July 2026 - Monthly Market Update

/Monthly Update || July 2026

“Every great money manager I’ve ever met, all they want to talk about is their mistakes. There’s a great humility there.”

Opening Remarks

Greetings from Ikigai Asset Management¹. We welcome the opportunity to bring to you our ninety-fourth Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into new technologies that have tremendous potential to make the world a better place and create trillions of dollars of value in the process.

We believe, in some cases, that we are obligated to be shepherds of some of these technologies – to do our little part to push ideas towards fulfilling their potential. We strive to be an objective, reasonable, well-intentioned voice of truth amongst a chorus of biased, fallacious, pernicious opportunists. It’s an honor that we take seriously.

To that end, crypto had a bad June while stocks traded fine. It’s a continuation of the trend we’ve seen all year.

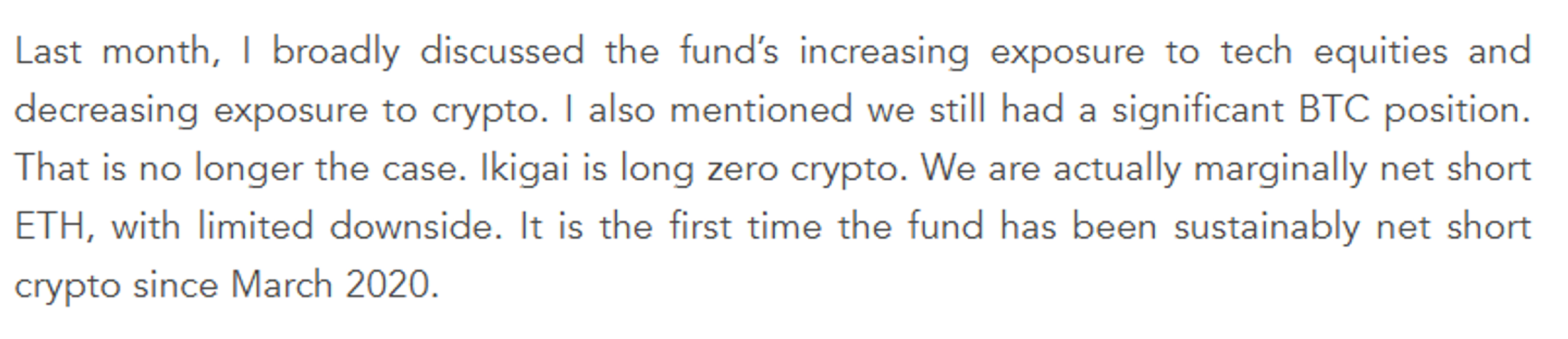

In last month’s letter we talked about the fund’s ongoing shift in exposure. I said-

That worked out well. In June, QQQ -1%. SOXX +12%. DRAM +17%. BTC -20% . ETH -22%.

On June 17th, the US and Iran signed a 14-point MOU (electronically; Trump signed in Versailles, Iran president signed in Tehran). The MOU is most accurately described as a 60-day “tactical ceasefire extension”.

The core elements of the MOU include:

Immediate/permanent end to military ops on all fronts (explicitly including Lebanon).

Iran to use "best efforts" for safe commercial passage through Strait of Hormuz (no charge for 60 days; Iran retains sovereignty/management, potentially with Oman/IMO dialogue—wording that allows Iranian interpretation of "service fees" vs. US "free and open").

US to lift naval blockade (announced/started removal June 18), issue 60-day oil export waivers, release some frozen assets, and support a $300B+ reconstruction fund (details deferred).

Iran reaffirms no nuclear weapons path; uranium dilution/stockpile talks in final deal under IAEA.

Monitoring mechanism; no new sanctions/force during window.

As soon as the MOU was signed, both sides started arguing about the details and implementation. Hormuz tolls and nuclear disarmament are the two main sticking points. And there were additional “hiccups” in the back part of June. Israel rejected the MOU’s ceasefire applicability to them and continued limited attacks in Lebanon. There were also limited “tit-for-tat” attacks between Iran and the US in Hormuz, adding to the friction.

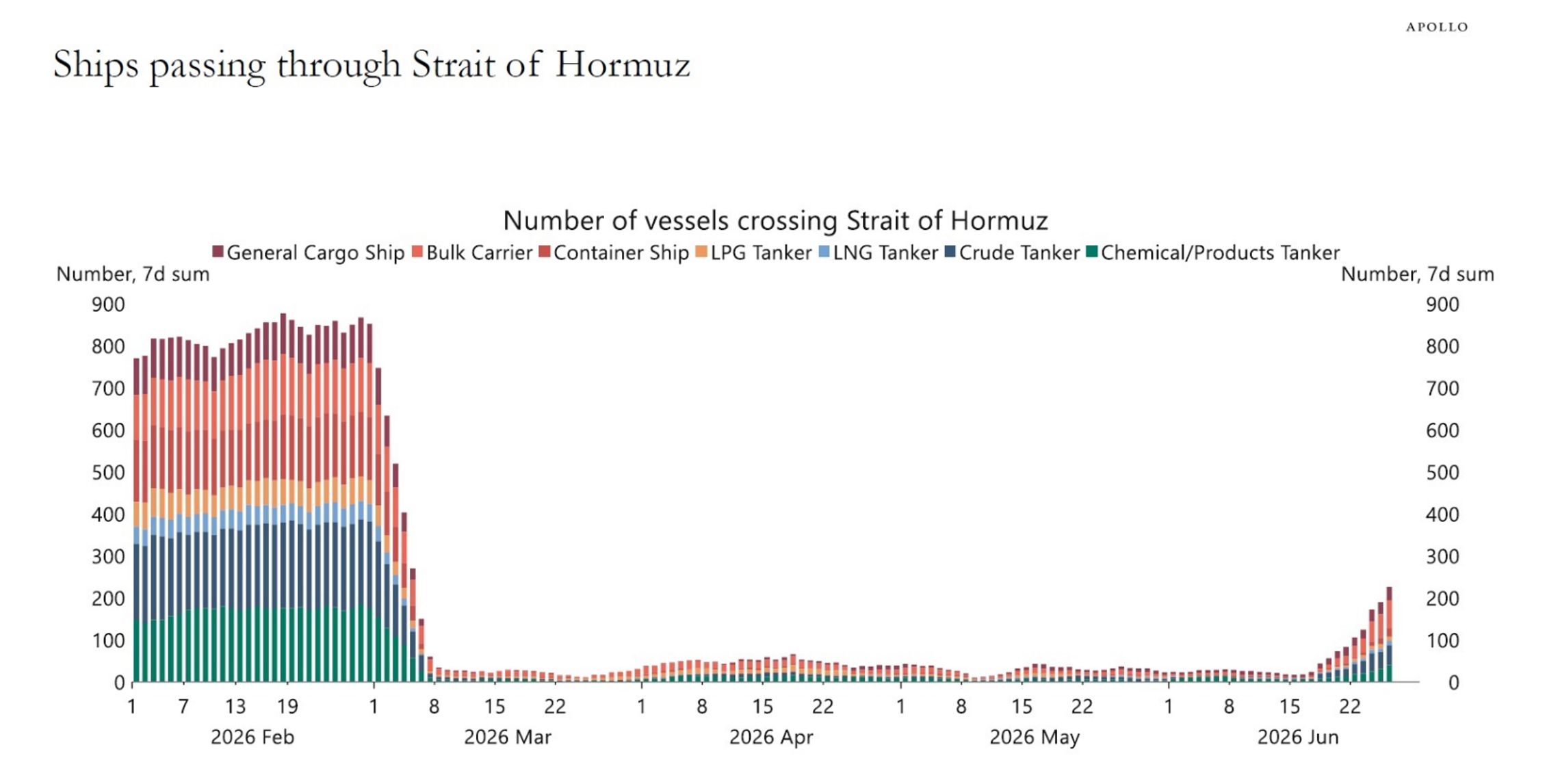

Overall, the situation is tenuous but appears to be heading in the right direction. In particular, this chart is heading in the right direction-

Source: @hedgeye. As of 6/29/26.

And that chart has led to this chart-

Source: TradingView. As of 6/30/26.

So while the Iran conflict is still very much up in the air, the impact on financial markets has been fading and should continue to fade. God willing, there won’t be another life lost in this conflict.

The Iran conflict has served as the market’s wall of worry over the last four months, and the Trump admin has put on a clinic on how to control the narrative so as to reduce financial market impact. It’s been impressive to observe. And there’s no telling how much higher stocks would have been if it weren’t for the Iran conflict. Because even WITH Iran, SPX is still +9% from pre-Irean levels. QQQ is +21% from pre-Iran levels. SOXX +80%. MU +178%. Wow. That’s how strong the appetite is for AI Value Chain exposure.

For as strong as the appetite has been for AI Value Chain stocks, the appetite for crypto has been almost equally as weak. The main driver for that weakness in June was unequivocally Michael Saylor.

June Highlights

MSTR Sells 32 Individual Bitcoins, Price Immediately Crashes ~20% In A Straight Line

After Crashing MSTR and STRC Prices, Saylor Announces new “Digital Credit Capital Framework”; Authorizes Additional Future BTC Sales

BTC ETFs See $4.5bn of Outflows; ETH ETFs See $530mm of Outflows

Visa, Stripe, Mastercard, BlackRock and 140+ Other Companies Jointly Launch New Stablecoin OUSD, To Share Revenue Amongst Partners

Binance Fails To Secure MiCA License, To Stop Serving EU Clients in July

Coinbase Launches Tokenized Stocks

CFTC Launches Sweeping Rule Proposal For Prediction Markets

CME To Sue CFTC Over Approval of Perpetual Futures

Framework Venture Raises $400mm Fourth Fund, Expands Scope Away From Crypto

Variant VC Raises $222mm Fund, Pivots Away From Solely Crypto To AI and Autonomy

Blockworks Acquires Messari for ~$10mm

BlackRock Launches BTC Covered Call ETF

Ethereum Foundation Lays Off 20% of Employees

BitGo Lays Off 15% of Employees

| Asset Class | Jun | May | Apr | Q1-26 | YTD | Q4-25 | Q3-25 | Q2-25 | Q1-25 | 2025 | 2024 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | -20% | -3% | 12% | -22% | -34% | -23% | 6% | 30% | -12% | -6% | 121% | BTC |

| NASDAQ | -1% | 11% | 16% | -6% | 20% | -6% | 2% | 18% | -8% | 20% | 25% | QQQ |

| S&P 500 | -2% | 5% | 11% | -5% | 9% | 2% | 8% | 11% | -5% | 16% | 23% | SPX |

| Total World Equities | 1% | 5% | 9% | -1% | 10% | 2% | 8% | 10% | -1% | 20% | 14% | VT |

| Emerging Market Equity | 2% | 7% | 13% | 4% | 22% | 2% | 11% | 10% | -5% | 31% | 4% | EEM |

| Gold | -7% | -2% | -2% | 24% | -8% | 11% | 16% | 6% | 19% | 64% | 27% | GLD |

| Long-Duration US Treasuries | -1% | 0% | -1% | 4% | -1% | -1% | 3% | -5% | 2% | -1% | -8% | TLT |

| High-Yield Corporate Credit | -1% | 0% | 1% | -5% | -1% | 1% | 4% | 3% | -2% | 6% | 8% | HYG |

| Copper | 2% | 6% | 6% | 8% | 8% | -6% | 11% | 15% | 2% | 23% | 19% | CPER |

| USD | 1% | 1% | -2% | -2% | -3% | -1% | -1% | -7% | -4% | -9% | 7% | DXY |

| Volatility Index | -15% | -25% | -33% | -22% | -55% | -8% | -4% | -24% | 28% | -14% | 3% | VIX |

| Oil | -8% | -12% | 16% | 84% | 54% | -6% | 1% | -5% | 2% | -8% | 13% | USO |

SOURCE: GROK. AS OF 6/30/26

The Saylor Problem

I’m not going to give you a full unfurling of all the facts of this Saylor situation. It would take me too long and it would probably be redundant for most of you, because if you’ve been paying any attention at all to crypto over the last month, this will already be on your radar.

Instead of reporting the facts, I’m mostly going to be sharing my opinion – which is often wrong. So keep that in mind. And because most of what we talk about here today is going to be opinions, you can just include a silent, implied “I think” at the beginning of each sentence.

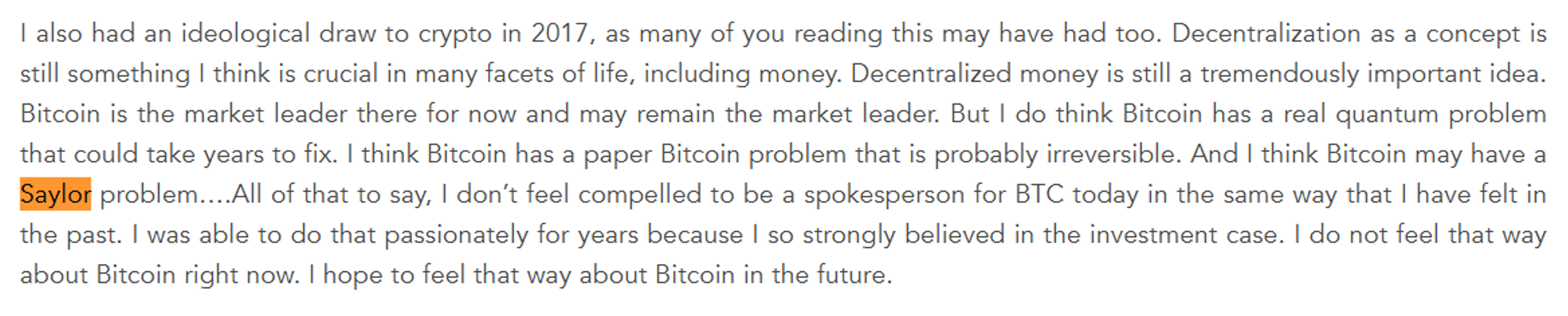

I think Saylor has made a series of missteps. I said as much in my May 1st letter –

Over the last month, he accelerated those missteps and in June it became very clear to the entire market that BTC does indeed have a Saylor problem.

Source: TradingView. As of 6/30/26.

The specific way The Saylor Problem reared its head was through the dwindling of MSTR’s dividend/interest coverage. In Feb, MSTR had built up a $2.25bn USD reserve, which equated to ~30 months of coverage at that time. In the subsequent months, Saylor: 1) issued so much STRC ($10bn); 2) Bought so much BTC; and 3) Bought back so many converts, that at the lows in late June, coverage had dwindled to ~9 months.

The market expressed its displeasure with Saylor’s actions in a variety of ways in June-

MSTR was down 45%.

STRC “depegged”. I use that term specifically because Saylor marketed STRC as a money market fund. It traded as low as 72 before bouncing to 85 at month end. STRC is supposed to trade at 100. The MSTR CEO said STRC is 80% owned by retail.

STRK is the cousin of STRC – but it pays a flat 8% perpetual. There’s been $1.4bn issued. It’s already traded terribly for a year and traded down another 15% in June.

There are six tranches of converts, maturing from 2028-2032. Total par value of $6.7bn. They all traded down in June, and on average were down about 20%.

And finally, BTC was down 20%.

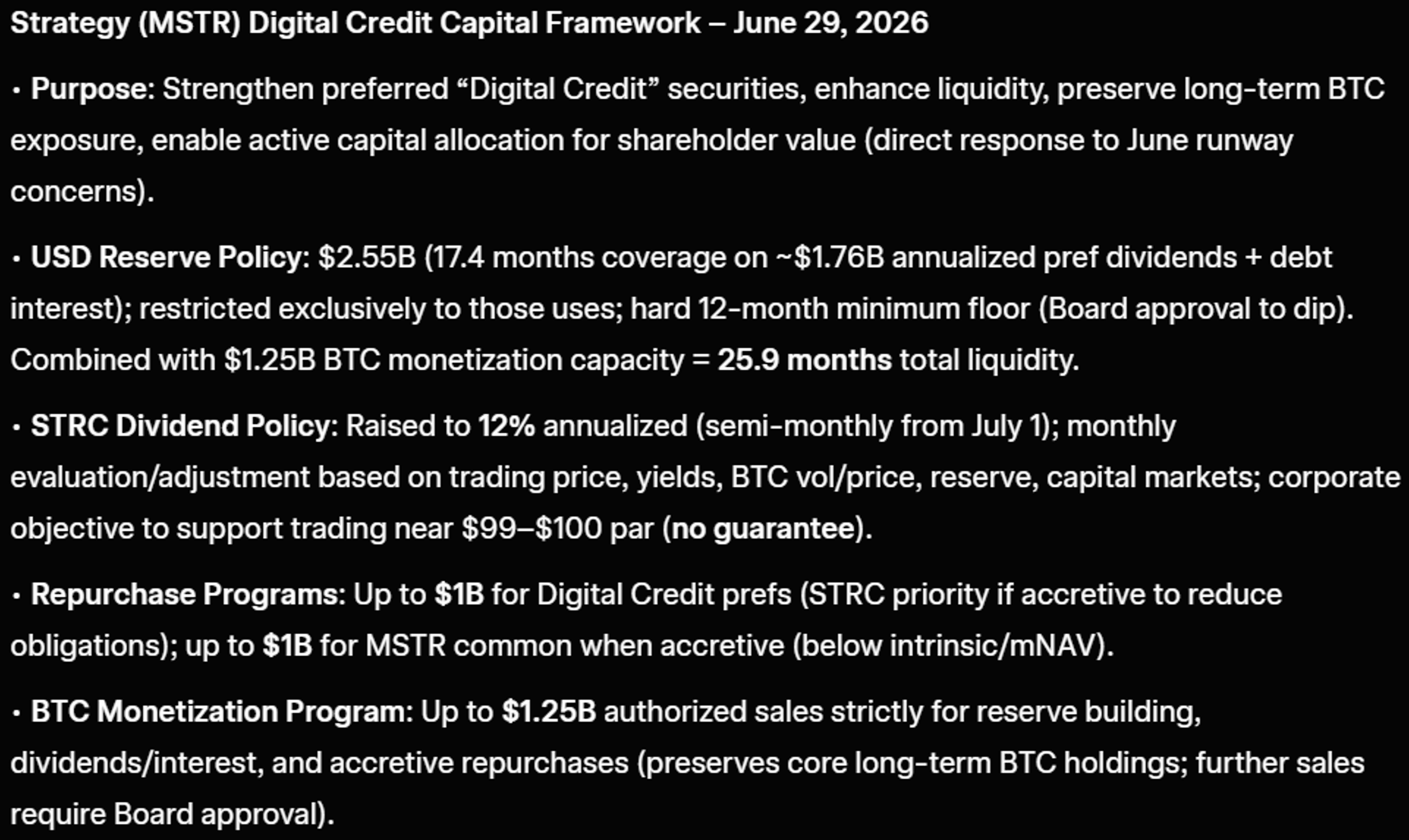

Needless to say, by the end of June Saylor was feeling the heat. The STRC chart was looking like the LUNA chart from four years ago. MSTR was in a death spiral. So on June 29th Saylor released the “Digital Credit Capital Framework”.

Here’s the overview-

Source: Grok. As of 6/30/26.

As of the afternoon of the 30th, the announcement bounced STRC from 72 to 85. MSTR is up about 5% from the pre-announcement lows, after being down 50% in a straight line. BTC is 2% below its pre-announcement price.

All of that to say, the market, across nearly a dozen different financial instruments, isn’t exactly pleased with the state of things at the moment. Saylor has problems - so BTC has The Saylor Problem.

Two days before the Framework was announced, I wrote a tweet about what Saylor SHOULD do-

Sell however many billions of $ of BTC necessary ASAP to take out all the converts and the prefs (yes Saylor can do things near-term that are damaging to these instruments so he can buy them back cheaper; that’s a separate topic).

Do the sale in one huge chunk. There are DEF huge buyers of BTC down 20-30% (just guessing where it would get done).

Flatten the entire cap structure. No debt no converts no prefs (makes total sense for a business that quite literally does nothing).

Then Saylor goes on a media campaign swearing up and down to Satoshi that he is NEVER going to do ANYTHING again. Nothing. Ever. Won’t buy another dollar of BTC. Won’t sell another dollar. Never touch the cap structure again. MSTR will just hold however much BTC they have left after selling a lot to clean up the cap structure.

This would pop BTC hard immediately (which is part of the reason you know the BTC sale deal would get done) . And over time, if Saylor does NOTHING, the market will eventually derisk him and his foolishness. And BTC can head much higher (still a big quantum problem and a paper Bitcoin problem but those are separate topics).

This is the NO BRAINER right decision for Saylor to make. Right decision for MSTR (which I don’t care about at all) and right decision for BTC (which I care about a lot).

This was what he SHOULD do. This is not what I thought he WOULD do. And it’s not what he’s done. At least not yet. I think the entire complex is going to continue to struggle in this current situation because BTC price is going to struggle. That’s at the base of all this.

BTC price needs to go up enough where he can avoid what he SHOULD do, which I laid out above. I’m not so sure that’s going to happen. After seeing the Framework announcement on the 29th and thinking about it, the question is-

If you're a deep pocketed investor that is considering buying billions of BTC (it’s going to take quite a few of those to drive prices much higher from here), was the Framework announcement a green light to buy now?

Doesn't feel like it to me. Feels like “Saylor risk” is still very much in BTC price right now. So why buy vs wait for that risk to ACTUALLY get cleaned up? You can’t find anything better to do with your capital? That’s certainly not the issue right now. So those are the would-be buyers who aren’t going to be buying.

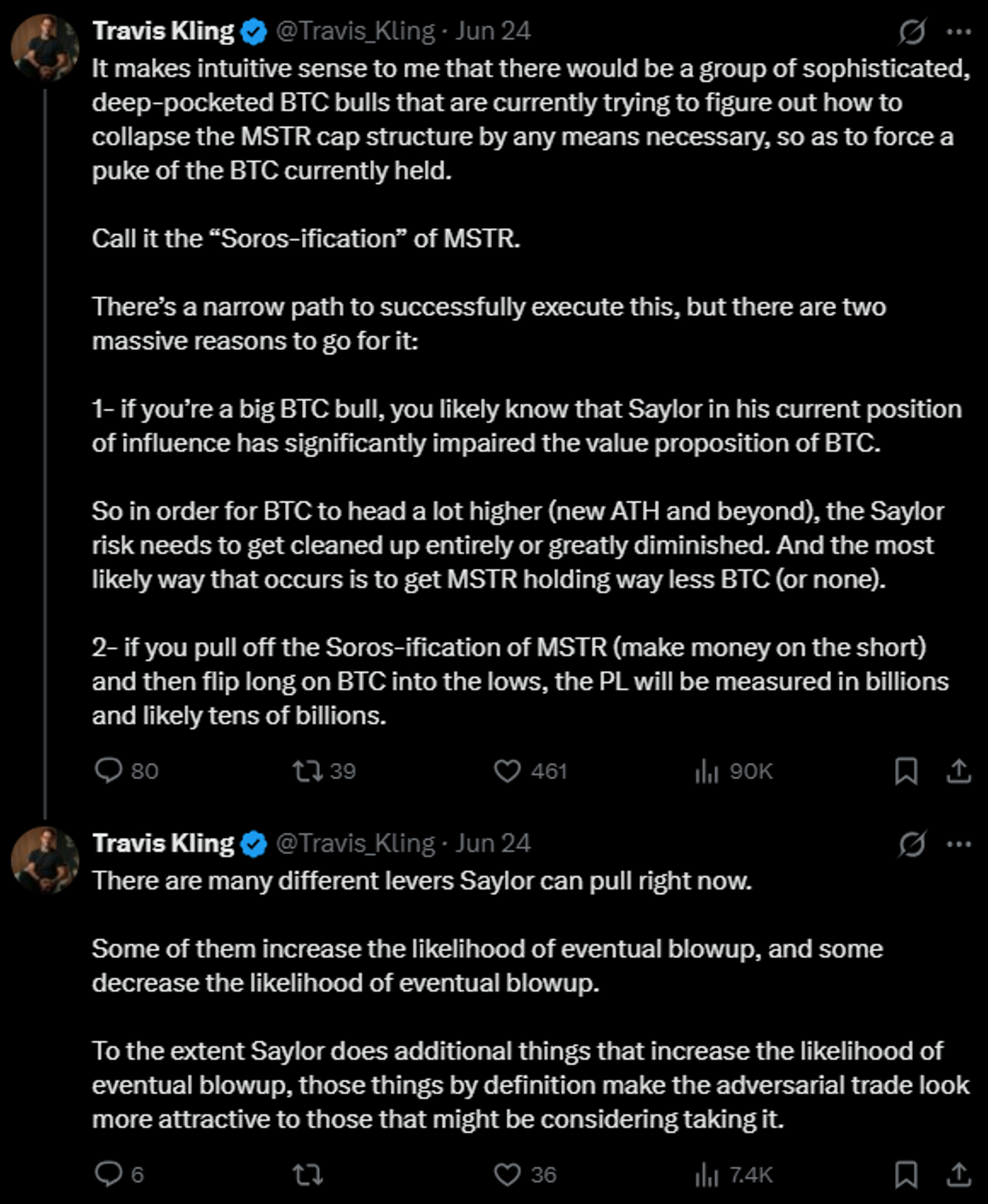

Then there’s a second category of market participants who might be actually playing offense AGAINST MSTR. On June 24th, I had this two-parter-

I said it because I meant it. It was my honest assessment of the situation. I just call it like I see it.

Within the context of that second tweet, I think the Framework announcement was not a significant step in the wrong direction. Remember, Saylor had made a series of really bad missteps. So there was some chance that was going to happen again, and he could immediately be a big pickle.

I don’t think that’s what happened. This felt like a kick the can announcement. Prices have traded as such so far.

I think all of it continues to muddle along. Pretty much his only choice is to slowly sell BTC to fund dividend/interest payments and then in 2028, start to sell BTC to cover the principal repayments.

MSTR has no mNAV premium and it’s probably not going to get one any time soon (ever?), so the ability for MSTR to issue equity is going to be pretty limited (absent some grander plan).

The market will smoke everything if he issues any more STRC or converts or really much of anything, except maybe some common if it’s above 1 mNAV.

I think the market will firmly reject the idea of him buying MORE BTC. I think that era of Saylor has drawn to a close. He likely has too much. He may have way, way too much.

But there’s a path where he leaks out enough BTC to repay all encumbrances on the balance sheet and he can sit there and do nothing and perhaps that will be enough for BTC price to head much higher from there.

You’d really prefer for it to get totally cleaned up and I think that requires MSTR to hold MUCH less BTC than it does now. MSTR holds 847k BTC. The whole cap structure has something like $22bn of par value encumbrances. Let’s say he sells enough BTC tomorrow to pay the whole $22bn off. Let’s say he sells the BTC down 30% from here because that’s what the market is going to make him pay to sell $22bn in one slug. 30% down from $59k is $41.3k. $22bn / $41.3k is 533k BTC. He’d have to sell 533k BTC, 63% of his total stack. Amazingly, I think that would be the perfect right-size for the market to be able to let go of The Saylor Problem. But he’s got to really promise he’s done with all this foolishness going forward. We’ll see how it turns out.

I try to give people the benefit of the doubt, but I am also a student of human nature, and I try hard to call things as they are. When I look at Saylor’s actions as of late, I see underlying pride, arrogance and greed. It’s impossible for me to see anything else. He could have bought SO much BTC and everything still would have been totally fine. But he just needed more. More leverage. More financial engineering. Financial engineering on top of financial engineering. So certain that BTC price would keep going up and he could keep issuing more of whatever anyone will buy in order to buy more BTC. And now he’s a seller of BTC, potentially for the foreseeable future, and potentially in big size.

A tale particularly common at the upper echelons of crypto, but also a tale as old as time. People can have it all and still want more and end up flying too close to the sun. Icarus is a 3,500 year-old story.

Market Update— Liquid Markets Investing

| Name | Jun | May | Apr | Q1-26 | YTD | Q4-25 | Q3-25 | Q2-25 | Q1-25 | 2025 | 2024 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| S&P 500 | -2% | 5% | 11% | -5% | 9% | 2% | 8% | 11% | -5% | 16% | 23% | SPX |

| NASDAQ-100 | -1% | 11% | 16% | -6% | 20% | -6% | 2% | 18% | -8% | 20% | 25% | QQQ |

| Magnificent Seven | -2% | 7% | 14% | -12% | -2% | -4% | 12% | 23% | -8% | 29% | 42% | MAGS |

| Bitcoin | -20% | -3% | 12% | -22% | -34% | -23% | 6% | 30% | -12% | -6% | 121% | BTC |

| Ethereum | -15% | -11% | 7% | -25% | -48% | -28% | 67% | 36% | -45% | -11% | 46% | ETH |

| Solana | -7% | -1% | 0% | -32% | -42% | -35% | 48% | 42% | -52% | -19% | 312% | SOL |

| BNB | -15% | 4% | 0% | -18% | -17% | -14% | 53% | 9% | -14% | 23% | 124% | BNB |

| Hyperliquid | -5% | 70% | 24% | -28% | -13% | -22% | 81% | 67% | -38% | 45% | n/a | HYPE |

| Aggregate Mkt Cap | -10% | 5% | 11% | -21% | -13% | -24% | 16% | 24% | -19% | -11% | 136% | TOTAL |

| Aggr Alts Mkt Cap (ex top-10) | -12% | -5% | 4% | -25% | -22% | -24% | 34% | 25% | -34% | -16% | 72% | OTHERS |

| Semiconductors | 12% | 23% | 40% | -10% | 104% | -8% | 15% | 28% | -12% | 32% | 49% | SOXX |

| Expanded Tech Software | -15% | 21% | 5% | -5% | -12% | -3% | 9% | 16% | -7% | 19% | 22% | IGV |

| ARK Innovation (disruptive tech) | -1% | 8% | 12% | -18% | 3% | -11% | 25% | 31% | -23% | 19% | 38% | ARKK |

| Robotics & AI | -6% | 4% | 16% | -12% | 3% | -8% | 19% | 22% | -15% | 15% | 30% | BOTZ |

| Quantum Computing | 2% | 18% | 25% | -10% | 47% | 7% | 38% | 59% | -31% | 88% | n/a | QTUM |

SOURCE: GROK. AS OF 6/30/26.

For the third consecutive month, tech stocks broadly outperformed crypto, and by a notably wide margin. I would expect that trend to continue, both for fundamental reasons and just looking at the charts.

For QQQ, some have called this last six weeks of price action “distribution” –

Source: TradingView. As of 6/30/26.

That would not be my base case. I think that’s consolidation before heading higher.

SOXX has been consolidating for about a month, but in an even stronger posture than QQQ –

Source: TradingView. As of 6/30/26.

Note that SOXX didn’t even sniff the 50DMA (purple) while QQQ firmly tested and bounced off it. SOXX looks like it wants higher.

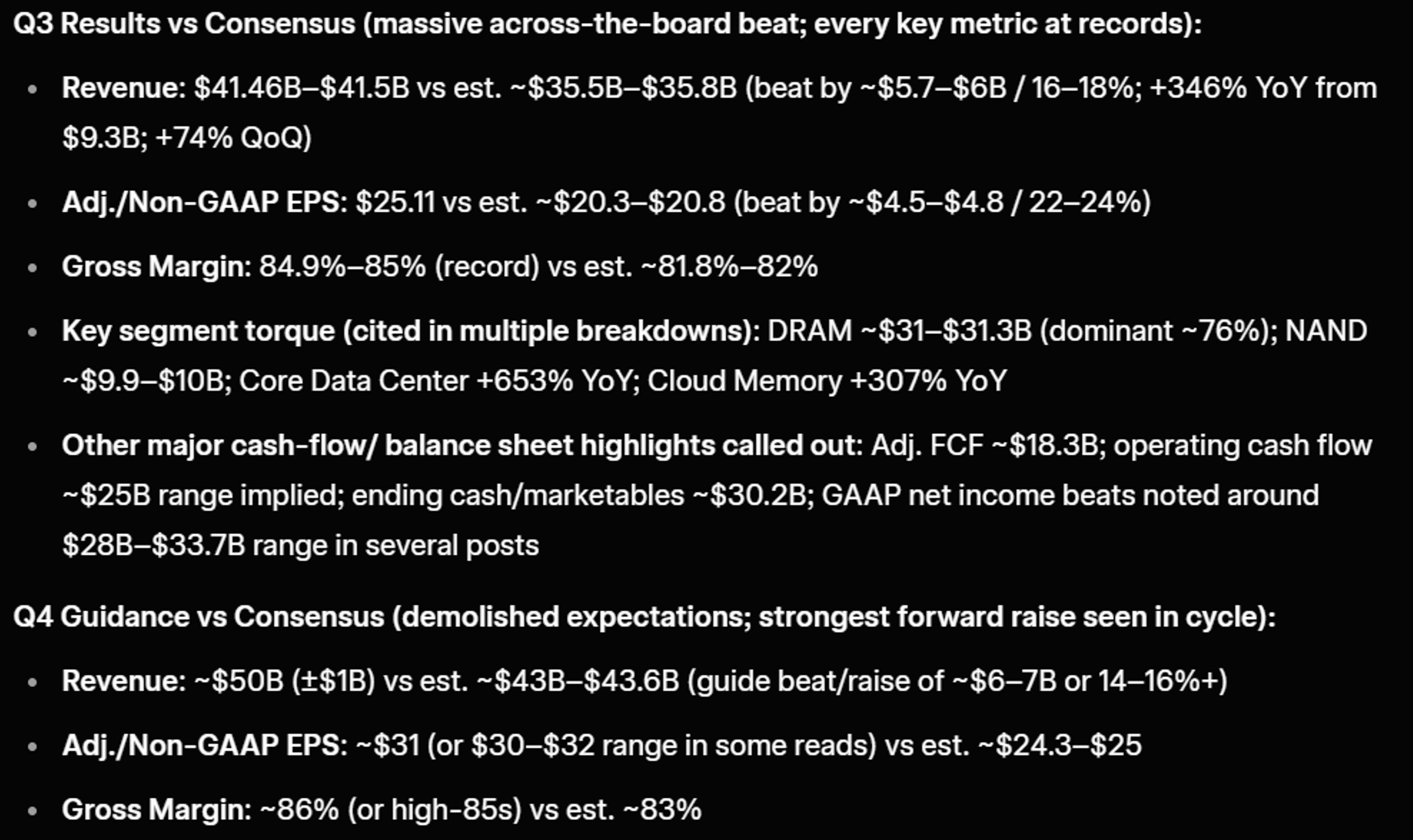

MU is a name we’ve talked about for multiple months in a row. They put up one the most breathtaking quarters in the history of public companies and that is not an exaggeration. Here is a summary-

Source: Grok. As of 6/30/26.

Guiding to $50bn of revenue next quarter on 86% margins (they will almost certainly beat on both). That’s notably better than NVDA has ever done.

The chart has been insanely strong (not even sniffing the 50DMA) but it’s been consolidating for a few weeks now-

Source: TradingView. As of 6/30/26.

That doesn’t look like a top to me. I don’t think the fundamentals warrant a top here either.

MAGS (the Magnificent 7 ETF) was down 9% in June - it’s worst month in over a year. We talked about that last month. MAGS are the capex spenders. AI Value Chain are the capex receivers. So the market has been selling one and buying the other. Chart looks like this-

Source: TradingView. As of 6/30/26.

It’s at a pretty interesting spot right here. Retesting the 200DMA (yellow) as resistance after breaking below. MACD flipping positive. Good volume into the bottom. Got decently oversold on RSI. We don’t have any direct exposure here at the moment but that could change. We have a ton of indirect exposure.

MAGS also had to make room for a new big boy with the largest IPO in history – SPCX raised $86bn at a $1.77tn valuation. The IPO made Elon a trillionaire on paper. The chart looks like this-

Source: TradingView. As of 6/30/26.

SPCX priced at $135, opened at $150, closed day 1 at $165. Traded as high as $224 and as low as $150, where it’s bounced along quite a few times. That $150 level has held so far, but I doubt it holds in the coming months. The fund has zero exposure here. We might be interested down 50% from here, months or quarters from now.

Software gave up its May gains this month. IGV down 13% in June-

Source: TradingView. As of 6/30/26.

That chart looks like it wants to go test the 200DMA in yellow. Many of the names in IGV – ORCL, PLTR, CRWD, CRM, APP, NOW – are major battleground stocks. The fund has limited exposure to software names, but we do have some, in the direction of “AI enabled”. At this point I’m not sure that I’m itching to get a lot more exposure in this general direction.

PENG is a $4bn market cap HPC platform solutions provider. Their business has significant torque to the memory boom. Chart looks like this-

Source: TradingView. As of 6/30/26.

PENG has been consolidating for a month. Earnings report 7/7.

Overall, I think tech stocks head broadly higher in 2H-26. There are all sorts of risks to that. Layers of risk. But it is not my base case these stocks are about to top for the year.

Moving on to crypto, BTC, ETH and SOL all look bad. I’ve been saying that for months now and it’s been correct and they still look bad today.

Last month, with BTC at $72k, I said-

“I don’t really see a strong reason technically why this shouldn’t go back to the bottom of the range - $60k or low $60s.”

A month later we’re at $59k and the chart looks like this-

Source: TradingView. As of 6/30/26.

Frankly I would be shocked if that white circle of price action was some kind of major bottom. It might be a bottom for a few weeks or a month or two at most. I think BTC sees lower lows this year. TBD on how much lower.

ETH looks worse-

Source: TradingView. As of 6/30/26.

In June, ETH fully lost its range, retested the prior range support, and failed at resistance. Then immediately puked. That is pretty textbook. There is some support at the white X around $1400ish, but eventually I think this heads to the white circle at $1000 and we see how the narrative is down there.

SOL traded as low as $60 in June before closing the month at $75. From a TA perspective, it is noteworthy that there is a lot of air underneath price currently. This is most easily shown with the VRVP indicator on the right side of the chart-

Source: TradingView. As of 6/30/26.

Note the gap in volume highlighted shown in the white circle. Low $30’s looks like the next major area of support. I am not aware of a current narrative that would keep SOL from heading to these levels, but perhaps I will be surprised.

HYPE was down 10% in June, outperforming most other crypto by a decent amount. Chart looks like this-

Source: TradingView. As of 6/30/26.

The structure tested and held the prior range high as support (yellow line). But it’s making this diamond-shaped thing that doesn’t look great to me. If it loses the yellow line, low $40’s is prob the next stop.

I’m not itching for any crypto long exposure in any form at the moment.

Closing Remarks

The Saylor Problem sucks. It sucks that he did these things that put BTC in this place. It’s greed to the point of stupidity. The market let him do it because the market is greedy and now BTC has a Saylor Problem.

History doesn’t repeat, but it often rhymes. And The Saylor Problem rhymes with other problems crypto has had in the past. Arthur Hayes and BitMEX. Sam Bankman-Fried and FTX. Changpeng Zhao and Binance. Terra Luna. 3AC. Celsius. BlockFi. It’s not exactly the same. There’s no fraud at MSTR AFAIK. A blowup is not imminent. But it’s a problem. And the situation probably needs to change meaningfully from its current state in order for BTC to move meaningfully, sustainably higher.

No need to worry though (unless you find yourself uncomfortably long crypto, in which case IDK what to tell you). We have tech stocks to pay attention to. We have AI Value Chain stocks to research. The hottest sectors on the planet in perhaps the most consequential stock theme of all time. It’s not a hard choice about where to allocate your attention and dollars.

“The shortcut is the long way.”

-Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2023 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS