “more dovish on the margin” than expected last week, which led to the strongest rally in stocks after a Fed meeting since 1970. I believe asset prices can bottom before a recession is even officially acknowledged, and certainly before a recession ends. The market is observing that the Fed may be nearing the end of its interest rate hikes, and asset prices care more about monetary policy these days than GDP growth. The chart below is telling. The higher line is the OIS curve (an approximate measure of Fed Funds futures) after the June FOMC meeting, and the lower line is the OIS curve after this most recent meeting.

Source: Goldman. As of 7/29/22

The futures curve is now betting the Fed is done with hikes in December and cutting by spring. Doesn’t mean it has to play out like that, but the OIS market is sensing the upcoming recession and betting that means hikes are coming to an end.

These expectations are showing up in the inflation market as well, with 5-year breakevens down 75bps in the last four months.

Source: Tradingview. As of 8/1/22.

All of this occurred in July in traditional markets into very thin liquidity and very lopsided positioning. I could show you half a dozen charts about how underinvested traditional markets were in July but take my word for it. Without that very bearish positioning, the setup for a rally in risk assets in August would be much less compelling.

The biggest risk at the moment continues to be the Ukraine conflict. Putin is in an advantaged position as the EU has a massive natural gas shortage problem looming this winter and he has the only viable solution. He knows this. The EU knows this. The US knows this. The manner in which this situation plays out will likely be the key factor for risk assets in 2H-22. If Putin holds the EU hostage for natural gas, it could quickly lead to global turmoil in financial markets. The exact timing of how it will play out is unclear. The situation bears paying close attention.

If that OIS curve above is indeed correct, it bodes well for crypto prices in the coming months. But with Ukraine, Taiwan and a host of other risks looming, the path is far from bright and sunny. Should these macro risks remain at bay, it’s pretty clear ETH presents the best risk-adjusted upside potential in crypto. The merge is a narrative I’ve been talking about here and elsewhere for many months (along with a bunch of other folks). The chatter has reached a fever pitch. Hundreds of hours of podcasts have been dedicated to the merge event at this point, yet the story continues to bring new twists and turns in real-time-

ETC, essentially a ghost-chain, saw its price increase 150% in July in advance of miners being forced out of ETH as it moves to PoS and potentially reviving the ETC project.

Most recently, rumors of an ETH PoW fork (somewhat similar to BCH with BTC in 2017) have swirled, although nothing has materialized to date and doesn’t necessarily have to. Kevin Zhou, founder of Galois Capital, has been leading much of this discussion on Twitter. I’m not sure how to price the likelihood of a legitimate ETH fork occurring before the merge. If a fork were to occur, it would likely be a price positive event for ETH, although could cause a knee jerk sell off at some point.

There has been some chatter about what centralized stablecoins USDC and USDT may do around the merge. Most of that appears to be scare tactics and not legitimate concerns, but that could change and it’s worth watching.

I have been vocally, publicly bullish on ETH and the merge catalyst since at least May 2021. I hope I have also clearly laid out the risks around the event, but as we move even closer to the merge, I want to lay them out again. There are many risks to the price of ETH going into, during and after the merge. Technical design risk. Technical implementation risk. Hack risk. Value accrual risk. Price manipulation risk. Illiquidity risk. There’s a lot of risk. I think the risk is priced attractively but I don’t intimately understand all of the risks. I could be mispricing one or more, potentially grossly. I may learn some new information and very rapidly decide the risk isn’t attractive anymore for any number of reasons. If you’re long ETH, you need to understand these risks. Price could do literally anything, including go down 50% in straight line. It just did that six weeks ago. Price could go up a lot then go down a lot (fade the news) and then go up even more. The merge could technically work, and price could go up a lot, but value accrual could eventually fail, and ETH could bleed out into oblivion like EOS. It’s not my base case, but it could happen.

Should ETH thread the needle with implementation. Should ETH value accrual hold. Should the Fed slow tightening. Should QT not implode some corner of the US financial market. Should the global financial markets remain reasonably stable. Should Taiwan not cause WW3. Should Ukraine not hold the EU hostage over natural gas and cause a continent-wide economic collapse and potential collapse of the Euro… Then ETH should work well. That’s a whole bunch of qualifiers though.

Invest

Ikigai is currently fielding interest from new investors globally. We are open to international investors and qualified accredited U.S. investors (including self-directed IRAs).

We accept new investors on the 1ˢᵗ and 15ᵗʰ of every month.

Contact us to see if you qualify.

June Highlights

Tesla Sells ~75% of Bitcoin Holdings for $936mm, Records $106mm Loss

SEC Charges Former Coinbase Employee in First Ever Crypto Insider Trading Scheme, Alleges Coinbase Has Listed Securities

Three Arrows Capital Files for Bankruptcy, Founders Go into Hiding

Celsius Files Chapter 11 Bankruptcy

India-based Crypto Lender Vauld Blows Up, Files for Bankruptcy, Owes $400mm

Voyager Digital Files Chapter 11 Bankruptcy, FTX/Alameda Propose Bailout for Voyager Customers, Voyager Doesn’t Like Bailout Terms

Jason Stone, Former DeFi Trader for Celsius, Sues Celsius, Claims CEL Token Market Manipulation, Infers Criminal Activity

Lending Firm Genesis Loses Hundreds $mm’s in 3AC Debacle

Crypto Exchange Blockchain.com Loses $270mm in 3AC Debacle

Auction House Christie’s Announces Web3 Venture Fund

Crypto VC Variant Raises $450mm in Two Venture Funds

Multicoin Capital Announces $430mm Venture Fund

Facebook’s Libra Spinout Aptos Raises $150mm, Led by FTX Ventures, Jump, Multicoin

Discussion Swirls About Potential ETH Fork Leading Up to ETH 2.0 Merge Date

Tether Announces it Holds Zero Chinese Commercial Paper and Will Hold Zero Commercial Paper by November 2022

Crypto Miner Core Scientific Reports Selling 7,202 BTC in Jun

BlockFi Announces It Will Not Accept GBTC as Collateral

Pomp’s Crypto Recruiting Firm Raises $12.6mm, Acquires Proof of Talent

Russia Announces Ban on Crypto Payment

“Into the Metaverse” on the Cover of TIME Magazine

Minecraft Announces Ban on NFTs

| Asset Class | July | Q2-22 | Q1-22 | YTD | Q4-21 | Q3-21 | Q2-21 | Q1-21 | 2021 | 2020 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | 18% | -57% | -2% | -50% | 6% | 25% | -41% | 103% | 60% | 303% | BTC |

| NASDAQ | 13% | -23% | -9% | -21% | 11% | 1% | 11% | 2% | 27% | 48% | QQQ |

| S&P 500 | 9% | -16% | -5% | -13% | 11% | 0% | 8% | 6% | 27% | 16% | SPX |

| Total World Equities | 7% | -16% | -6% | -15% | 5% | -2% | 6% | 6% | 16% | 14% | VT |

| Emerging Market Equity | 0% | -11% | -8% | -18% | -3% | -9% | 3% | 4% | -5% | 15% | EEM |

| Gold | -3% | -7% | 6% | -4% | 4% | -1% | 3% | -10% | -4% | 25% | GLD |

| High Yield | 6% | -11% | -5% | -10% | -1% | -1% | 1% | 0% | 0% | -1% | HYG |

| Emerging Market Debt | 3% | -13% | -10% | -19% | -1% | -2% | 3% | -6% | -6% | 1% | EMB |

| Bank Debt | 3% | -7% | -1% | -5% | 0% | 0% | 0% | -1% | -1% | -2% | BKLN |

| Industrial Materials | 1% | -25% | 16% | -12% | 8% | 2% | 8% | 8% | 29% | 16% | DBB |

| USD | 1% | 7% | 3% | 10% | 1% | 2% |

-1% | 4% | 6% | -7% | DXY |

| Volatility Index | -26% | 40% | 19% | 24% | -26% | 46% |

-18% | -15% | -24% | 66% | VIX |

| Oil | -3% | 8% | 36% | 44% | 3% | 5% | 23% | 23% | 64% | -68% | USO |

Source: TradingView. As of 7/31/22.

The Exciting Potential of Soulbound Tokens

Guest Author: Ikigai Researcher Odette Wu

The Web3 experience today is dominated by transacting hyper-financialized assets - characterized by the emergence and popularity of Defi, Socialfi, Gamefi and the speculation around art and profile picture NFTs. According to DefiLlama, total value locked in Defi currently stands at $88B (down from an ATH of $250B), and the cumulative total transaction volume of NFTs is approximately $97B. However, what’s missing in Web3 is interpersonal trust and other “relational settings” which are the basis of various human interactions. A secondary effect is that economic and social activities that rely on trust are not feasible on-chain, such as on-chain credit score, personal brands, uncollateralized P2P/communal lending, etc.

In Decentralized Society: Finding Web3's Soul, Vitalik et al. proposed a social identity primitive for “encoding social relationships of trust” on the blockchain. This paper reminds me of some of the public economics and political science readings I did in college. For example, the late Nobel Laureate Elinor Ostrom would very much be excited with the potential practical utilities of identity-linked NFTs (what Vitalik et al. call “Soulbound Tokens” or SBTs) in the context of collective decision making and coordination in public goods - a topic she discussed extensively in her book Governing the Commons. Political scientists like Robert E. Goodin would find networks and patterns of SBT ownership among different accounts (what Vitalik et al. calls “souls”) a good basis for examining the online manifestation of cross-cutting cleavages and social conflict, an issue that has significant explanatory power on the study of modern democratic society. In fact, as Vitalik et al. envisioned, a uniquely Web3-native decentralized society can have long-lasting impacts beyond finance into political, economic and social domains.

The Ikigai team studied Vitalik et al.’s paper internally in May and were intrigued by the wide range of applications that a decentralized society can enable, in the Web3 world and beyond. In this monthly, we will discuss some conceptual innovations by Vitalik et al., compare and contrast their innovation with current identity solutions, and discuss some practical use cases and applications.

Notes

Vitalik et al.’s paper is a wealth of information, we are not aiming for a comprehensive treatment, and we will inevitably leave some parts unaddressed.

The primary references are Vitalik’s original post on Soulbound, Vitalik et al.’s original paper and The Block Research’s research publications, authored by Hiroki Kotabe.

What are SBTs and Souls?

SBTs are “soulbound tokens”, which are NFTs that store identity-relevant data. Souls are accounts or wallets that hold entirely or partially publicly visible, and non-transferable SBTs that may be revocable by the issuer. A Soul is the Web3-equivalent of an identity and SBTs are attestations by others tied to one’s Soul, making a Soul like a CV with references. For example, a person can have a Soul that stores SBTs corresponding to a variety of affiliations, memberships, and credentials, including educations, employment history, club memberships, etc.

These SBTs can be “self-certified” (similar to how we may share information about our unique interests and skills and in our CV) or issued and attested by other Souls, who are trusted third parties serving as counterparties to these relationships. SBTs thus carry weight corresponding to the reputation of their issuers. The more reputable SBTs a Soul has, the more the individual starts to emerge. Social networks of trust and the carried meanings, manifested by patterns of SBT holdings of Souls, are then developed in coordination with others rather than separately by each individual. With a little creativity, it’s easy to imagine wide-ranging implications for SBTs.

There is no strict requirement for a Soul to be linked to a legal identity, nor for there to be “one human, one Soul.” Souls can be persistent pseudonyms with many SBTs that are not easily linkable. One individual may have several such persistent pseudonyms in parallel, and this is the Web3-equivalent of having multiple discrete identities.

Souls, and the various communities and collectives they belong to, together form the basis for a co-determined “decentralized society” (DeSoc), where Souls and (new) communities emerge from each other, creating goods and services at different scales. This is how Souls can drive changes in the political, economic, and social domains. For example, organizations (DAOs or NGOs) could use SBTs to make leadership and governance “programmatically responsive” to their constituents and patrons. As discussed in the original paper:

Leadership roles could dynamically shift as the composition of the community shifts, reflected in the changing distribution of SBTs across member Souls.

A subset of members could be elevated to potential leadership roles based on their intersectionality and coverage across multiple communities within the organization.

Initiatives that promote community cohesion could use SBTs to keep intersectional Souls at the center.

Organizations may opt for governance that elevates certain combinations of traits (characterized by SBTs’ holdings) more than others, such as diversity among zip codes.

Compare and Contrast SBTs with Other Identity Solutions

The Soulbound framework enables a digital individuation that allows a Soul to build reputation, establish provenance, and access services. It incentivizes people to protect their reputation and identity in web3.

This section compares and contrasts the Soulbound framework with four other prominent and adjacent identity primitives widely discussed in Web3

|

Identity Frameworks |

Notes/Explanation |

SBT & DeSoc Alternative |

|

The Dominant Legacy Identity Ecosystem |

Rely on pieces of paper or identity cards issued and mediated by a trusted 3rd party

Lacking social contexts, wildly inefficient, weak/no composability, doesn’t support rapid, efficient coordination. |

The security requirements of government IDs can be met and exceeded-

|

|

The Pseudonymous Economy |

Combining reputation systems with zero knowledge proof mechanisms to preserve privacy.

People accumulating transferable zero-knowledge attestations and evading reputational attacks by transferring a subset of attestations to new wallets without traceability. |

Over-separation of different aspects of identity renders it ineffective/unusable for many use cases.

By maintaining social context, people can maintain trust, even if they are under threat of cancellation, and hold attackers accountable.

|

|

Proof of Personhood (“PoP”) |

Aim to provide tokens of “individual uniqueness”, to prevent Sybil attacks and allow non-financialized applications.

Rely on approaches such as global analysis of social graphs, biometrics, simultaneous global key parties, etc. |

PoP focuses on achieving global uniqueness rather than social identities. PoP protocols are limited to applications that treat all humans the same.

Soulbound framework aims to help empower applications that are relational and move beyond just the unique human problem. |

|

Verifiable Credentials |

Verifiable credentials (VCs) are a W3C standard where credentials (or attestations) are zk-shareable at the holder’s discretion. |

VCs and SBTs can be natural complements |

Practical Use Cases and Applications

Provenance and Scarcity for Art, Video, Creative Medium, etc.

Artists can stake their reputations on their works. For example, an artist can issue tradable NFTs from her Soul account and accompany these NFTs with publicly verifiable (on-chain) SBTs that attest to the identification number and scarcity of every NFT in a collection.

This idea is extendable to any scenarios involving verifying scarcity, reputation, or authenticity. For example, when identifying fakes (deep fakes, fake news, etc.), time and social context are crucial for determining veracity. The blockchains can attest to the time, and SBTs can provide the deeper social contexts of the creation and the creator. One could cross-reference the metadata of a (fake) news piece to determine whether it is likely to be legitimate or a hit piece. “Fake news” is already a tremendous problem today and is virtually assured to get worse over time. The world desperately needs a solution to this issue and SBTs have the potential to be that solution.

On-chain Credit Score and Open Finance

Mainstream, publicly accessible money markets in Defi (such as AAVE and Compound) currently take the form of over-collateralized lending. Uncollateralized and under-collateralized lending in Defi cannot be scaled at the moment, as these products require some form of non-transferable and non-saleable reputation metrics like credit scores in traditional finance. A good example is what Teller protocol was building in their V1.

In traditional finance, credit scores determine one’s creditworthiness and serve as critical evidence in applying for uncollateralized loans. However, it is a centralized and flawed system in terms of its opacity, sub-standard data security practice, arbitrary assessment process and built-in systematic bias. In Web3 and Defi, building an alternative on-chain credit score should be urgent, thereby bringing financial services to those shunned by the traditional system. That can help the world and its worth working on.

An ecosystem of SBTs could be the building blocks of a censorship and bias-resistant credit score framework. SBT-based credit and reputation systems may arise in a bottom-up manner with embedded economic and relational contexts, where SBTs representing education credentials, work history, rental contracts, P2P lending experiences, etc. will serve as the record of credit-relevant history.

Uncollateralized loans could be issued as non-transferable-but-revocable SBTs as a kind of non-seizable “reputational collateral”. Loan security is, in theory, derived from two key properties of SBTs: non-transferability prevents one from transferring or hiding the outstanding loans, and social interconnectivity makes it difficult for a borrower to escape their loans by forging a new soul. When loans are repaid, the loan SBTs could be replaced with a proof of repayment which adds to a soul’s credit history.

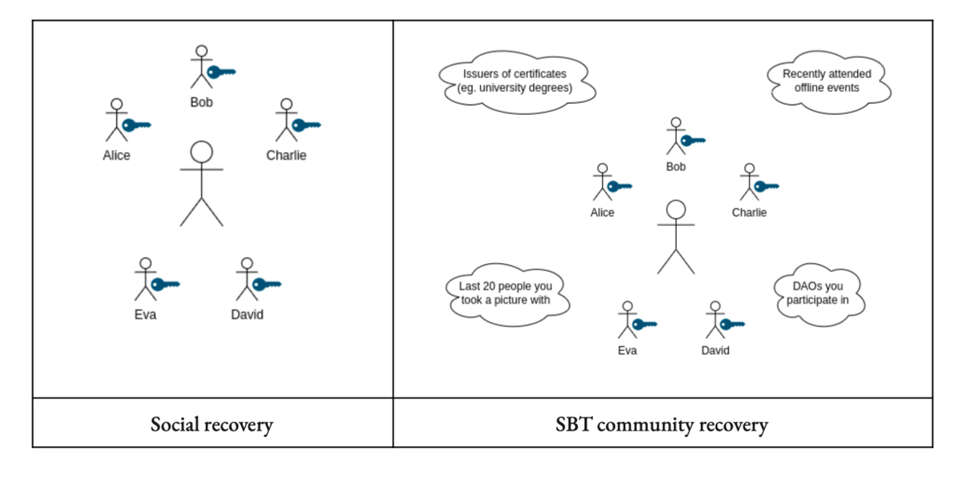

From Social Recovery to Community Recovery

Wallet recovery methods like muti-sig recovery or mnemonics have different tradeoffs in terms of mental overhead, ease of transacting, and security. Social recovery is an alternative that relies on an individual’s trusted relationships. SBTs allow for an even broader paradigm: community recovery, where souls perform the authentication.

Under social recovery, the user curates a set of “guardians'' and gives them the power to change the keys of her wallet by a majority rule. Guardians could be a mix of individuals, institutions, or other wallets. The challenge is that a user needs:

A reasonably high number of guardians

Guardians from discrete geographical or social backgrounds such that they won’t collude

Maintaining frequent updates with guardians

Source: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4105763

A more robust solution is to tie recovery to a Soul’s memberships across communities, drawing on a broad set of persistent relationships for security. In a community recovery model, recovering a Soul’s private keys would require a member from a qualified majority of a random subset of a Soul’s communities to consent.

Souldrops as an Alternative to Airdrops

Varying degrees of intersections among Souls - “cross-cutting cleavages” - would enable “digitally-separable” communities. These communities could convene at intersections as specific as “holder of X token & proof of contributing to source code of Protocol Y & attended Conference Z at least 3 times in the last 5 years.”

The primary method used today to summon a DAO is an airdrop based on past on-chain activities, which is vulnerable to strategic manipulations. A more sophisticated method is an airdrop based on computations over a unique Soul’s SBTs and other tokens – thus the “souldrop.” A simple computation could airdrop only to Souls that possess some specific combination of SBTs, while a more sophisticated scheme could programmatically overweight certain SBTs over others. For example, a protocol may want to weight source code contributions more heavily than community participation, thereby rewarding contributing developers more than the average user.

Conclusions and Discussions

On-chain identity is an often-discussed but currently unsolved problem. When evaluating new use cases for crypto assets, we often ask ourselves “how ready is the tech for the world” and “how ready is the world for the tech”. With use cases such as Defi, NFTs and gaming already establishing significant traction but with shortcomings, we believe the ecosystem is rapidly approaching a point where on-chain identity is “an idea whose time has come”. We believe the Soulbound framework has a good chance to be the solution to that need. Vitalik et al. 's Soulbound framework offers an alternative to current identity primitives used in Web3, and it has the potential to enable more transformative use cases on-chain and in real world applications. We believe more theoretical and practical innovations will emerge in the coming years. A decade from now it could easily be transformative.

Regarding our new venture fund, we have yet to receive a pitch deck that incorporates the Soulbound framework, and we are looking forward to learning how a team might integrate Souls as the identity layer in their product. Hopefully we can help form some of those ideas along the way.

Market Update – Liquid Crypto Asset Investing

Guest Author: Ikigai Trader Asher Montague-Warr

| Symbol | July | Q2-22 | Q1-22 | YTD | Q4-21 | Q3-21 | Q2-21 | Q1-21 | 2021 | 2020 |

|---|---|---|---|---|---|---|---|---|---|---|

| BTC | 18% | -57% | -2% | -50% | 6% | 25% | -41% | 103% | 60% | 303% |

| ETH | 58% | -67% | -11% | -54% | 23% | 32% | 19% | 160% | 399% | 469% |

| XRP | 15% | -59% | -2% | -54% | -10% | 31% | 23% | 161% | 278% | 14% |

| BCH* | 27% | -67% | -13% | -64% | -13% | -6% | -11% | 45% | 6% | 71% |

| EOS | 44% | -67% | -7% | -56% | -23% | -5% | -14% | 85% | 17% | 1% |

| BNB | 29% | -49% | -16% | -45% | 32% | 28% | 0% | 708% | 1269% | 172% |

| XTZ | 23% | -62% | -14% | -60% | -28% | 100% | -37% | 142% | 116% | 49% |

| XLM | 0% | -51% | -15% | -58% | -4% | -1% | -31% | 220% | 108% | 184% |

| LTC | 12% | -57% | -16% | -59% | -4% | 6% | -27% | 58% | 17% | 202% |

| TRX | 6% | -12% | -2% | -9% | -16% | 31% | -26% | 244% | 181% | 101% |

| Aggregate Mkt Cap | 22% | -58% | -5% | -50% | 13% | 33% | -23% | 146% | 186% | 301% |

| Aggregate DeFi* | 39% | -74% | -8% | -67% | 29% | 64% | -27% | 339% | 581% | 1177% |

| Aggr Alts Mkt Cap | 26% | -58% | -7% | -51% | 19% | 40% | 1% | 246% | 479% | 274% |

Source: CoinMarketCap. As of 7/31/22. BCH includes SV. Aggregate DeFi from Coingecko.

Firstly, I’d like to wholeheartedly thank the readers for tuning in. It’s been quite an eventful month and as usual we will do our best to decipher the market clues from the data to figure out the next move in the crypto sphere.

The most anticipated market event of July was the 7/27 FOMC meeting. The Fed announced a 75bps increase to the Fed Funds rate (as expected) and Powell's surprisingly “dovish on the margin” tone gave risk assets the green light and catalysed a significant rally. Nearly every other FOMC meeting this year ended up with markets dumping shortly thereafter, so this rally has been a welcome relief thus far. The knock-on effects from 3AC’s bankruptcy have also probably come to an end, or nearly so. Both of these factors point to an improved backdrop relative to the last several months.

Key Points

3 Arrows Capital has likely finished its liquidation

FOMC meeting was dovish on the margin

Inflows from exchanges show capitulation on par with other market bottoms

Puell Multiple indicator flashing a buy signal

CME gap which has a high tendency to get filled is sitting just above at $27k-$28k

Downside liquidity still remains a juicy target for bears at 18500

Bitcoin is reclaiming the 200 weekly MA and has historically only stayed below it for short periods of time

Source: @Slurpxbt.

The 3AC on-chain wallet tracker shows they have approximately $80mm of holdings left over. It’s unclear if they will end up selling that too, but in any case, the majority of the holding are in stables so further risk of crypto assets falling in price due to them having to liquidate seems less likely. 3AC brought to light a new kind of systemic risk in the crypto market, one more opaque than metrics such as Open Interest or Perp Funding, which have historically been used to gauge how levered the market is. We’ve now seen the risks of shadow leverage via loans from platforms like Voyager, Celsius, Deribit, Genesis, BlockFi, blockchain.com and many others. Unfortunately, events like these are apparently a necessary part of the maturation of the crypto market. I’m hopeful that going forward, check and balances will be put in place to prevent events like this happening again.

Assuming that Bitcoin is sent to exchanges with the intent to sell, capitulation seems apparent from the sheer number of BTC that recently flowed onto exchanges (shown below). Exchange inflows from June 2022 were rivalled only by the infamous Covid crash in March 2020 and the very peak of the bear market in 2018. These spikes indicate coins being transferred from weak to strong hands and quite indicative of market bottoms.

Source: CryptoQuant. As of 7/29/22.

The Puell Multiple, an indicator created by David Puell, is still one of the most interesting metrics for finding cyclical turning points for BTC and its currently flashing a buy signal. The metric is meant to estimate sell pressure from BTC miners. Miner selling capitulation from being over-leveraged or unable to cover operational costs has historically occurred in the depths of market bottoms. After some time, the selling subsides, and price once again resumes an uptrend. We also see a similar look from the hash ribbons (shown below) as stated in last month’s update. These two charts are helpful in conjunction and indicative of a bottoming process.

Source: @caprioleio. As of 7/29/22.

Source: Glassnode. As of 7/29/22.

Looking immediately ahead, I am targeting the overhanging CME gap sitting at $27k-$28k. I think there’s a decent chance that level is hit in August and then where we go from there is TBD. I believe there is still a good chance we could come all the way back down to retest the June lows. While a more V-shaped recovery like the Covid crash is possible, and some metrics (like the ones shown above) are showing some similar signs, the macro backdrop isn’t the same and the money printer isn’t currently going Brrr. Therefore, a V-shape bottom is not my base case. After the CME gap is filled, moving back to cash may make sense depending on how price action unfolds at those levels. It seems likely that we go through a sideways accumulation phase, with the market quieting down and volatility reducing - entering a more boring phase of the market. Capitulation can happen in two ways: one is more obvious when price goes down rapidly and liquidates a lot of market participants. The second form of capitulation is with time: long drawn-out periods causing participants/miners to lose interest or sell for other capital demands, as conviction in a price bounce wanes and participants target lower prices to buy back later.

Source: Tradingview. As of 7/31/22.

Source: Tradingview. As of 7/31/22.

The indicator above represents estimated areas of liquidity. It’s calculated using the total number of perp contracts opened at a specific price point, then presents the liquidation zones of high leverage traders. High leverage is identified by 100x, 50x and 25x. It’s far from a perfect metric but it does present some potentially helpful information. The light gradient immediately above current price indicates a fair bit of shorting at the highs, which could serve as fuel for price to head higher, were we to reach those levels, potentially taking BTC up to around the CME gap. This setup adds confluence to my thesis that we could fill the CME gap on an ensuing rally. You will also note the large liquidity incentive to the downside too around $18.5k. There's no guarantee we have to come back down, but if we do end up showing signs of weakness then that's a good area for accumulation and potential bottom.

Recent price action is only the 4th time in Bitcoin history price has gone below the 200-week moving average. At time of writing, we have reclaimed this level, which is a promising sign of recovery when compared to previous occasions.

Source: Tradingview. As of 7/31/22.

Summary

Bitcoin appears to be in a bottoming phase, and we are likely to form a large range for some months ahead. Liquidation events over the past month have started to end and sell pressure has subsided. It helps that there appears to be light at the end of the tunnel with inflation possibly peaking and Powell suggesting that a slowdown in tightening is likely for future FOMC meetings. There are plenty of global risks right now that bear close attention, including Nancy Pelosi’s visit to Taiwan in the near-term. Any number of macro risks could still cause the market to have a knee-jerk reaction and give back the gains made from this recent rally as risk broadly sells off. However, the ETH merge is upon us and there are lots of promising signs to suggest we are bottoming. So long as our global leaders keep a lid on war and inflation maintains a downward trajectory, confidence should return to the crypto market.

Closing Remarks

July was a month where crypto started to heal from the aftermath of the Shadow Leverage Daisy Chain Unwind. The wounds are still fresh and further wounds may be inflicted still. The full aftermath will take many months to completely resolve. While that was going on, macro factors were swirling and weighing heavy on crypto. They remain so today.

The above factors do nothing to slow the innovation occurring in the crypto ecosystem. In fact, it’s the opposite. Future bull markets get made in bear markets. No one can pay enough attention to get much done during bull markets. The folks that build the stuff that the market loves to speculate on build that stuff in bear markets. That’s occurring now. And for the first time, Ikigai has a venture vehicle to be involved in that part of the market.

I’m really excited about that. I’d be lying if I said my venture chops are currently up to snuff. I haven’t put nearly enough time in to really understand and have a well-informed view on the early-stage crypto market. Frankly I’ve been too busy paying attention to macro. We’re fortunate enough to have Odette who has been spending all his time there for several years. And I’m looking forward to turning more of my attention to the early-stage crypto market. I believe I can help, and it is a personal life goal of mine to have a meaningful part in designing a token structure that gains significant adoption. I believe I can do it, but it will require focused attention.

I am energized by how wide open the early-stage crypto landscape still is. Most problems are still unsolved. Very little of this ecosystem is set in stone at this time. I used to say that in 2018 and it’s surprising how true it still is. There are plenty of venture folks that have a much deeper understanding of this landscape at the moment, but we’ve got a fresh perspective and we’ve never been shy about rolling up our sleeves to do the work. I see our entry into the early-stage crypto landscape as both an amazing opportunity and a big responsibility. We’re honored to be here.

“If you do not enter the tiger’s cave, you won’t catch its cub.”

– Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2021 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS