June 2026 - Monthly Market Update

/Monthly Update || June 2026

“I’ve always loved to play games, and face it: investing is one big game. You need to be decisive, open-minded, flexible and competitive.”

Opening Remarks

Greetings from Ikigai Asset Management¹. We welcome the opportunity to bring to you our ninety-third Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into new technologies that have tremendous potential to make the world a better place and create trillions of dollars of value in the process.

We believe, in some cases, that we are obligated to be shepherds of some of these technologies – to do our little part to push ideas towards fulfilling their potential. We strive to be an objective, reasonable, well-intentioned voice of truth amongst a chorus of biased, fallacious, pernicious opportunists. It’s an honor that we take seriously.

To that end, the stock market. And especially tech stocks. And especially especially “AI Value Chain” stocks… Traded exceptionally well in May despite Hormuz staying ~90% closed all month and remaining closed today. Crypto traded poorly. BTC down 3%. ETH down 11%. SOL down 1%. QQQ +11%. SOXX +23%.

This price action disparity was coincidental timing. I spent the majority of last month’s letter talking about Ikigai’s move away from crypto towards tech stocks, and more specifically, AI Value Chain stocks. The main section of today’s letter will be a continuation of that discussion. So if you didn’t read last month’s, I really would urge you to do that before reading this one. I think I am a fair self-critic, and last month’s letter was prob a top 10-15 all-time for me. FWIW.

Last month, I broadly discussed the fund’s increasing exposure to tech equities and decreasing exposure to crypto. I also mentioned we still had a significant BTC position. That is no longer the case. Ikigai is long zero crypto. We are actually marginally net short ETH, with limited downside. It is the first time the fund has been sustainably net short crypto since March 2020.

I don’t want you to think that I think a crypto crash is imminent. I don’t think that. And the fund is very long tech equities, so that’s certainly not a net short portfolio. Not even close.

Honestly I thought: 1) the TA looked bad on ETH; 2) the DAT era seems dead; and 3) the fundamentals seem quite bad. So we have a little ETH short. Might TP it tomorrow, might keep it.

If Clarity Acts gets passed, BTC/crypto should get at least SOME sort of rally. The Kalshi looks like this-

Source: Kalshi. As of 5/31/26.

$2.1mm decent volume but not massive. Note that the odds peaked right into the Senate Banking Committee vote and then declined after the committee vote was passed. There was a flurry of headlines after the committee vote passed that made it seem like passing a Senate floor vote was very much not a sure thing. So I think that explains those charts.

I will say that crypto is not trading like this is going to pass. Not at all. But it is still very much a headline driven situation. For example, on May 29th Jamie Dimon said Brian Armstrong was “full of shit” on Fox Business.

Another example, the bump you saw on the Kalshi chart was Trump tweeting this on May 27th-

So the Clarity Act passing a Senate vote seems very much in flux right now. If it fails the vote (or more likely just never gets to a vote in the first place), BTC/crypto probably make new lows. If Clarity Bill looks like it’s going to pass (or if a Senate vote even gets scheduled), BTC/crypto should get at least some rally.

I would be wary of that rally. It does not seem like there are tens/hundreds of billions of dollars that are just waiting for Clarity Act green light and then they’re jumping in. That would not be my base case, for a few reasons. One of which is all the money is going to AI Value Chain stocks.

May Highlights

Clarity Act Advances Out of Senate Banking Committee with 15-9 Vote; Unclear If It Will Pass Senate Floor Vote

Saylor Says On MSTR Earnings Call They Will Sell BTC

MSTR Reports Selling 32 BTC for $2.5mm

MSTR Buys $2.1bn of BTC in Two Tranches; Issues $2bn in STRC; Buys Back $1.5bn of Convertible Debt with Cash on Hand

BTC ETFs See $2.4bn of Outflows; ETH ETFs See $540mm of Outflows

SEC Commissioner Hester Peirce Tweets Imply That Synthetic Tokenized Stock Exposure May Be Regulated As A Security

Circle Raises $222mm at $3bn Valuation in ARC Token Presale From BlackRock, Apollo, et al

A16Z Crypto Raises $2.2bn in 5th Crypto Venture Fund

Huan Ventures Raises New $1bn VC Fund, Expands From Crypto To AI Agents

Bullish Acquires Leading Transfer Agent Equiniti For $4.2bn In Stock Tokenization Push

SEC Delays Plan For Approving Tokenized Stocks

CFTC Issues Blanket No Action Letter on Prediction Markets

Tether Acquires SoftBank’s Stake in Bitcoin DAT Twenty One Capital Run By Jack Mallers

US Has Reportedly Seized ~$1bn of Iran Funds

Anthony Pompliano’s DAT Sells BTC to Buyback Shares

Coinbase Cuts 14% of Workforce

| Asset Class | May | Apr | Q1-26 | YTD | Q4-25 | Q3-25 | Q2-25 | Q1-25 | 2025 | 2024 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | -3% | 12% | -22% | -16% | -23% | 6% | 30% | -12% | -6% | 12100% | BTC |

| NASDAQ | 11% | 16% | -6% | 21% | -6% | 2% | 18% | -8% | 20% | 2500% | QQQ |

| S&P 500 | 5% | 11% | -5% | 11% | 2% | 8% | 11% | -5% | 16% | 2300% | SPX |

| Total World Equities | 5% | 9% | -1% | 13% | 2% | 8% | 10% | -1% | 20% | 1400% | VT |

| Emerging Market Equity | 7% | 13% | 4% | 26% | 2% | 11% | 10% | -5% | 31% | 400% | EEM |

| Gold | -2% | -2% | 24% | 20% | 11% | 16% | 6% | 19% | 64% | 2700% | GLD |

| Long-Duration US Treasuries | 0% | -1% | 4% | 3% | -1% | 3% | -5% | 2% | -1% | -800% | TLT |

| High-Yield Corporate Credit | 0% | 1% | -5% | -4% | 1% | 4% | 3% | -2% | 6% | 800% | HYG |

| Copper | 6% | 6% | 8% | 22% | -6% | 11% | 15% | 2% | 23% | 1900% | CPER |

| USD | 1% | -2% | -2% | -3% | -1% | -1% | -7% | -4% | -9% | 700% | DXY |

| Volatility Index | -25% | -33% | -22% | -61% | -8% | -4% | -24% | 28% | -14% | 300% | VIX |

| Oil | -12% | 16% | 84% | 87% | -6% | 1% | -5% | 2% | -8% | 1300% | USO |

SOURCE: GROK. AS OF 5/31/26

Tech Stocks Part 2

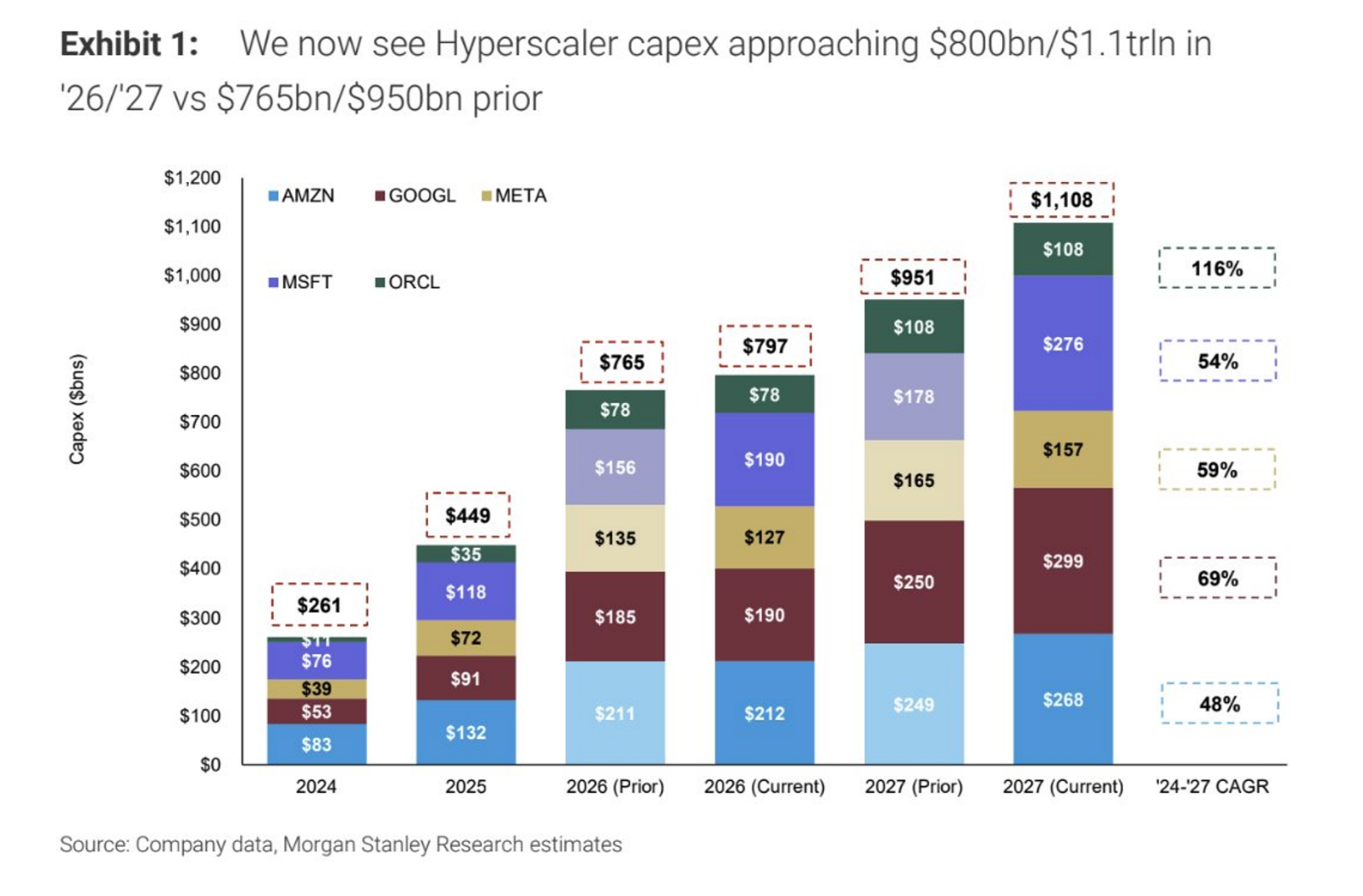

Last month we talked about how bullish tech stocks are, specifically AI Value Chain stocks (although there are other tech sectors that are trading well too). I highlighted a Morgan Stanley Hyperscaler capex chart, that showed the five Hyperscalers spending a combined $1.1.tn in capex in 2027. The chart looked like this-

Right below that chart, I said this-

So the main thing I want to do here today is just reiterate that stance above and build on it a little bit. To reiterate – this capex backdrop is the SINGLE thing that I think matters more than anything else about this AI Value Chain trade. If I wanted to boil the whole thing down to one chart, it’s definitely THAT chart.

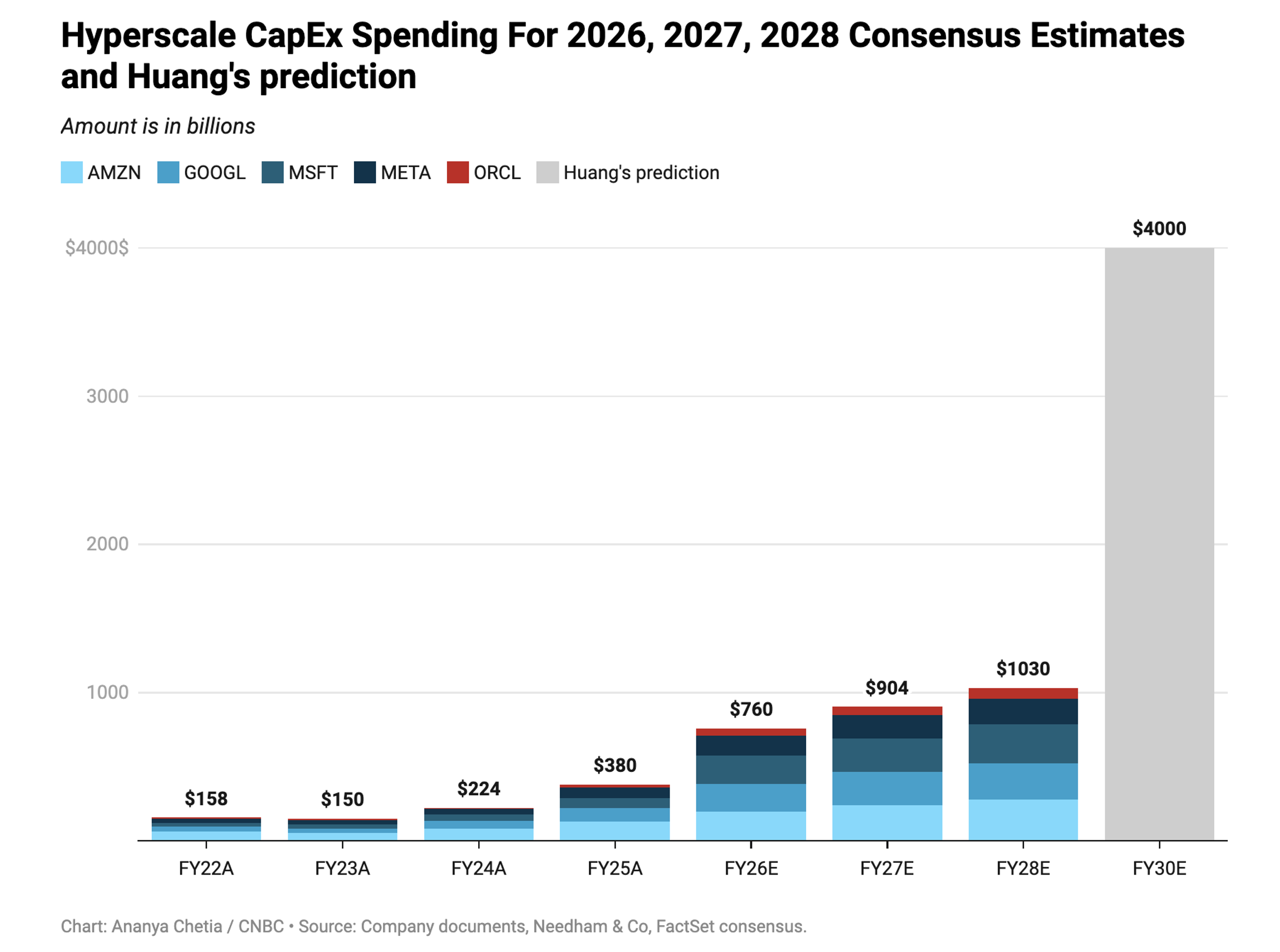

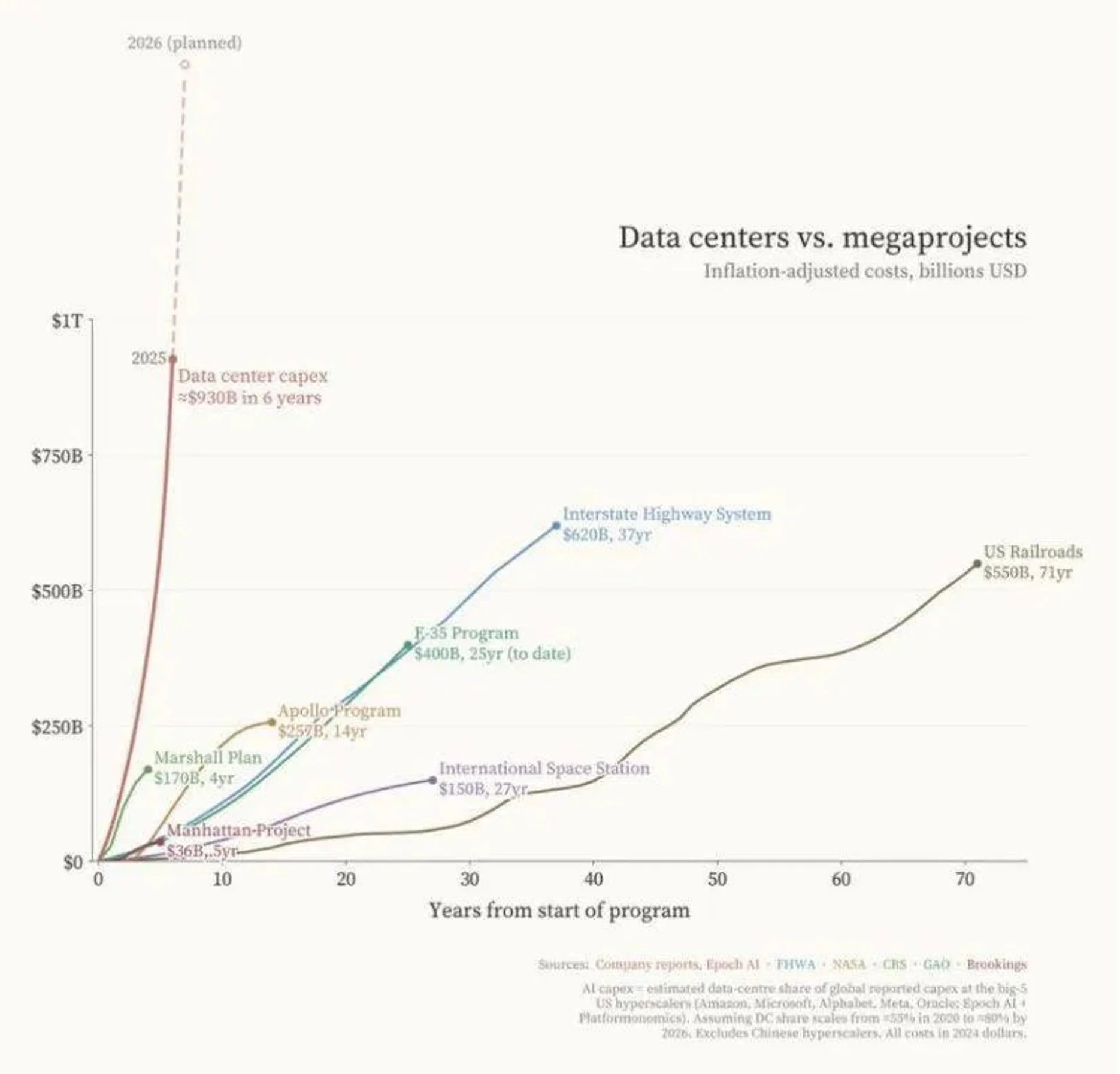

Except now we got a NEW chart that drives the point home even more! It’s THIS chart-

The chart is from this tweet. Which is from likely the most market-moving Twitter account in the entire AI Value Chain trade. Extremely influential account. And that tweet did numbies-

To explain the new chart, first off, it’s a lot like the previous Morgan Stanley chart. The historical numbers are bit different because of fiscal YE’s, but the point is the same. The new chart is consensus estimates, which are low compared to Morgan Stanley (and there’s also prob a bit of CY/FY difference).

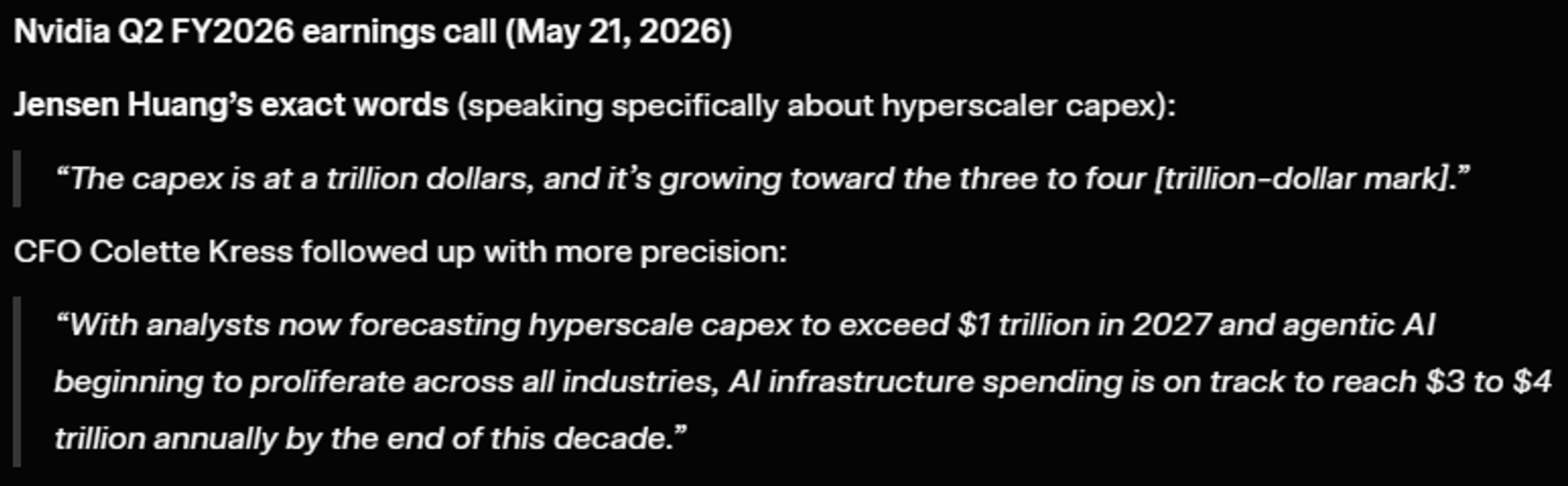

So the new chart introduces us to 2028 consensus capex numbers. And then there’s a massive 2030 $4tn number labeled “Huang’s Prediction”. This is straight from NVDA’s earnings call on May 21st -

Source: Grok. As of 5/31/26.

That explains the big grey bar on the chart. Jensen and Colette both said $3-4tn in 2030. And the author used $4tn for dramatic effect (or perhaps because the author is expecting closer to $4tn). It is a fact that Jensen is incentivized for his customer’s stock prices to be high. Everything works better when customer stock prices are up and to the right. So he’s incentivized to say a big number on the capex.

This is the #1 point I want to make- if the grey bar is even $2tn, these stocks really should keep working for a while. Forget $4tn. It might be $4tn, but that’s upside. $4tn. $3tn. It’s upside. If it’s even $2tn, these AI Value Chain stocks should keep working through the rest of 26 and probably all of 27 and potentially into 28.

The 2022-2025 CAGR on the Jensen capex chart is 34%. The expected growth rate in 2026 is 100%. So that’s what the market has been pricing in recently and is continuing to price in as we speak. The consensus 27 capex growth is 20%. But that number is quite likely to end up higher than $904. It will likely be north of $1tn and maybe north of $1.2tn. That’s my gut feeling.

And then the consensus 28 capex growth is 14%, but again that is likely low. That $1tn 28 number is prob closer to $1.5tn, up from probably $1.2tn in 27. That’s 25% capex growth in 28.

Then we skip 2029 on the graph and jump straight to the $4tn 2030 prediction number. Again. That’s icing on the cake. Call it $2tn. The CAGR from $1.5 to $2tn over two years is 15%.

It is true that stocks, especially momentum stocks, trade on the future expected rate of range of the rate of change. But if Hyperscaler capex doubles in 2026 and then grows at 25% for two years and then grows at LEAST 15% in 29 and 30, it would not make sense to me that the AI Value Chain trade would top in 26 or even 27. That capex growth translates to earnings growth for the companies that have Hyperscalers as customers. That’s what I mean when I say “AI Value Chain” – you’re downstream from this historic level of capex spend.

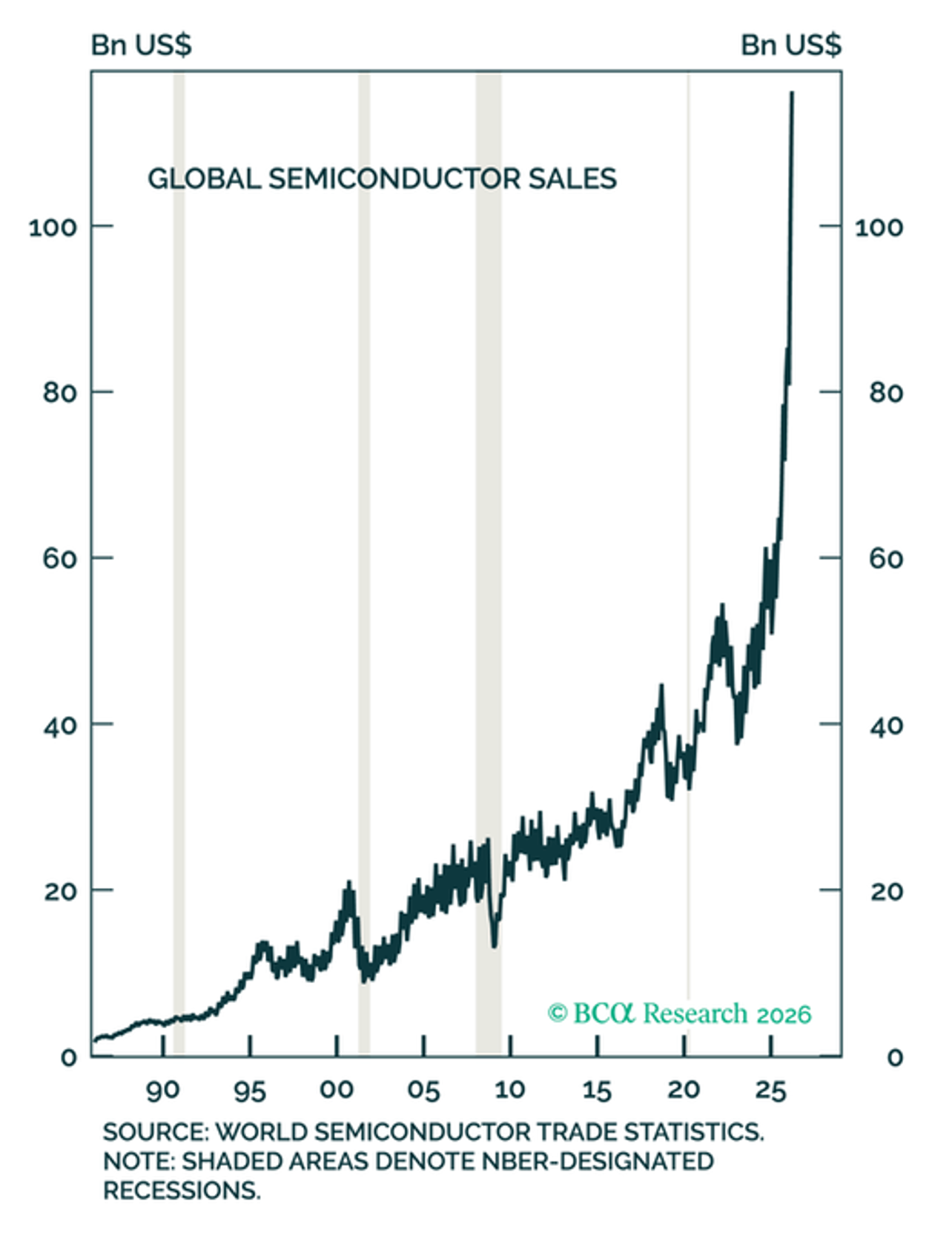

And capex spend is historic-

Source: @finmoorhouse. As of 5/17/26.

So I show you the Jensen chart and I say-

“those are some really big numbers that are growing really fast”.

And you say-

“how fast are they growing on some sort of relative basis?”

And then I show you that railroad chart. And I say-

“turns out it’s definitely the most aggressive ramp in capex in US history. And it very well might be the largest overall capex program in human history. It also might be the LAST capex cycle humanity ever has – no not because the robots are going to destroy humanity (right??). It’s because if done right, AI + robotics will likely solve global scarcity, and the concept of a capex cycle will fade away over the next couple centuries.”

So yeah. I think this is potentially a generational or once-in-a-species investment opportunity. Seriously. No it’s not going to move like crypto in 2021 (perhaps a few exceptions). These are real companies that do real things and the markets they trade on are not saturated with frauds and scams and manipulation like crypto. But this AI Value Chain could be one the most attractive R/R opportunities you could ever ask for over the next 12-24 months.

There are, of course, very real risks to that outlook. Any number of macro risks, like there always are. But also layers of idiosyncratic risk – at the company level, sector level, technology level, etc.

But in a lot of ways, the risk all boils down to that Jensen chart. Is that chart going to deliver those numbers? That is another unique aspect of this trade. It all seems to boil down to whether those capex numbers show up. If they do, it is quite likely that the best-positioned companies will perform very well over the next couple years. Not every company, of course. There will be winners and losers, of course. But the overall index (eg, QQQ, SOXX, DRAM) will perform well and the biggest winners will put up incredible returns.

As mentioned last month, the biggest risk to the Hyperscaler capex story is Hyperscaler ROIC. As such, this is a topic of great discussion in the market. And it feels like it will be the acute point of risk to the entire AI Value Chain trade. If sufficient Hyperscaler ROIC shows up, the downstream names will likely work, probably for years.

The main deciding factor for whether Hyperscaler ROIC shows up is whether Hyperscaler customer ROIC shows up. The end user (which is overwhelmingly enterprise) has to see that it’s worth their while to spend money with the Hyperscalers – one customers spend is another customers ROIC is another customers spend is another customers ROIC. But the top of the funnel is whether Hyperscaler customers are seeing their money’s worth and want to grow their spending.

So the market is going to be laser focused on this setup. And because so many AI Value Chain names have run so hard already, they are vulnerable to whippy pullbacks at any moment. Any whiff of a hiccup in Hyperscaler capex ROIC will aggressively ripple through these high-flying charts. It’s really easy for a name that’s +300% in six months to pull back 40% really quick.

There will be hiccups along the way, for sure. Some will be scarier/more consequential than others. But I think in general you gotta be ready to buy the dips in the coming weeks, months and quarters. The macro dips will be the easiest to buy. Obviously if the macro risk is big enough and real enough, it could crash all stocks, including AI Value Chain. But look at what just happened. You just took 20%+ of global seaborne crude/LNG and 30% of global seaborne ferts off the market and QQQ is +24% from PRE-IRAN levels.

The market is showing you how ravenous it is for this AI Value Chain exposure. SOXX is +54% from pre-Iran levels. MU is +130% from pre-Iran levels. That’s how hungry the market is for this exposure. And those two charts I shared above (Jensen + Railroad) are the reason why.

Perhaps you have heard of the term “atoms over bits” or vice versa. Everyone has been arguing about bits over atoms vs atoms over bits. I think you want to own the atoms that make the bits. It seems like that may be where the most earnings torque is.

And lemme tell you, there is serious earnings torque in this trade.

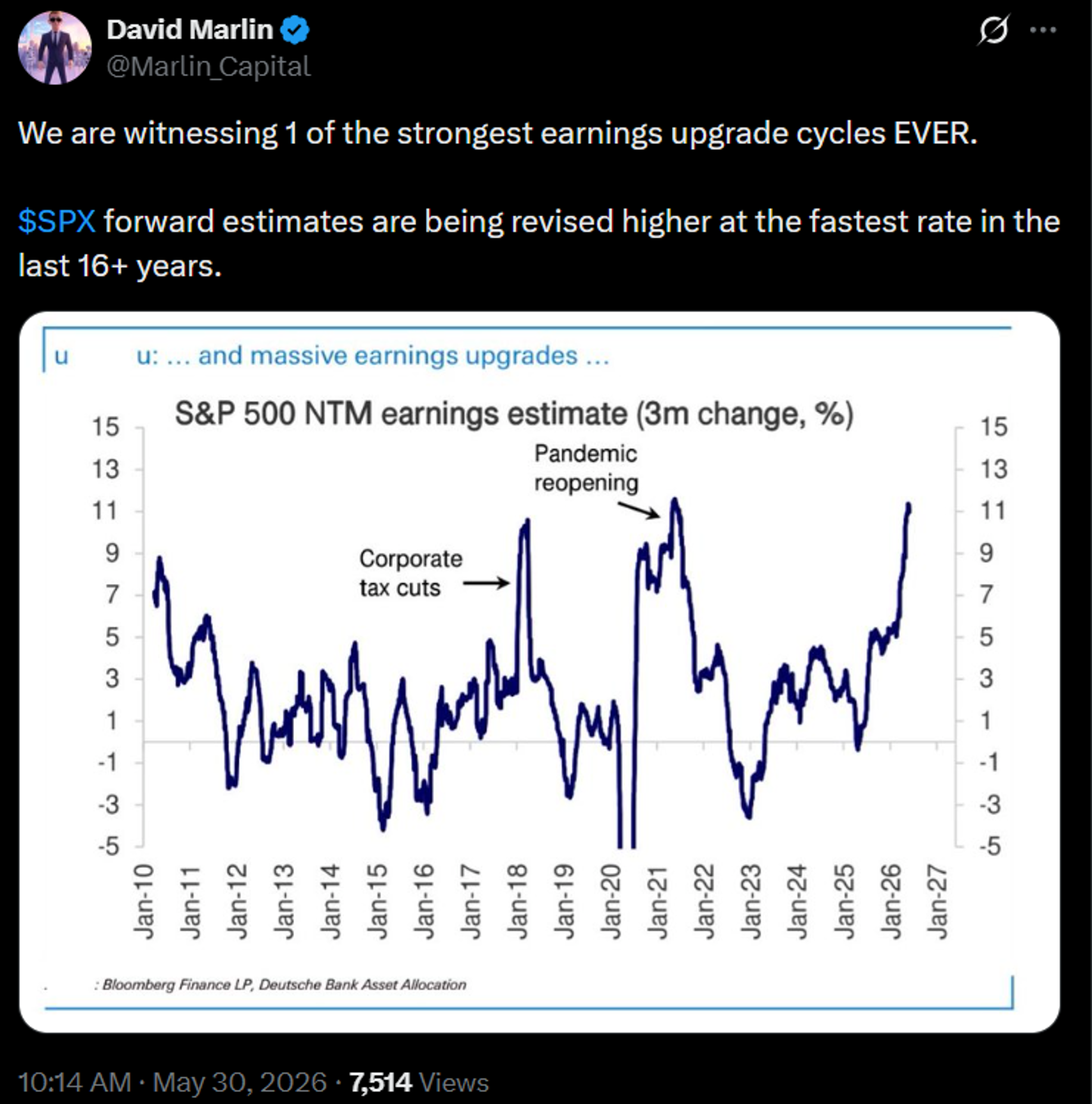

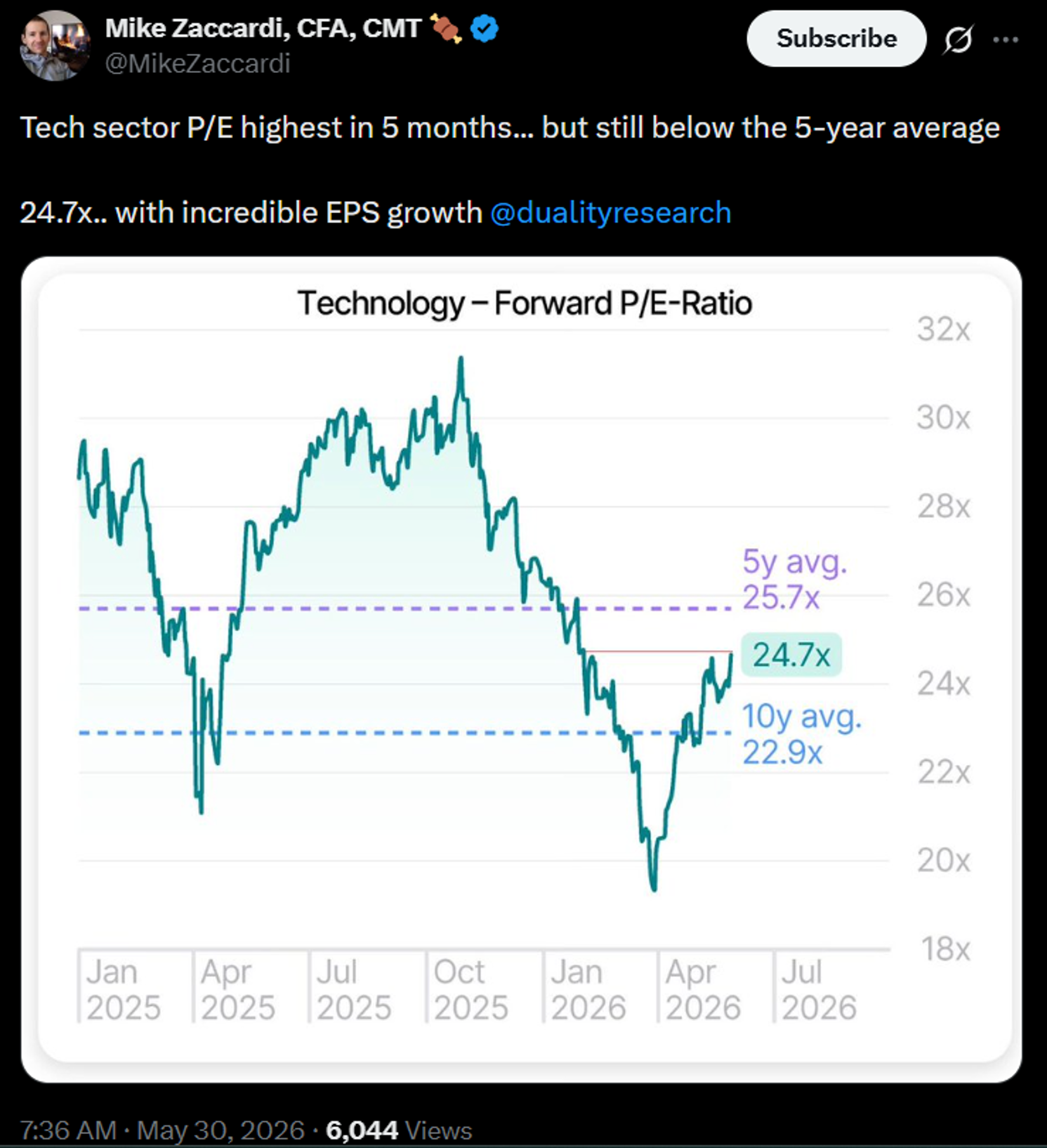

People have been using the term “earnings bubble”. It’s not a “valuation bubble” - where the P/S and/or P/E look totally insane. It’s an earnings bubble – the multiples look cheap now because you’re pricing them on peak earnings. And they won’t look so cheap on numbers 3+ years out because earnings will peak in year 2 (or some version of something similar to that thesis).

Earnings bubble might look like this-

Another look at what might be an “earnings bubble” –

And another look. Is that a “bubble”?

It all leads to a question about the durability of future earnings and earnings growth. This will play out in the markets in the coming years and trillions will certainly shift because of it. The AI Value Chain would FAR AND AWAY be my leading candidate for the most interesting public market in the next few years. Honestly, how could it not be?

P.S. – I forgot this part. You could ask yourself the question – does the US Govt think that winning the AI/compute/chips/robotics/space/defensetech/biotech/etc/etc races are a matter of national security? Yes or no? The answer to that question should help inform how you feel about the durability of the Hyperscaler capex.

Market Update— Liquid Markets Investing

| Name | May | Apr | Q1-26 | YTD | Q4-25 | Q3-25 | Q2-25 | Q1-25 | 2025 | 2024 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|

| S&P 500 | 5% | 11% | -5% | 11% | 2% | 8% | 11% | -5% | 16% | 23% | SPX |

| NASDAQ-100 | 11% | 16% | -6% | 21% | -6% | 2% | 18% | -8% | 20% | 25% | QQQ |

| Magnificent Seven | 7% | 14% | -12% | 7% | -4% | 12% | 23% | -8% | 29% | 42% | MAGS |

| Bitcoin | -3% | 12% | -22% | -16% | -23% | 6% | 30% | -12% | -6% | 121% | BTC |

| Ethereum | -11% | 7% | -25% | -28% | -28% | 67% | 36% | -45% | -11% | 46% | ETH |

| Solana | -1% | 0% | -32% | -33% | -35% | 48% | 42% | -52% | -19% | 312% | SOL |

| BNB | 4% | 0% | -18% | -14% | -14% | 53% | 9% | -14% | 23% | 124% | BNB |

| Hyperliquid | 70% | 24% | -28% | 52% | -22% | 81% | 67% | -38% | 45% | n/a | HYPE |

| Aggregate Mkt Cap | 5% | 11% | -21% | -8% | -24% | 16% | 24% | -19% | -11% | 136% | TOTAL |

| Aggr Alts Mkt Cap (ex top-10) | -5% | 4% | -25% | -26% | -24% | 34% | 25% | -34% | -16% | 72% | OTHERS |

| Semiconductors | 23% | 40% | -10% | 55% | -8% | 15% | 28% | -12% | 32% | 49% | SOXX |

| Expanded Tech Software | 21% | 5% | -5% | 21% | -3% | 9% | 16% | -7% | 19% | 22% | IGV |

| ARK Innovation (disruptive tech) | 8% | 12% | -18% | -1% | -11% | 25% | 31% | -23% | 19% | 38% | ARKK |

| Robotics & AI | 4% | 16% | -12% | 7% | -8% | 19% | 22% | -15% | 15% | 30% | BOTZ |

| Quantum Computing | 18% | 25% | -10% | 33% | 7% | 38% | 59% | -31% | 88% | n/a | QTUM |

SOURCE: GROK. AS OF 5/31/26.

Yeah stocks absolutely ripped in May. Tech stocks especially. Crypto did not rip. Crypto traded quite weak throughout the month and that trend continued on June 1st.

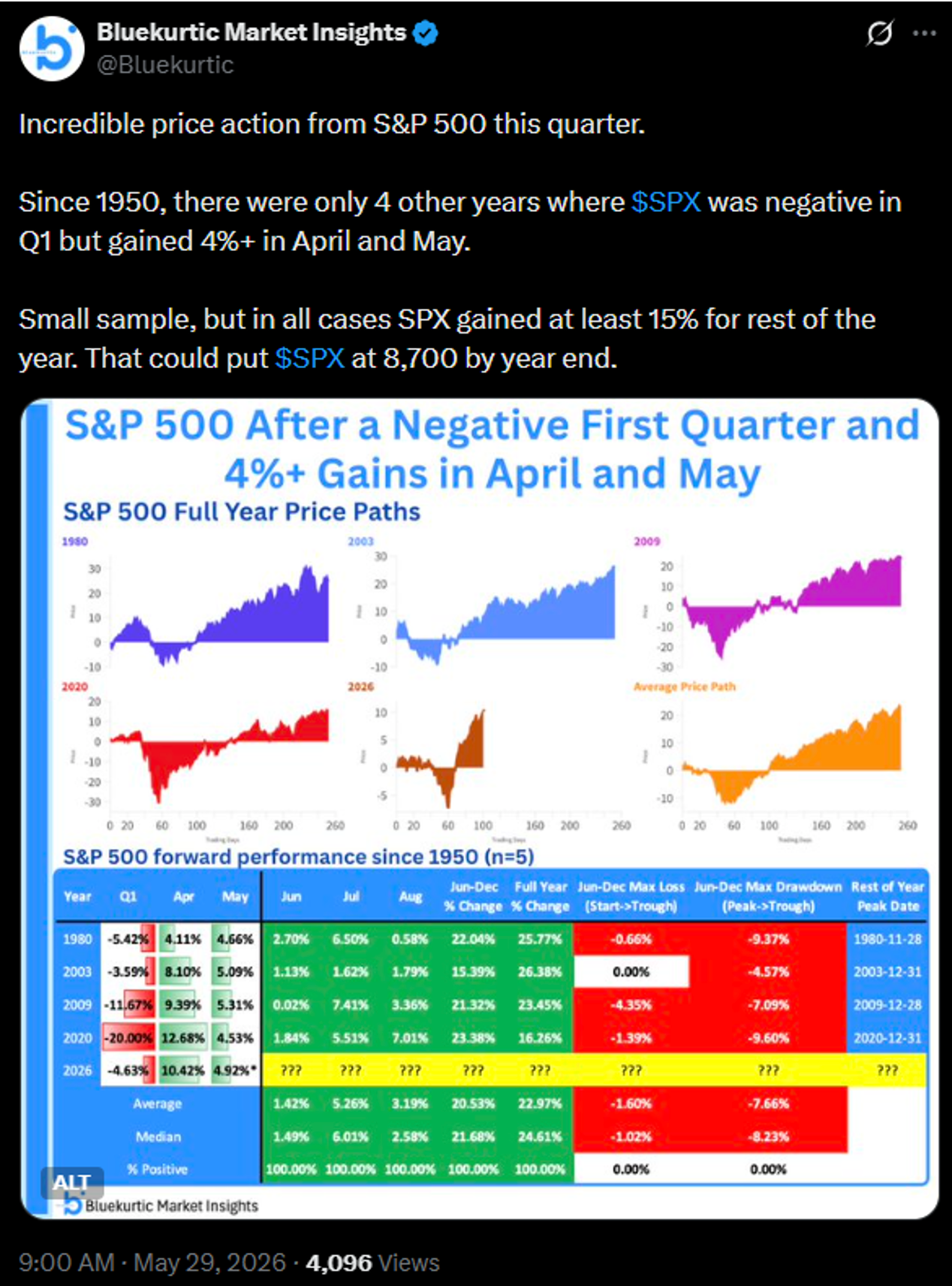

In last month’s letter, I showed you a bunch of seasonality charts that drove home the point that when the market acts like it did through April, the forward returns were historically very strong. Well now we have another month of price action, which was insanely strong. So we have some more seasonality charts, with another month of data-

Small sample size, but compelling-

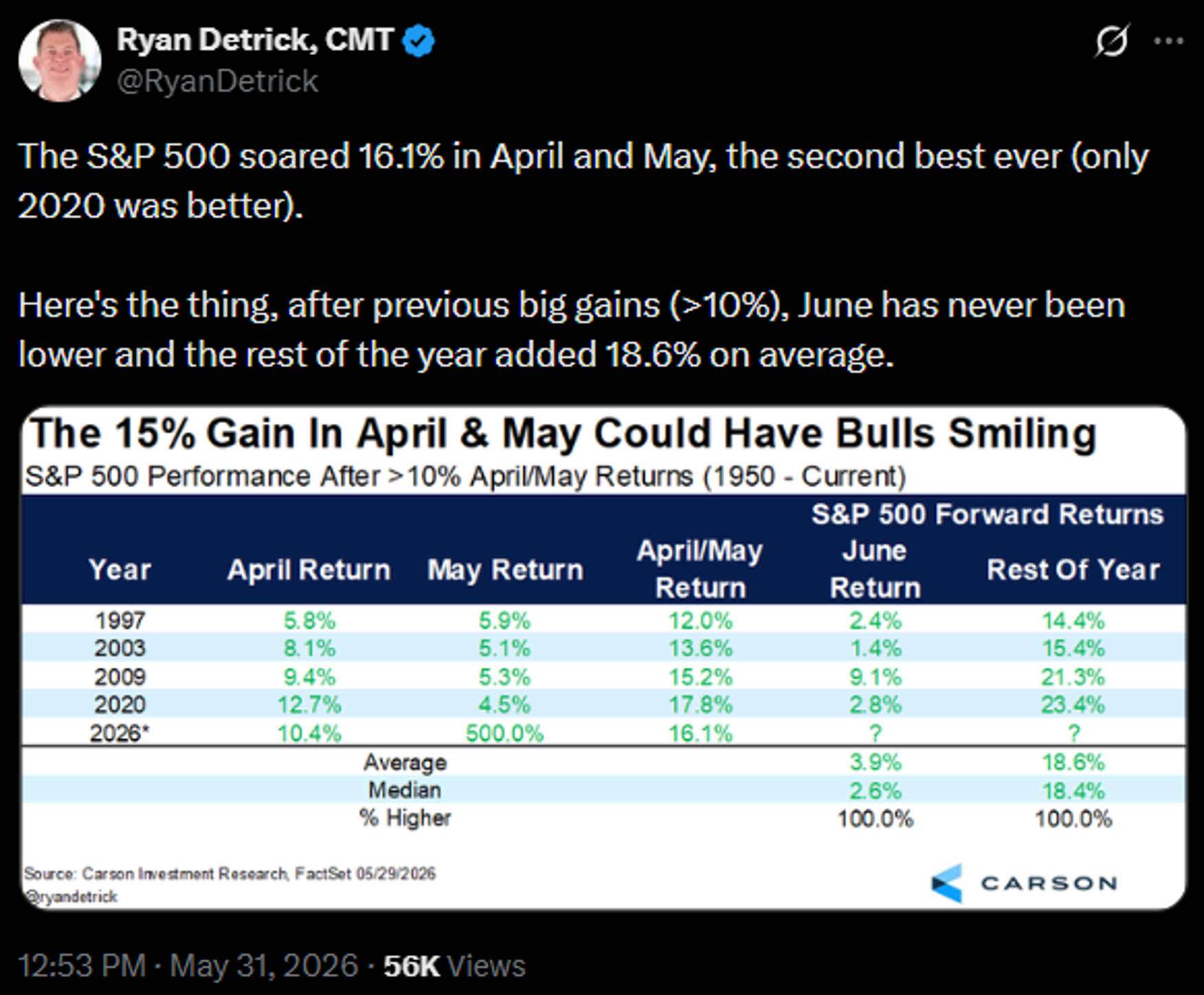

Somewhat similar look. Again, small sample size but typically very strong June and ROY returns-

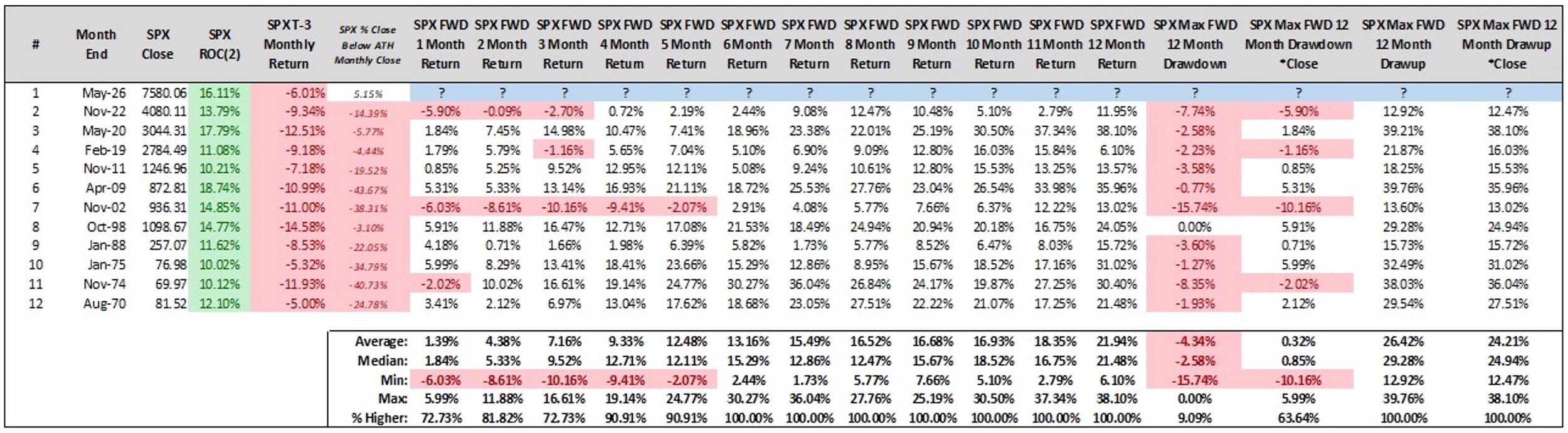

Again, another similar look. This highlights strong price thrust reversals. Below is every instance where the SPX was +10% in two months after down >5% in the month prior. Very strong forward returns-

Source: @SJD10304. As of 5/29/26.

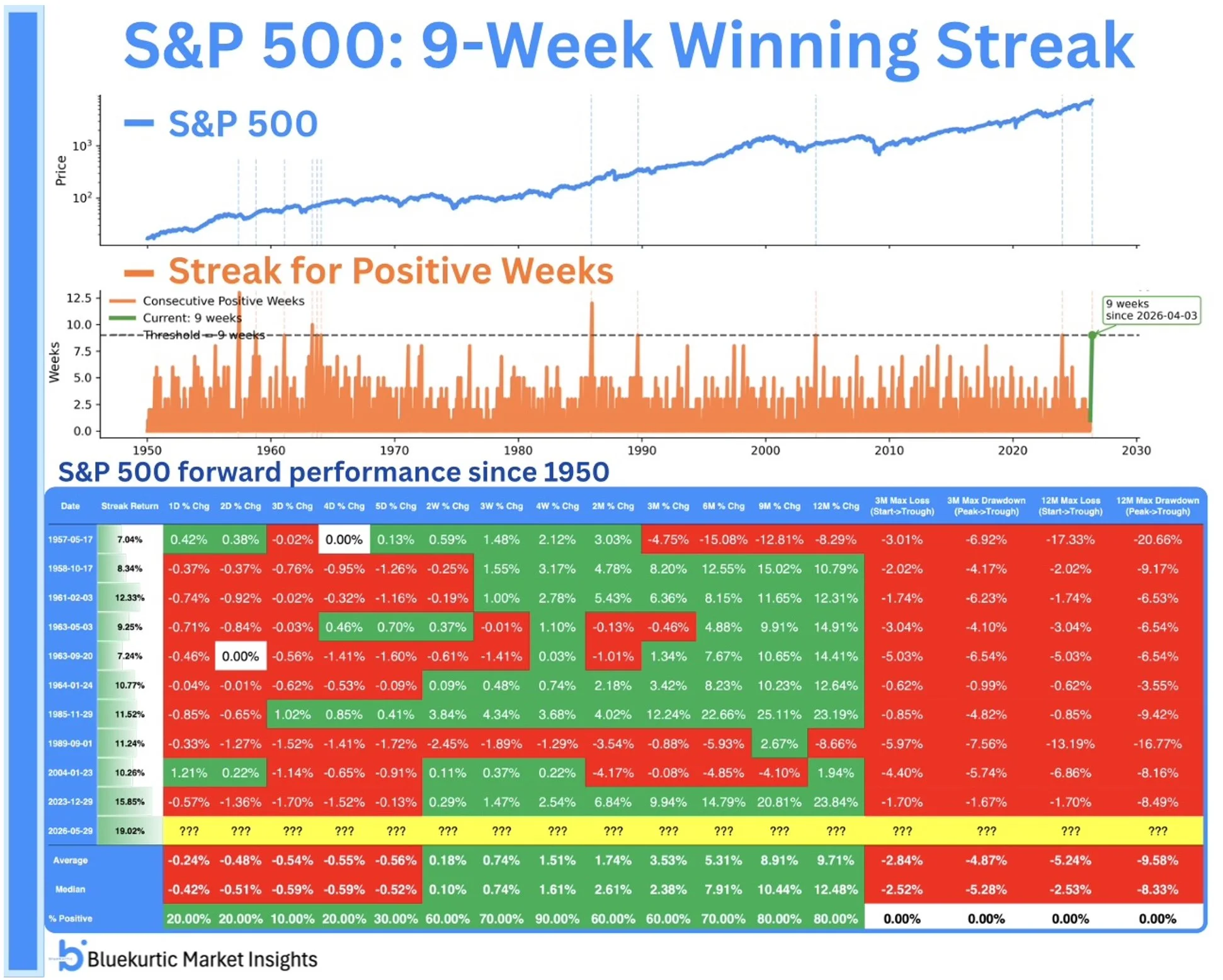

The SPX just posted 9 consecutive positive weeks. This is rare. When looking at the forward returns of other 9-week winning streaks, they are typically pretty strong-

As of 5/30/26.

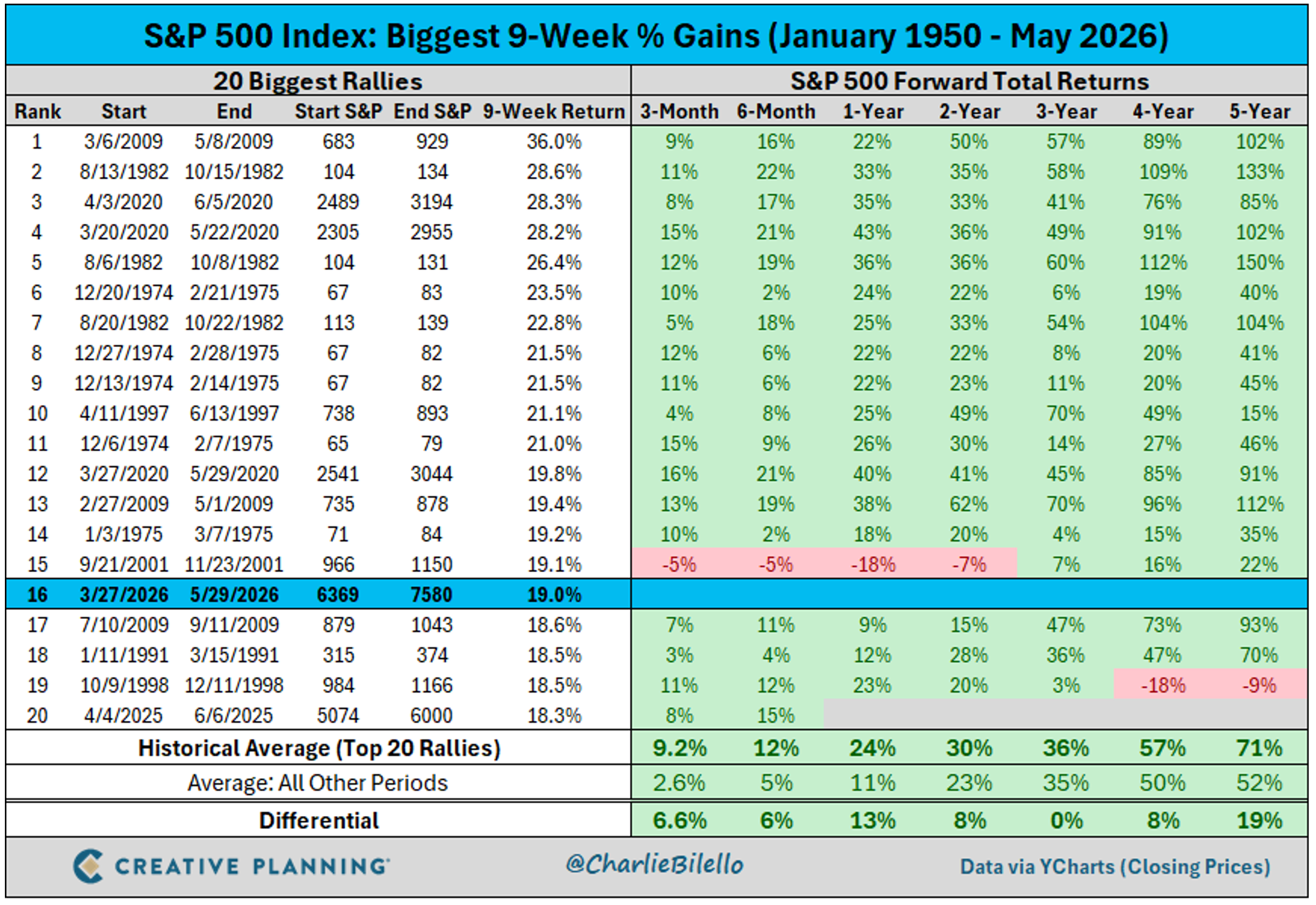

Here’s a similar way to look at it. We just finished the 16th strongest 9-week total SPX performance ever (not just 9 consecutive positive weeks, like the last chart). Below is a chart of 20 largest 9-week SPX gains ever. You see that typically the forward returns are very strong-

As of 5/29/26.

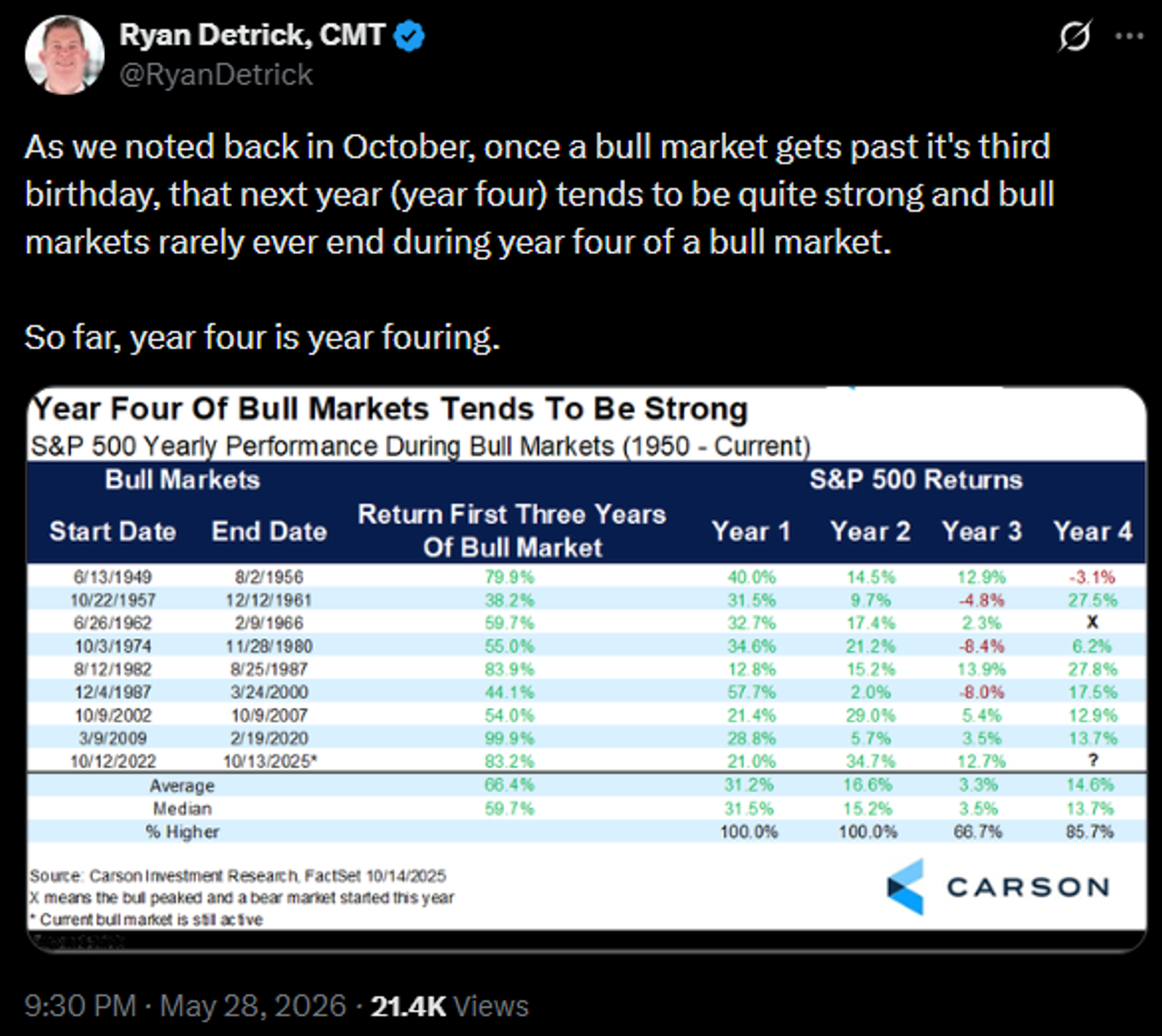

If a bull market makes it to its fourth year, the returns are typically strong –

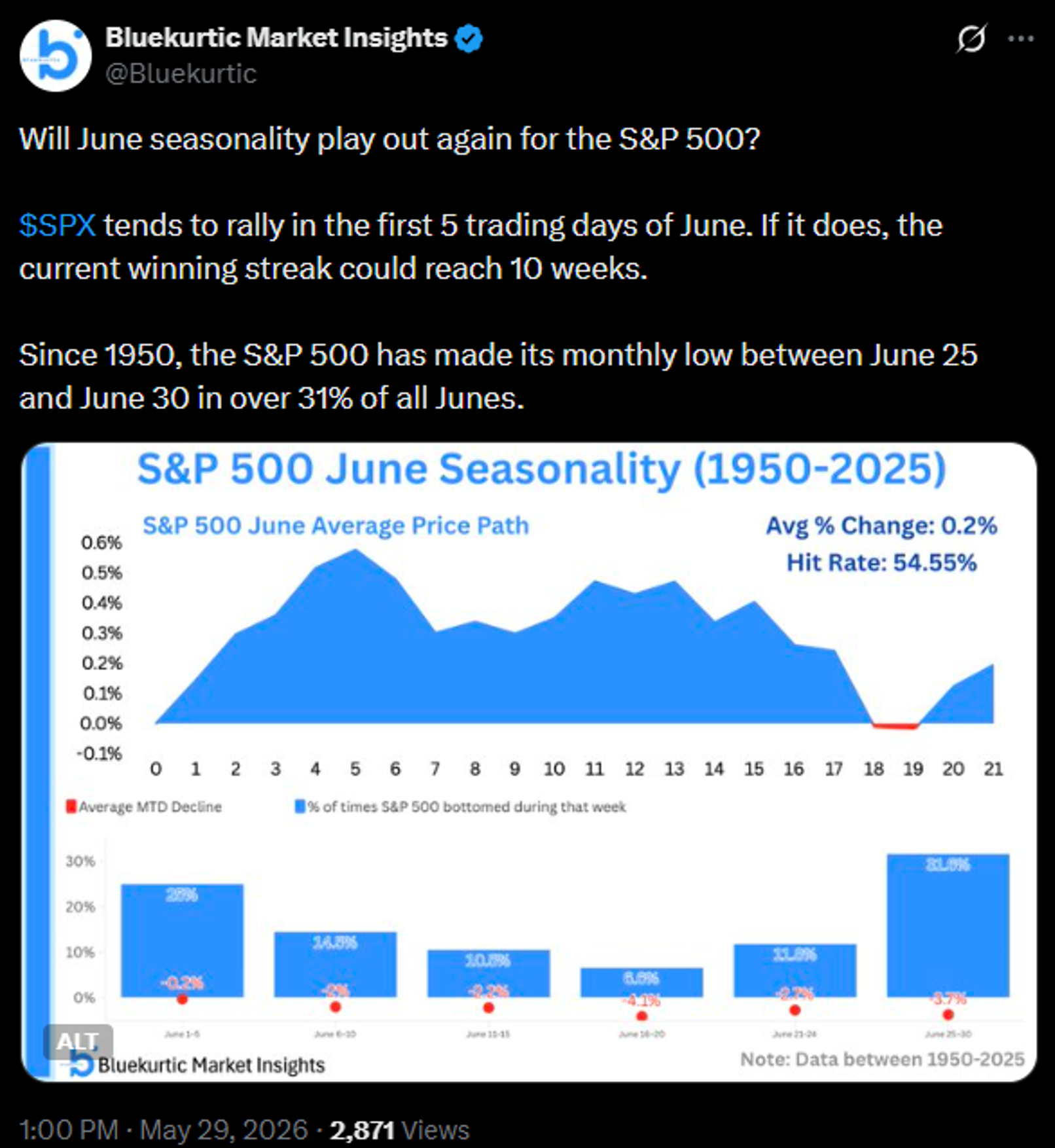

In the very near term, SPX has been positive 9 of the last 10 Junes. Historically, June tends to be strong at beginning of the month and top at the end of the month-

So. ALL of that to say, I think you want to be in dip buying mode unless something big changes. And a dip could come at any time for little/no reason, if for no other reason than these stocks have run INSANELY hard in the last two months.

QQQ is +33% from the 3/30 lows (remember the market bottomed a week before the ceasefire came). All gas no brakes. Price is currently 11% above the 50DMA-

Source: TradingView. As of 6/1/26.

So that’s just insanely strong performance. SOXX is even more extreme-

Source: trading view. As of 6/1/26.

Semiconductors, in many cases, are pretty fully valued here. On 27 consensus EPS, they look pretty full. But that 27 EPS number could be too low by…10%? 25%? 50%? And then looking into 28, you could still see another strong double digit % EPS growth Y/Y. And maybe that % EPS growth continues all the way through 2030. That’s how these stocks start to look not all that expensive. And if you can get them on a pullback, say at the 50D or 100D, they might look flat out cheap on 28 P/E at that point. Those are the types of entries I’m begging for.

MU we discussed in more detail last month. It was up 90% in May lmao. It is now a $1.2tn market cap company. This is the chart-

Source: TradingView. As of 6/1/26.

And it still trades at like 8x 27 P/E.

Software had a huge month. +23% and a continuation of the strong bottom and reversal that started in April. One of the more unique and interesting chart setups in tech-

Source: TradingView. As of 6/1/26.

This has the hallmarks of a short squeeze and there is short interest data out there to support that view. It’s only another +10% from here to get to new ATH. Shorts may have to keep scrambling to cover.

MAGS (Mag7) is a different looking chart than these highfliers-

Source: TradingView. As of 6/1/26.

MAGS underperformed QQQ off the Iran lows, and only sits 1% above pre-Iran highs. Seems like MAGS is being somewhat ignored or just less aggressively bought than many names downstream of them in the AI Value Chain. That makes intuitive sense to me.

I think MAGS might also be lagging some because of the upcoming SpaceX IPO (currently scheduled for June 12th). Gotta make room for the new big dawg. There is some chance this IPO puts in a temporary market top. I will be watching closely for that.

Last month we talked about NBIS as the best-in-class datacenter operator. This month, Leopold Aschenbrenner’s Situational Awareness fund, which is likely the most market-moving fund investing in the AI Value Chain today, announced a $2.6bn position in NBIS, representing 5.6% of the entire company and ~35% of Leopold’s total long equity exposure. It’s a MASSIVE position.

NBIS chart looks like this-

Source: TradingView. As of 6/1/26.

There is a subsector of semis called power semis. Some of them have exposure to what has been dubbed the “800V transition theme”. One of the most pureplay ways to get exposure to this theme is through a $2bn mkt cap ticker WOLF-

Source: TradingView. As of 6/1/26.

WOLF is an interesting situation in part because it went bankrupt in 2025. It had a bunch of legacy automotive/EV assets and businesses that weren’t doing well. And then as it turns out, that same underlying technology now looks like it’s going to be super important for datacenters. There’s a ton of risk on this one, and it could not work for all sorts of reasons.

And now to crypto. As of the afternoon of June 1st, BTC and crypto look very weak-

Source: TradingView. As of 6/1/26.

For BTC you had a very clear failure at the 200D (yellow). You had no support at the 50D or 100D. You did not have support at prior range highs from March. And now you’ve accepted back into the prior range established since early Feb.

I don’t really see a strong reason technically why this shouldn’t go back to the bottom of the range - $60k or low $60s. There is some support in that white box but I don’t think it’s a lot. By the time we get down to the low $60’s, price will be quite oversold. So I don’t get the sense that BTC has the downward momentum right now to immediately go break down to new lows. It probably chops that range low for a bit, let the oscillators reset some, and then eventually breaks down.

The BTC weekly chart looks worse than the daily. The weekly looks like it does actually have room to break to new lows before much of a bounce-

Source: TradingView. As of 6/1/26.

ETH is in worse shape than BTC-

Source: TradingView. As of 6/1/26.

Say what you want about TA, but that was a pretty textbook rising wedge (white channel). And when it fell out, it responded in a textbook way. Looks like $1500-$1600 is the next level. It might take a couple months to get there. If Clarity Acts doesn’t pass, it probably gets there sooner rather than later.

Last month I said SOL looked the worst out of the big three. It still looks bad-

Source: TradingView. As of 6/1/26.

That white circle is not a confidence-inspiring structure. $64 is the cost basis for a lot of the FTX locked SOL that got sold out of BK. I could see SOL finding at least some amount of support around that level.

Lastly, we have HYPE. Truly bucking the trend-

Source: TradingView. As of 6/1/26.

+87% in a couple weeks. And you see the volume trend there (that is Bybit spot). HYPE got two ETFs and a DAT called PURR recently. The ETFs have seen more than $100mm of inflows. The DAT initially started with ~$500mm of HYPE tokens and $300mm of cash in exchange for PURR shares. They have been spending that cash to buy HYPE. And the DAT has been raising additional proceeds through equity issuance.

So HYPE has been trading REALLY well. Perhaps if tech stocks weren’t going absolutely bonkers, I might feel some amount of FOMO on this. But as it stands, I have no FOMO.

Closing Remarks

I have been really busy lately. The market has been taking up a lot of my attention. I have been trading more actively than any point since before FTX collapsed. And I have been spending a ton of time researching tech stocks as well, which has been easy to do because it’s fascinating and a compelling opportunity.

I also dedicate a lot of time to Things Hidden. We release new long-form episodes every other Thursday and we’ve been on that cadence for a year. In fact, next week is the one-year anniversary of Things Hidden launching.

The episodes so far have all been solo episodes (we will start having guests soon). And I pour a lot of effort into them. On average, the episodes take about 40 hours of focused effort to prepare. It is a wonderful labor that I am blessed to do. But 40 hours an episode is 40 hours an episode.

I’m also a husband and a father to an 18-month old daughter. And they are far and away the best things that have ever happened to me, and the best parts of my life. So I want to spend as much time as possible with them.

I say all that to say, when I sat down to write this letter, I was tired and pretty burnt out (short term burnt out not like long term burnt out). These letters take me 8-12 hours of focused effort a month to produce. TBH, it really didn’t feel like a massive priority to me this month to write this letter. To spend those hours. And I think that was the first time I’ve felt that way about sitting down to write this letter. Sure, there have been months past when I wasn’t in the MOOD to write the letter, but it always felt like a high priority. Does it feel like that now?

That got me thinking about the purpose of this letter, both for me and for you. The purpose has been changing in real time and that’s a good thing. A necessary thing. And it might continue to change. I may look to figure out a format that maybe cuts my hours in half on this. Or I might move to a quarterly letter.

Or I might just keep finding compelling things to write about every month that still takes 8-12 hours of focused work. Because I will say, this month, it wasn’t a hard decision to write what I did. I had something I wanted to say and I said it. But as I mentioned last month, slanging tech stocks is something altogether different than investing in, and being a public proponent of, the ideology of decentralization.

In any case, I appreciate you taking this journey with me through this letter. I know some of you reading this right now have been reading these for many years. What a ride it has been! We’ll see where it takes us.

“Regret does not come first.”

-Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2023 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS