March 2026 - Monthly Market Update

/Monthly Update || March 2026

“Every great money manager I’ve ever met, all they want to talk about is their mistakes. There’s a great humility there.”

Opening Remarks

Greetings from Ikigai Asset Management¹. We welcome the opportunity to bring to you our ninetieth Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that has tremendous potential to make the world a better place and create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to do our part to push crypto towards fulfilling its potential. We strive to be an objective, reasonable, well-intentioned voice of truth amongst a chorus of biased, fallacious, pernicious opportunists. It’s an honor that we take seriously.

To that end, crypto prices were decidedly lower in February, a continuation of the weak price action in January which was a continuation of the weak price action from Q4. I ended last month’s letter with this warning –

“Wish I had better news for you, but I don’t. If you were looking to deploy additional capital into crypto in the near term, I’d wait for lower prices. I really doubt this thing runs away from you.”

That played out pretty aggressively in Feb: BTC -15%, ETH -20%, SOL -20%. YTD BTC/ETH/SOL are down 23/34/32%.

This ugly price action in crypto occurred with a relatively subdued traditional markets backdrop. Stocks were down marginally (albeit with significant rotation under the indexes). Gold and silver were up 8% and 10%. VIX about flat. Yields a bit tighter. The crypto weakness was pretty much contained to crypto.

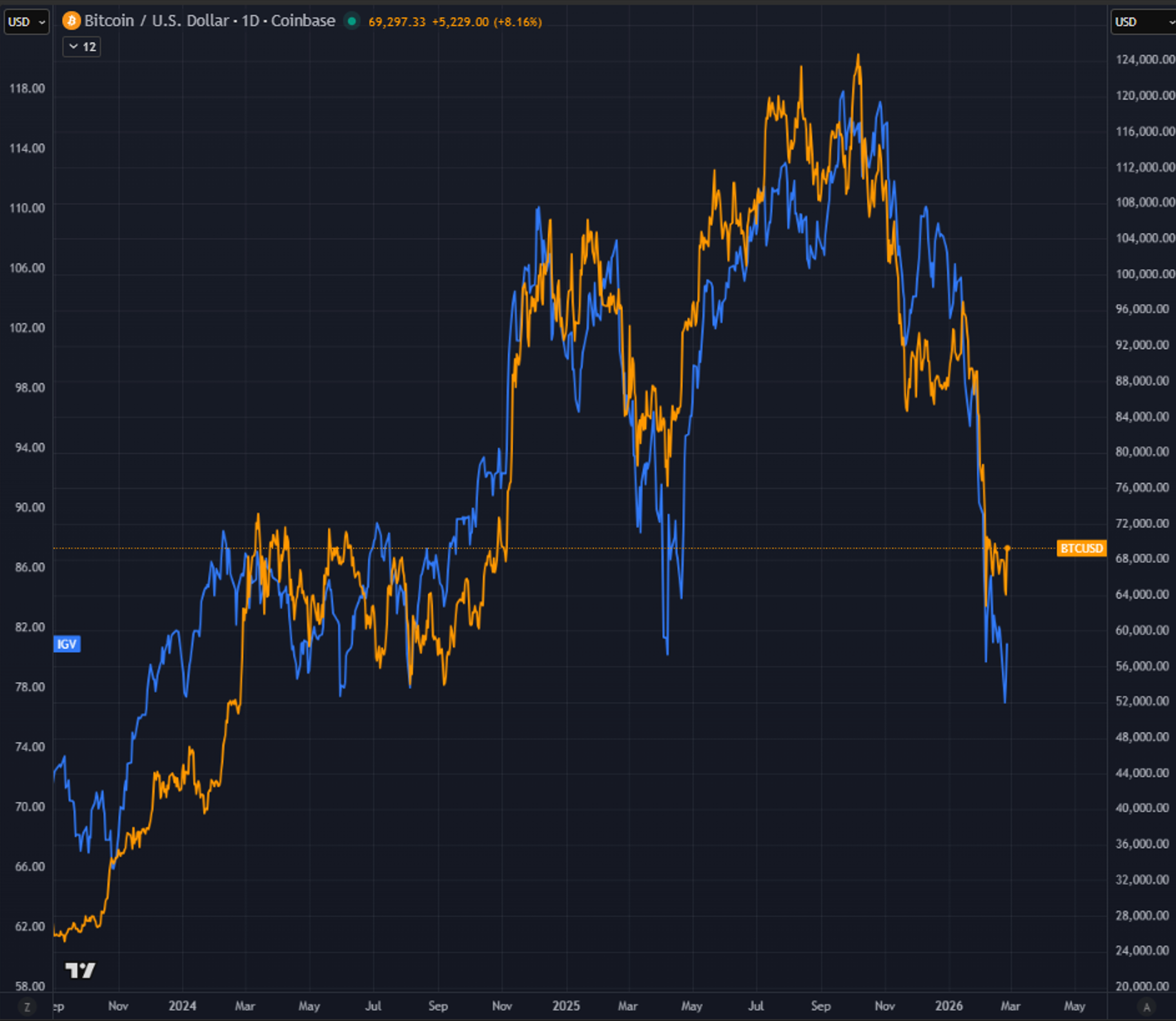

There is one particular traditional market correlation that has been getting a lot of airtime lately-

Source: TradingView. As of 2/26/26.

That is BTC in orange and the software ETF IGV in blue going back 2 ½ years. There has been lots of conjecture about this chart recently, for obvious reason. IGV holds names like MSFT, PLTR, ORCL, CRM, PANW ADBE, APP, INTU. These names have come under pressure in recent months as AI fears have gripped the market – with investors questioning the long-term durability of any software’s moat against the breath-taking advance of LLMs.

So is the market telling us that BTC is basically software? Well, it is software. But it certainly isn’t software like these other companies have software, right? You could argue that it’s spurious correlation. Or you could argue BTC and IGV have both represented speculative, frothy, momentum type of market factors, even though the underlying fundamentals are quite different. Whether BTC and IGV will continue to trade together in the coming months, I don’t have a strong view on. But one thing we can say for certain, BTC has not been trading like “digital gold” –

Source: TradingView. As of 2/26/26.

Physical gold has been trading like the world is revaluing the US dollar and US treasuries. “Digital gold” has been trading like it has a quantum problem and probably a DAT problem, both of which will likely take time to play out.

February Highlights

Kyle Samani Leaves Multicoin Capital, Tushar and Team to Continue Operating

Crypto Lender “BlockFills” Halts Withdrawals, Rumors of $75mm Loss and Rescue Financing

Fortune Reports Binance Firing Top Compliance Investigators Who Uncovered Evidence of Iranian Sanctions Violations

US Senator Blumenthal Opens Federal Inquiry Into Binance Noncompliance Claims

Forbes Reports 87% of WLFI’s Stablecoin USD1 Is Held on Binance, Immediately After Trump Pardoned Changpeng Zhao

RobinHood Launches Public Testnet of L2 Blockchain

MSTR Buys $373mm of BTC in Four Tranches

BMNR Buys $273mm of ETH in Three Tranches

BTC ETFs See $207mm of Outflows

ETH ETFs $370mm of Outflows

CFTC Chair Selig Announces CFTC’s Sole Oversight of Prediction Markets, Prepared To Fight States In Court Over Gambling Laws

ZachXBT Reveals On-Chain Evidence of Insider Trading at Axiom Exchange

Dragonfly Raises $650mm Fourth Venture Fund

Tether Announces $100mm Strategic Equity Investment in Anchorage Digital

DBA Crypto VC Fund Announces $62mm Fund II

Jump Trading Receives Equity Ownership in Polymarket and Kalshi in Exchange For Market Making Service

OpenAI Partners With Paradigm To Launch “EVMBench”, AI Agent Smart Contract Tool

Crypto.com Receives Conditional OCC Approval To Become a Bank

Netherlands Bans Polymarket Over Illegal Gambling Services

| Asset Class | Feb | Jan | YTD | Q4-25 | Q3-25 | Q2-25 | Q1-25 | 2025 | 2024 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | -15% | -10% | -23% | -23% | 6% | 30% | -12% | -6% | 121% | BTC |

| NASDAQ | -2% | 1% | -1% | 2% | 9% | 18% | -8% | 20% | 25% | QQQ |

| S&P 500 | -1% | 1% | 0% | 2% | 8% | 11% | -5% | 16% | 23% | SPX |

| Total World Equities | 2% | 3% | 5% | 2% | 8% | 10% | -1% | 20% | 14% | VT |

| Emerging Market Equity | 6% | 8% | 14% | 2% | 11% | 10% | 4% | 31% | 4% | EEM |

| Gold | 9% | 12% | 22% | 11% | 16% | 6% | 19% | 64% | 27% | GLD |

| High Yield | 0% | 1% | 0% | -1% | 0% | 3% | 0% | 3% | 2% | HYG |

| Emerging Market Debt | 1% | 0% | 2% | 1% | 3% | 2% | 2% | 8% | 0% | EMB |

| Bank Debt | -3% | -1% | -4% | 0% | 0% | 1% | -2% | 0% | -1% | BKLN |

| Industrial Metals | 1% | 5% | 5% | 12% | 4% | 3% | 2% | 22% | 3% | DBB |

| USD | 1% | -1% | -1% | 0% | 1% | -7% | -4% | -9% | 7% | DXY |

| Volatility Index | 14% | 17% | 33% | -8% | -4% | -24% | 28% | -14% | 39% | VIX |

| Oil | 3% | 15% | 18% | -6% | 1% | -5% | 2% | -8% | 13% | USO |

SOURCE: TRADING VIEW. AS OF 2/28/26.

AI Doom or AI Boom?

In the first two months of 2026, we have seen a host of “thought pieces” about the future of AI and the implications for markets and society as a whole. Many of these posts have gone very viral. In particular the Citrini doomer piece, released 2/22, was cited across Wall Street for causing the market-wide downward price action the next day – including some aggressive downward price moves in several names that were explicitly mentioned (negatively) in the Citrini piece. That post has now been viewed tens of millions of times.

That caught my eye. An AI-doomer piece that was so widely circulated that it caused the stock market to go down the next day? As a humble “thought piece” generator myself (ninety and counting!), I found this to be interesting. And there were a bunch of others too that were also interesting.

So I’ve aggregated the major ones here for you, with short summaries and links to the original-

Citrini Research – “The 2028 Global Intelligence Crisis” – Feb 22. The most viral of them all. The authors depict a hypothetical scenario where AI agents precipitate a unique economic downturn by 2028, distinct from traditional recessions. They argue that AI's deflationary effect on intellectual labor could lead to cascading job losses in white-collar sectors, eroding consumer demand. The piece details a chain reaction involving reduced spending, corporate bankruptcies, and market crashes. It highlights the absence of natural stabilizers, as AI lacks the cyclical brakes of human-driven economies. The narrative incorporates timelines for technological milestones accelerating the crisis. Ultimately, it serves as a warning about unpreparedness for AI's societal impacts. Alarmist and speculative tone.

Ray Dalio – "AI, the Big Cycle, and Other Such Things" – Feb 14. 79mm views just on the X post. Carries less weight because he always writes this type of stuff. Dalio positions AI within the framework of historical economic cycles, suggesting it is currently in the nascent phase of a potential bubble fueled by excessive optimism. He draws analogies to past technological revolutions, noting how initial hype often leads to overinvestment and subsequent corrections. The essay explores AI's capacity to amplify productivity across sectors while exacerbating inequalities if not managed properly. Dalio emphasizes the interplay between AI advancements and broader geopolitical shifts, including U.S.-China dynamics. He advocates for adaptive policies to harness benefits while mitigating risks like job displacement. The piece concludes with reflections on how AI could reshape global power structures over decades. Cautiously skeptical tone.

Dario Amoedei – “The Adolescence of Technology – Jan 26. 6mm views on X. Amodei likens the current state of AI to a turbulent teenage phase, characterized by rapid growth and unpredictable risks. He outlines potential threats including widespread unemployment, enhanced cyber vulnerabilities, and deepened social divides. The essay proposes solutions such as progressive taxation on AI-generated wealth and international frameworks for safety standards. Amodei envisions a future where AI enables unprecedented prosperity if existential challenges are addressed proactively. He stresses the importance of ethical alignment in model development to prevent misuse. Throughout, he balances optimism about AI's transformative potential with urgent calls for governance. Balanced yet urgent tone.

Matt Shumer – "Something Big Is Happening" – Feb 10. 85mm views on X. The most widely read expressly optimistic piece. Shumer asserts that AI's exponential progress is heralding a paradigm shift, with agents and advanced models poised to redefine daily operations. He describes how scaling laws are enabling breakthroughs in multimodal capabilities, outpacing prior expectations. The essay discusses implications for industries, from automation in creative fields to enhanced decision-making tools. Shumer notes the self-reinforcing nature of hype, which attracts talent and capital to fuel further innovation. He warns of distributional challenges, where benefits may concentrate among early adopters. The piece ends with a call to embrace the change actively. Enthusiastically optimistic tone.

Citadel Securities – “The 2026 Global Intelligence Crisis” Rebuttal – Feb 25. 1mm+ on X. TIL that Citadel Securities puts out “thought pieces”. The note refutes the collapse narrative by referencing diffusion patterns of past technologies, predicting an S-curve adoption for AI. It contends that compute limitations and costs will temper rapid labor displacement. The analysis projects sustained investment in infrastructure, leading to inflationary pressures in related areas. Flight highlights augmentation over elimination in workforce dynamics. The piece integrates macroeconomic data to support gradual integration. It concludes with optimism about balanced outcomes through market forces. Methodical and counterbalancing tone.

The Kobeissi Letter – "It's Too Obvious. What If AI Doesn't Actually End The World?" (Rebuttal to Citrini) – Feb 23. 6mm view on X. The authors counter the crisis view by positing that plummeting cognitive costs will unleash widespread abundance, expanding economic frontiers. They analogize to previous tech waves where fears gave way to booms through adaptation. The essay details how AI could democratize entrepreneurship and innovation, creating new sectors. It addresses geopolitical benefits, such as reduced resource conflicts via efficiency gains. Limitations in physical and identity-based roles are noted as natural buffers. The narrative emphasizes proactive societal shifts to capture gains. Bullishly contrarian tone.

Mrinank Sharma – Resignation Letter – Feb 9. 14mm views on X. Written by Anthropic’s Head of AI Safety. Sharma announces his departure from Anthropic after two years. He reflects on his contributions to AI safety. Despite these achievements, Sharma feels compelled to move on, citing a personal reckoning with the world's interconnected crises beyond just AI, such as bioweapons and broader societal perils. He emphasizes the challenge of aligning actions with core values amid pressures to compromise, observed in himself, the organization, and society at large. Through introspection, Sharma seeks to contribute with full integrity, exploring essential life questions inspired by poets like David Whyte and Rainer Maria Rilke. Reflective and principled tone.

Sam Kriss – "Child’s Play" – Feb 18. In Harper’s Magazine. Kriss offers a critical portrait of the AI ecosystem in San Francisco, depicting entrepreneurs as driven by a mix of ambition and delusion. He satirizes the culture of "high-agency" individuals pursuing omnipotent technologies at the cost of deeper human values. The essay weaves historical references to past tech utopias that faltered, questioning AI's true contributions. Kriss examines the psychological underpinnings of the scene, from messianic visions to escapist tendencies. He critiques the commodification of intelligence and its potential to erode meaningful pursuits. Overall, it blends observation with philosophical inquiry into technology's societal role. Satirical and critical tone.

Jack Dorsey – Layoff Announcement – Feb 26. 26mm views on X. Lays off >4,000 employees out of ~10,000 total – this is across Square, CashApp, Tidal Music and a few other random businesses. The layoffs are occurring while the company is raising 2026 gross profit guidance to $12.2bn. The tweet explicitly calls out “intelligence tools” as the reason that so many people are being let go. Jack saw this as an inevitability and he could have done it slowly with multiple rounds of layoffs over months or years, or just do it all now. He chose the latter. The stock went up 20% in response, leading many to point to the prophesy of Citrini already coming true. Somber and respectful tone.

So What?

That would be a half day’s worth of reading if you went through all of those. There are some themes and main takeaways I can provide though –

Broadest points of agreement – Rapid, recursive progress in AI capabilities. Widespread white collar job displacement. Productivity boom with inequality risks. Need for adaptive policies and safeguards. Geopolitical and existential tail risks.

Biggest points of opposing views – Economic collapse vs abundance boom. Pace of disruption – exponential doom vs gradual integration. Existential risks – inevitable perils vs overhyped fears. Humanity’s role – obsolescence vs augmentation and agency.

Economic winners – Compute/infra owners. High agency entrepreneurs. High-skill niches. Nations states that lead responsibly.

Economic Losers – White collar intermediaries. Most entry level jobs. Legacy firms that resist adoption.

My Takeaway #1 – There is broad disagreement about the precise pace of disruption and the knock-on effects, but there is no doubt that significant disruption lies ahead. Whether that is 2-4-6-8-10 years out, different people feel different ways. But 10 years from now, AI/automation will have made life very different than it is today.

My Takeaway #2 – I struggle to see how (in a vacuum) this doesn’t lead to significant deflation. This is my highest conviction position when assessing the overall technological innovation outlook (not to mention deflationary demographics). It really makes me think inflation is not going to be an issue. The deflation will be the issue.

My Takeaway #3 – Deflation is the ultimate boogeyman in this debt-laden global financial system that we find ourselves in. Central bankers are terrified of even marginal deflation over even a short period of time because the entire concept of debt repayment both at the sovereign and corporate level, collapses in a deflationary environment. Bankers learned this from the Great Depression and have been terrified of it ever since. At this point, there is SO much debt in the system that deflation isn’t an option.

My Takeaway #4 – The Fed and US government will be forced into low interest rates, QE-style accommodation (eg, YCC) and increasingly more deficit spending just to juice the economy enough to keep prices flat/marginally increasing. This is what will offset the innovation-driven deflation that will be occurring in the coming years. The economy will become MUCH more productive (in terms of units of output per unit of inputs) but that won’t show up in broadly lower prices, it will just allow the government to spend more. Technology drives the real economy toward deflation. Government policy drives the nominal economy toward inflation.

My Takeaway #5 – All of this combined – the tech-driven deflation + the loose monetary and fiscal policy (to stave off deflation) – will lead to massive wealth inequality. Much worse than what we have already, which is already as bad as it’s ever been in the US. Budget deficits will grow, money printing will grow, interest rates will be accommodative, and that will benefit asset owners and in particular owners of the assets that are doing the technological innovation. This will force UBI, I am convinced of that. The only questions are how much, in what form, and how much stress will show up in the system (financial and societal) before this UBI is enacted. It seems like at least a portion of this additional UBI spend will need to be funded by increased taxes on the top 1-10% of households and the corporations that will profit most from the technological innovation.

My Takeaway #6 – Both political parties are woefully unprepared for the societal problems that will arise from this spike in wealth inequality that feels inevitable. This will open the door to more socialist politicians gaining office and enacting more policies that distribute wealth from the top 1-10% back to the bottom 50%.

My Takeaway #7 – All of this will add up to a Purpose Crisis. A large portion of the population will be rendered mostly unusable in the modern AI/automation-driven economy. These people will be on UBI and have a reasonably high quality of life (small but nice apartment; decently healthy food; nice flat screen; iPhone; fast WiFi) but will have no societally-assigned purpose (their labor is simply not needed). It’s unclear how negative the knock-on effects from the Purpose Crisis will get – substance abuse, suicide, domestic terrorism, mass riots. You could imagine a scenario where it gets really ugly (lynch the rich) and a scenario where its more subdued. I do think eventually you get to the other side of it, and people settle in to a lifestyle where they don’t have much upward mobility but they also don’t have to work and still live a pretty nice lifestyle. I think faith will play a pivotal role during this transition period. It’s part of the reason I started Things Hidden.

Market Update— Liquid Crypto Asset Investing

| Feb | Jan | YTD | Q4-25 | Q3-25 | Q2-25 | Q1-25 | 2025 | 2024 | |

|---|---|---|---|---|---|---|---|---|---|

| BTC | -15% | -10% | -23% | -23% | 6% | 30% | -12% | -6% | 121% |

| ETH | -20% | -18% | -34% | -28% | 67% | 36% | -45% | -11% | 46% |

| XRP | -16% | -11% | -25% | -35% | 27% | 7% | 0% | -12% | 238% |

| BCH* | -9% | -15% | -23% | 6% | 10% | 59% | -31% | 27% | 36% |

| EOS | -10% | -43% | -49% | -60% | -31% | -8% | -20% | -80% | -8% |

| BNB | -21% | -10% | -28% | -14% | 53% | 9% | -14% | 23% | 124% |

| XTZ | -18% | -6% | -22% | -26% | 24% | -18% | -49% | -61% | 28% |

| XLM | -12% | -10% | -21% | -44% | 51% | -10% | -20% | -39% | 157% |

| LTC | -8% | -23% | -29% | -28% | 24% | 4% | -19% | -26% | 42% |

| TRX | -2% | 1% | -1% | -15% | 19% | 17% | -6% | 12% | 136% |

| Aggregate Mkt Cap | -13% | -10% | -22% | -24% | 16% | 24% | -19% | -11% | 96% |

| Aggr Alts Mkt Cap | -6% | -17% | -22% | -24% | 34% | 25% | -34% | -16% | 72% |

SOURCE: COINMARKETCAP AND COINGECKO. AS OF 2/28/26. BCH INCLUDES SV.

We’ll start with some macro charts and then get to crypto.

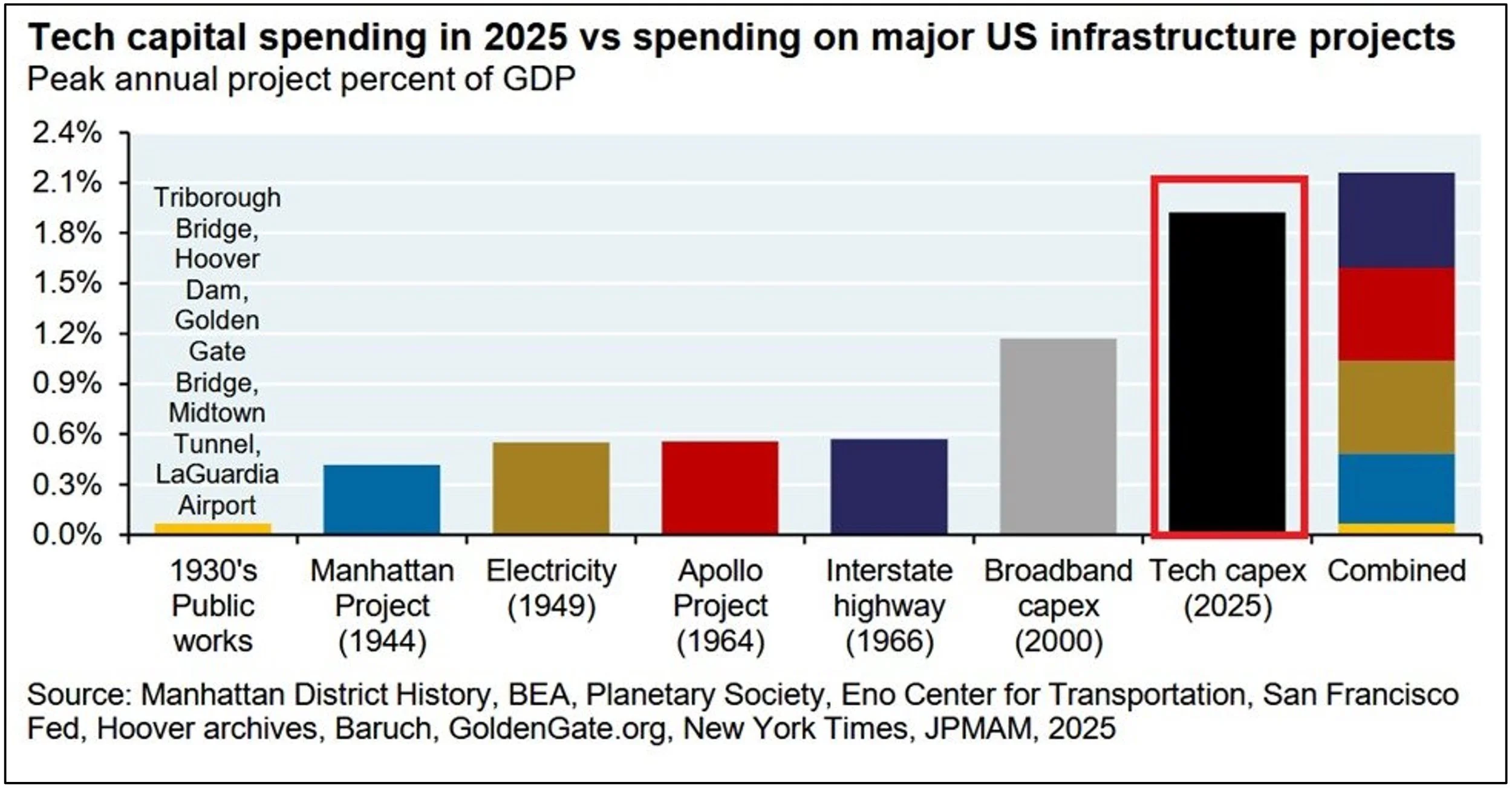

2025 tech capex was ~$450bn, already a huge number. That’s a number that’s difficult to get your head around. Here’s a chart that helps frame this 2025 capex spend, as a % of GDP, relative to other massive capex buildouts –

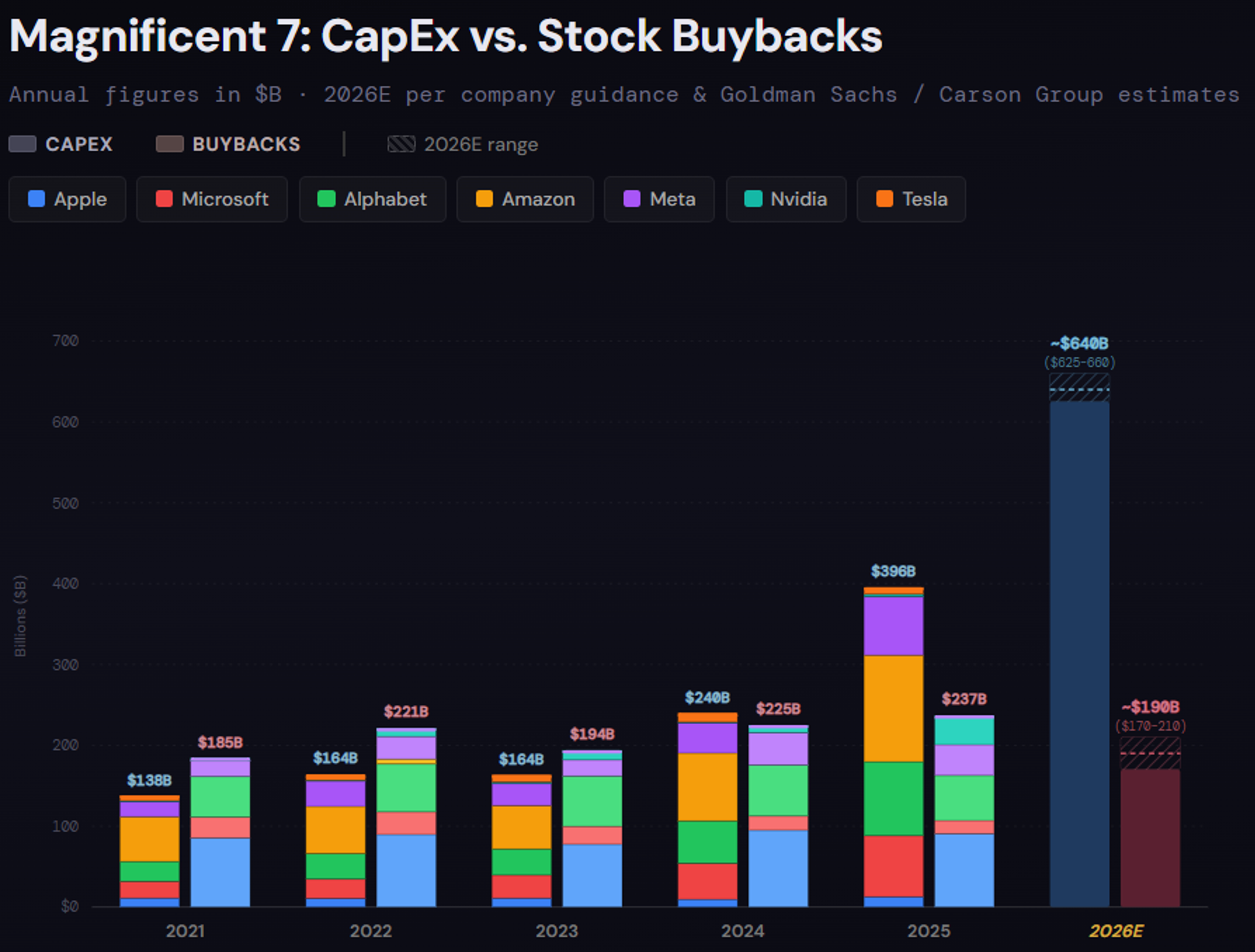

2026 tech capex is expected to be much larger. 2026 AI data center capex (mostly Mag 7) is now projected at ~$640bn. A question arises about where all this money is going to come from. One place it’s going to come from is Mag 7 stock buybacks, which have been a huge part of the market in the last few years. It looks like that trend is set to at least stall, if not reverse significantly –

Source: Claude. As of 2/26/26.

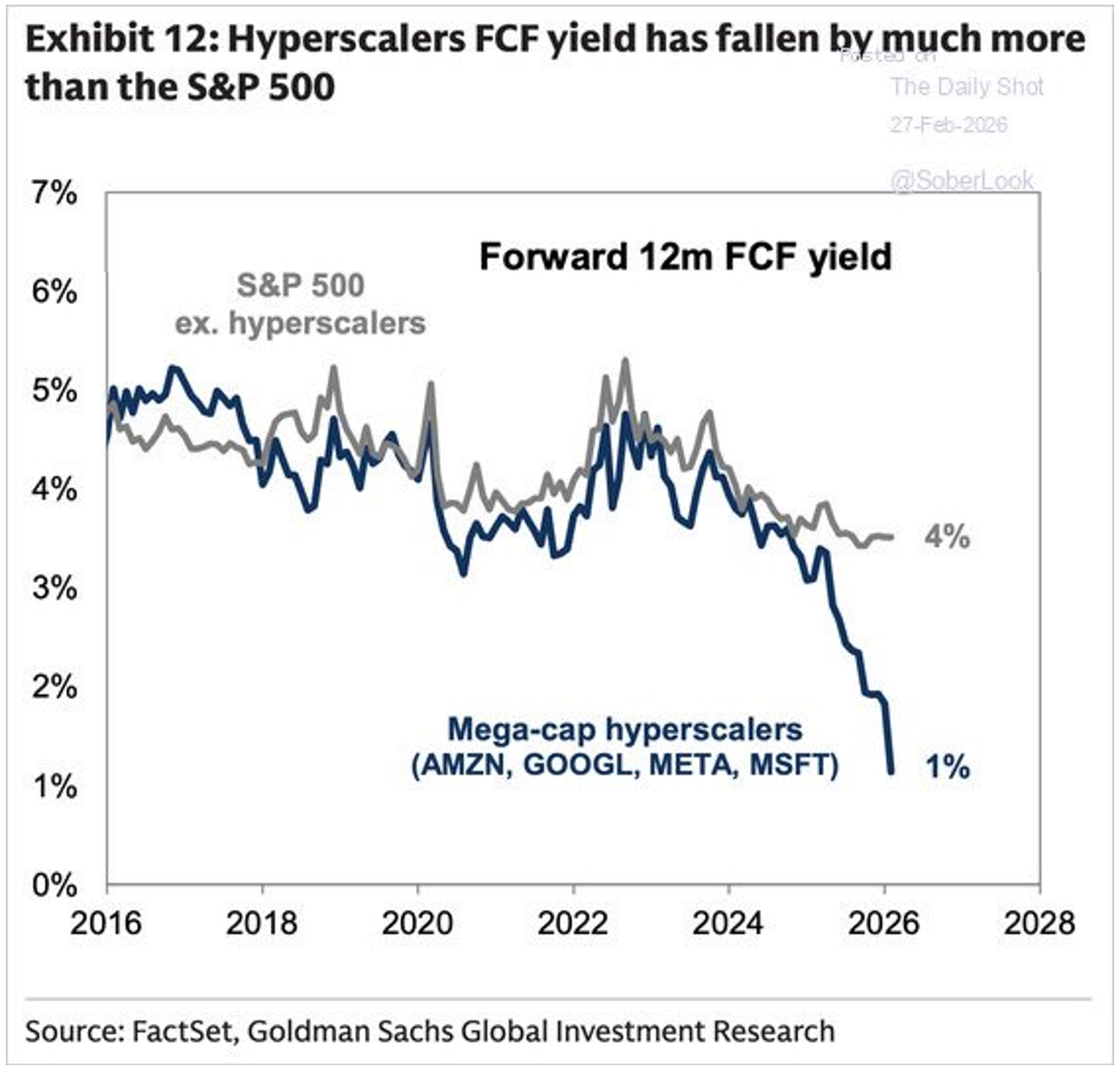

Here’s another way to look at it. Forward 12m FCF yield of hyperscalers vs the rest of the SPX –

This overall setup has the market a bit spooked about the tech sector at moment. And you’ve seen a significant rotation out tech (software especially) and into industrials and staples – atoms over bits, so the saying goes.

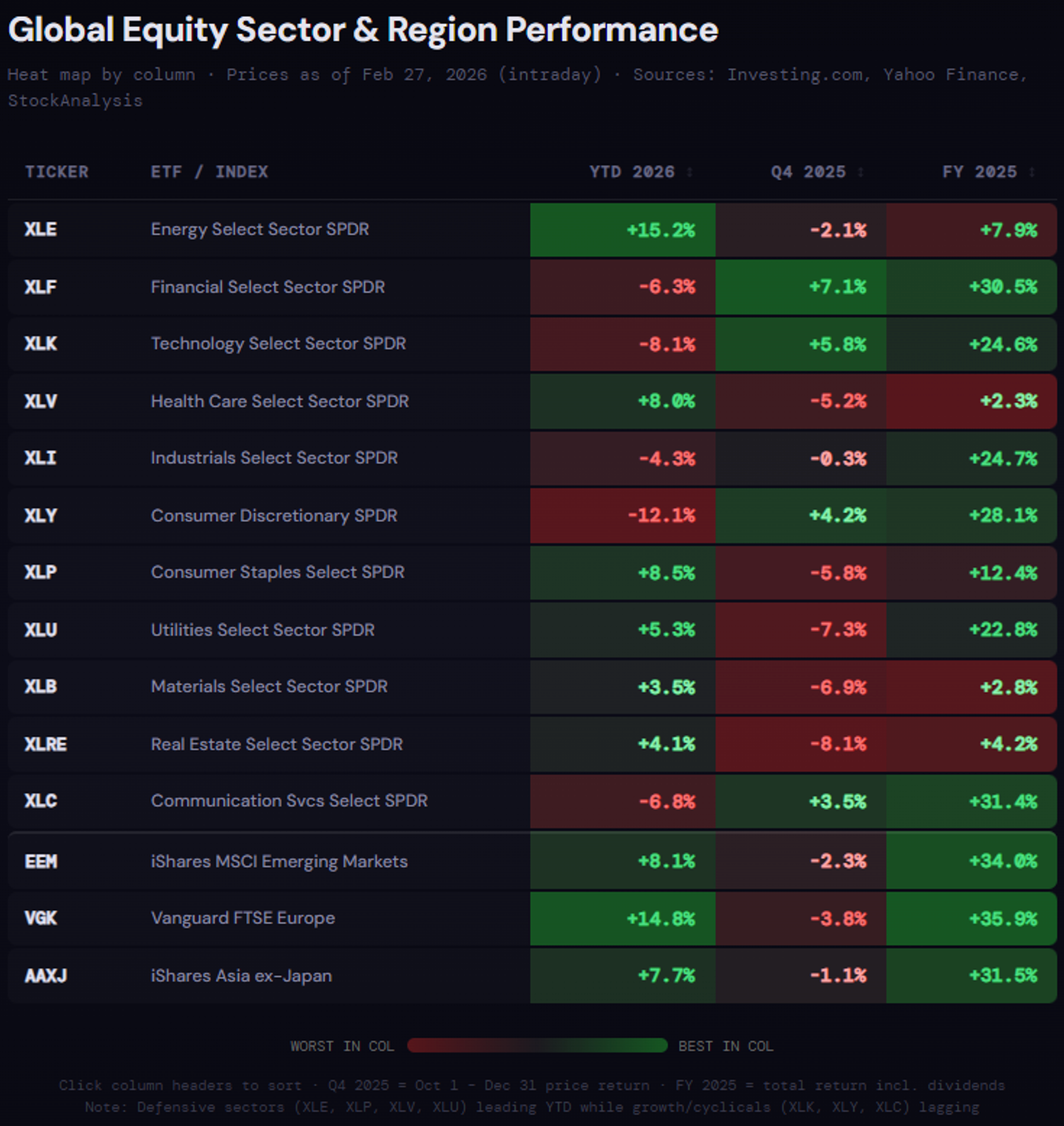

Let’s look at a table showing these rotations –

Source: Claude. As of 2/26/26.

Energy was a laggard last year, now the big winner YTD. Financials, Tech, Industrials, Consumer Discretionary, Communications – all great performers last year, lagging big YTD. Emerging markets, Europe and Asia are all outperforming YTD after great years last year.

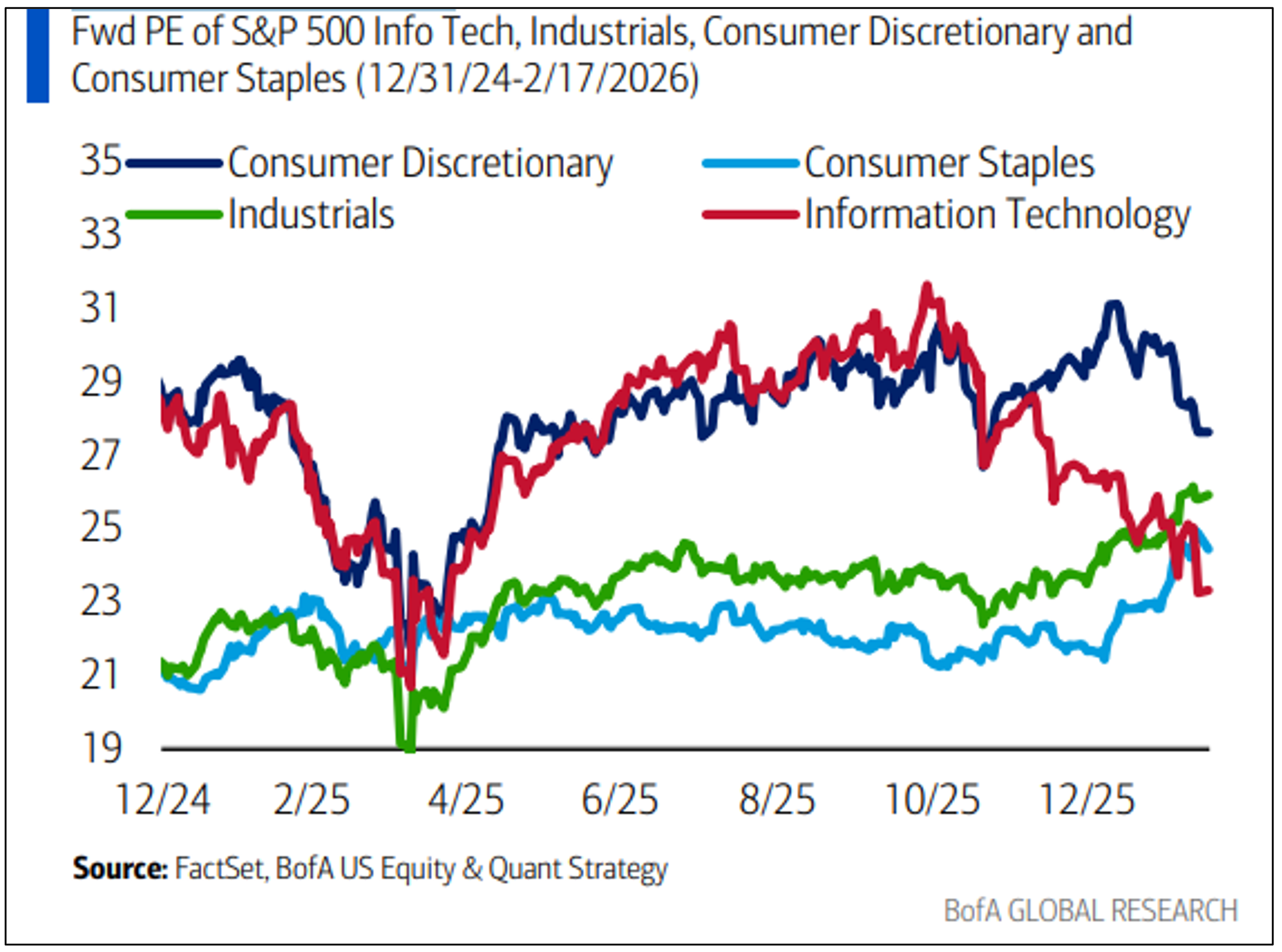

So while the major indexes are near their ATHs, there’s been plenty of rotation underneath. This rotation has led to a relative valuation that looks like this –

Industrials and Consumer Staples now trade at a higher forward PE than tech companies. Pretty crazy.

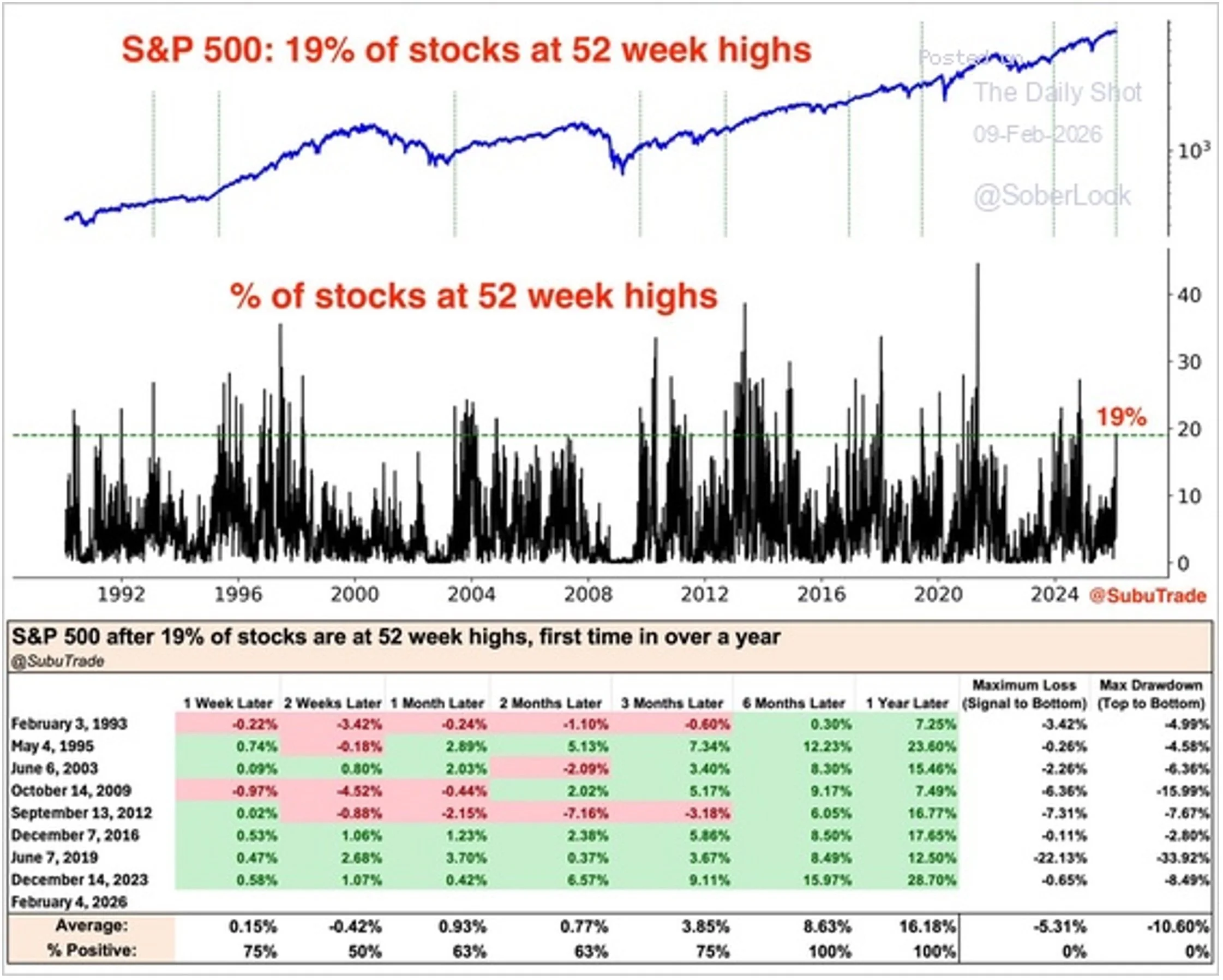

The rotation has caused a pickup in market “breadth” – a measurement of how many stocks are trending up vs trending down. There have been both bullish and bearish interpretations of this increased market breadth. Here is an interesting one –

At the bottom of that table, you can see the “% Positive” and average price change. Higher 100% of the time 6 months and 12 months out, with average gains of 9% and 16%. I like those odds.

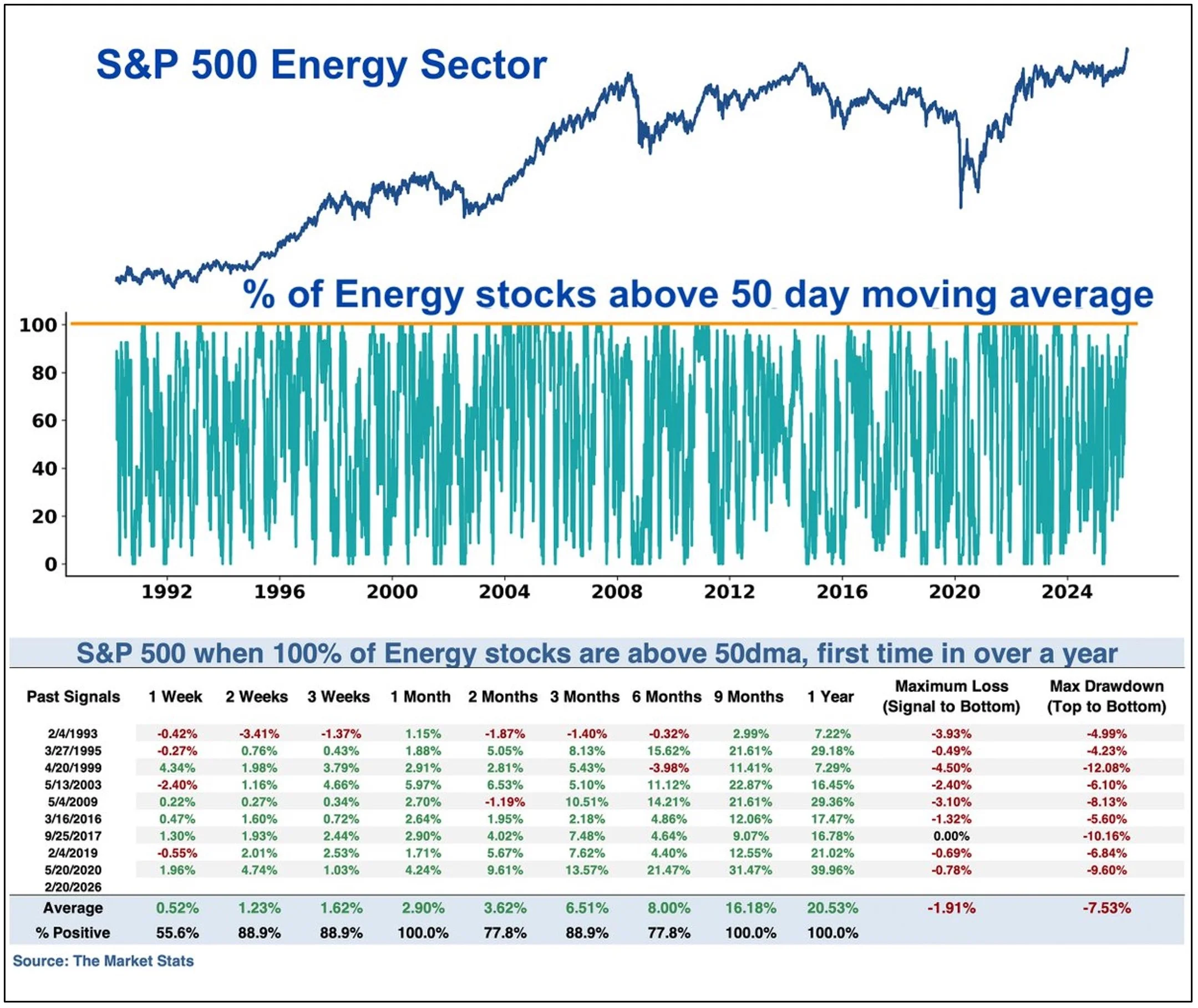

Here’s another amazing chart. This shows the periods when 100% of Energy stocks are above their 50DMA, and shows the forward price performance –

As of 2/20/26.

9 months and 12 months out, every single time, the market was higher – by an average of 16% and 21%, respectively. I like those odds.

OK. Back to tech stocks. QQQ looks like this. Many people are calling that big white circle distributive –

Source: TradingView. As of 2/26/26.

The smaller white circle on the inside is the convergence of the 50DMA and 100DMA, where it looks like price might have just been rejected. So perhaps we will go visit the 200DMA (yellow), which is only ~3% down from here.

Note on that chart above the big puke and bounce last year around tariff fears and then Liberation Day and then Trump’s reversal. So that puke very obviously blew through the 200DMA. In fact, it broke the 200DMA, retested it from below, failed and then puked hard and it was all over in about 10 days. The peak-to-trough drawdown of that whole move was 25%.

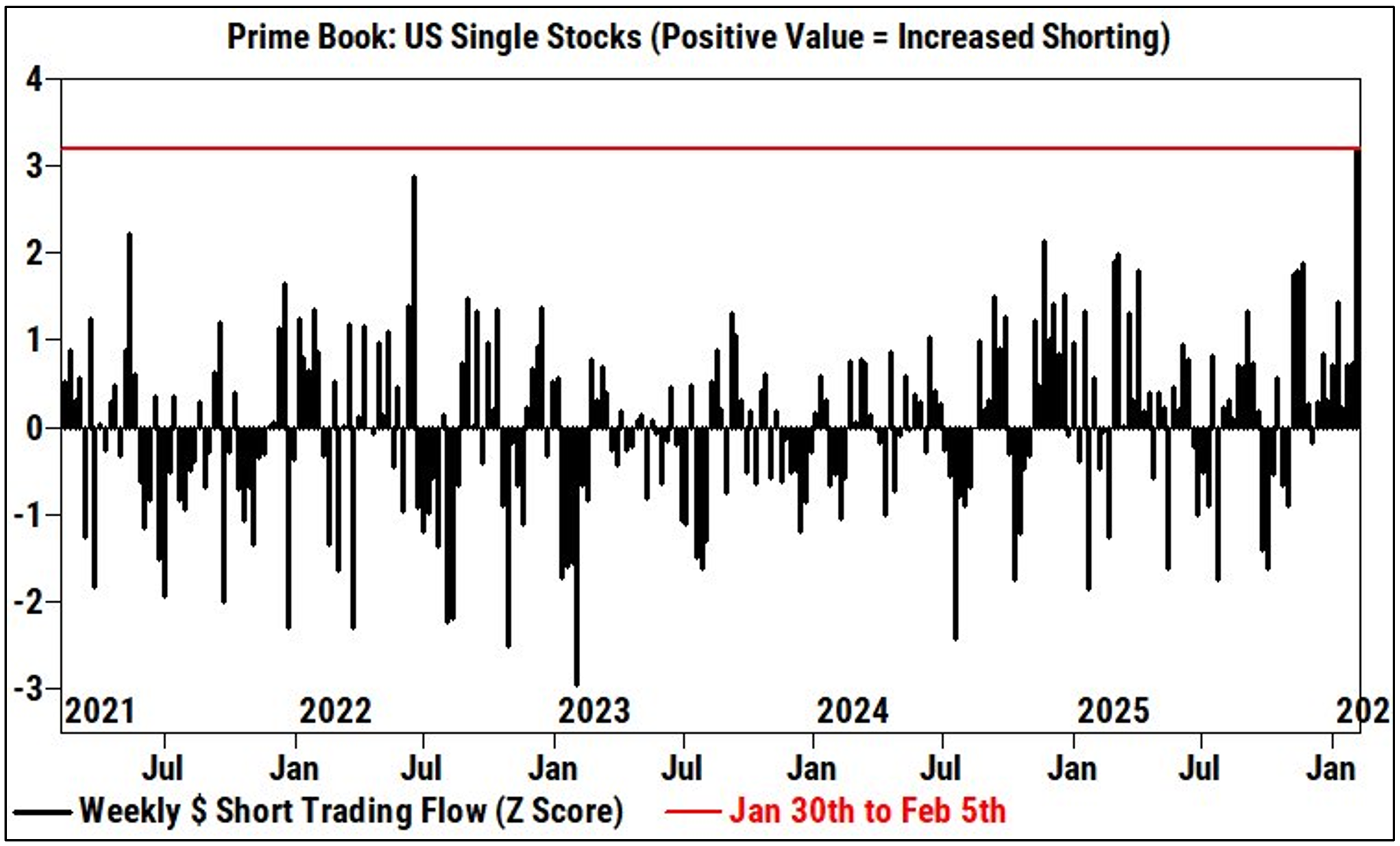

So what is on the immediate horizon that could give us a puke of that magnitude? Something that has as much fear to it as the tariffs did at the time? It seems like Iran would be the immediate pick for that. But Iran has been a very slow buildup. We’ve been watching the US military move into place for a month at this point. Iran has been front page news for over a month (year? decade? century? millennia?) now. So everyone that has wanted to hedge this event, has had time to hedge.

Case in point, the first week of Feb saw the largest weekly shorting on record from GS Prime Brokerage –

Source: @zerohedge. As of 2/6/26.

All-in, I struggle to see how an Iran conflict would cause a 25% decline in QQQ, absent something quite negative occurring unexpectedly. There’s a chance of that. Worth watching closely. Absent that, I kinda feel like we’re not going to get a down 25% in QQQ prior to the mid-terms, despite mid-term seasonality being very weak. The drawdown will probably be something shallower – down 15 or maybe 20%. Could we get some AI boogeyman? Yes. Could something crazy happen politically? Yes. There are plenty of potential boogeymen waiting around the corner. But I struggle to see that happening if it’s not Iran. And if it’s Iran, it’s probably going to happen soon.

Gold has been insanely strong –

Source: TradingView. As of 2/26/26.

You had the big blowoff top to end Jan, but the subsequent recovery has been IMPRESSIVE. You basically immediately settled back into the aggressive upward channel and kept going. Gold is an asset unlike any other. It has factors that weigh on its price in a way that no other financial instrument does. Gold has a relationship with the US dollar and treasuries that is unlike any other. We print the world reserve currency, and the price of our sovereign debt sets the price of every other asset on the planet. Gold is the mirror reflection of that. And when countries get skittish about the dollar or about treasuries (for one reason or another), they sell those assets and exchange them for gold.

BTC doesn’t have any of that. BTC has a quantum problem and it trades like absolute ass –

Source: TradingView. As of 2/26/26.

BTC price is currently sitting exactly at prior cycle ATHs which is also exactly at the pre-election price (white circles). When we were sitting here immediately after the Trump win, I don’t think anyone would have thought that 15 months later, we’d be at pre-election prices. But that’s where we are.

Overall, I think the chart looks weak. We could get a near-term bounce here because things got VERY oversold at the lows on Feb 5. But nothing about Feb 5 felt like a cyclical low to me. I think there has to be more pain eventually. Could come next month, could chop around here for a while longer. But I think we see lower prices this year.

ETH has declined 60% from its recent highs. It now sits firmly in the bottom half of its 5+ year range –

Source: TradingView. As of 2/26/26.

As with the BTC chart, this spot does not look like a cyclical low to me. We could chop a local range for a while, but I think eventually this heads down to the bottom of the overall range later this year.

ETHBTC has declined 32% from its recent highs, but still remains 62% above its cyclical lows –

Source: TradingView. As of 2/26/26.

ETHBTC also looks like a chart that is heading lower this year. Wouldn’t make much sense at all to me for this spot to be the cyclical low.

The SOL chart may look worse than the BTC or ETH charts –

Source: TradingView. As of 2/26/26.

It looks like price just fell out of a 2+ year range and is now retesting prior support from underneath. That recent price action does not look like a spring to me. It looks like it’s prob acceptance of a breakdown. Next stop $60.

I won’t spend any more time on other crypto charts. There’s nothing worth looking at. This stuff is heading lower. Maybe we get some kind of local bounce here because everything got so oversold, but I’m pretty confident we’ll see lower prices later this year.

Closing Remarks

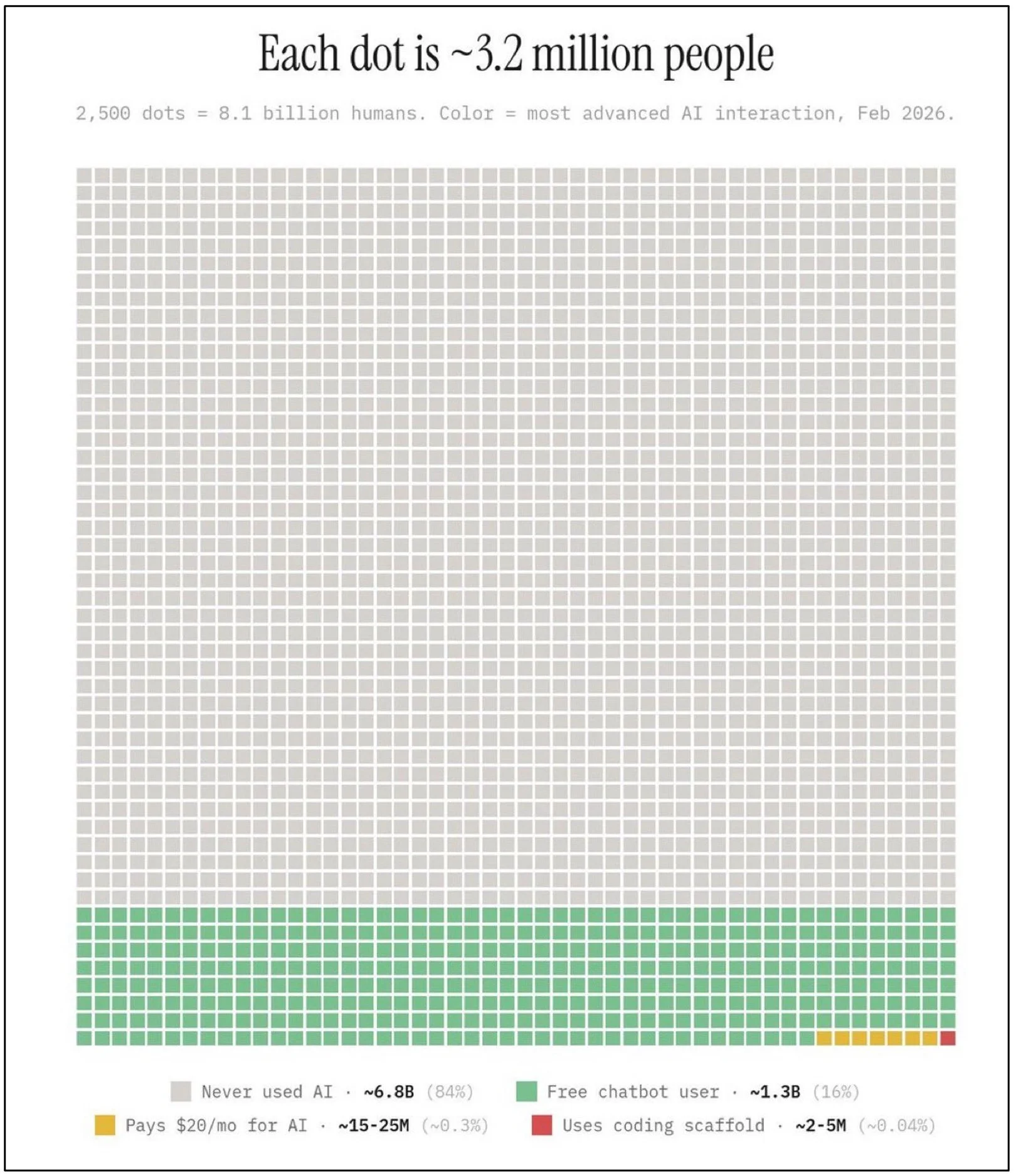

The anxiety around AI reached a new ATH in February with the release of this barrage of AI thought pieces in tandem with LLMs continuing to make rapid, significant progress. At the risk of sounding alarmist, if it feels like things are moving fast now, brace yourself. This is probably the slowest things will move ever again. Technological innovation is accelerating at an accelerating rate. This is causing commotion in financial markets and commotion in society/vibes.

And it looks like it the commotion is going to accelerate. As a reminder, this is what LLM adoption looks like currently –

Source: @damianplayer. As of 2/21/26.

So if all this commotion is already being generated by basically that lone red dot and maybe some of the yellow dots, what happens when that user base 5x’s, while the AI capability 10x’s or 100x’s or 1000x’s? That’s what has people so shook.

I would expect neither the market nor society at large to get “less shook” about AI over the course of this year and the next. This feels like a one-way train for a while. I think the market and society can and will get out over its skis on timing and scale of AI impact. We might be having some of that currently with all these thought pieces and consumer staples trading at a higher P/E than tech stocks. But I think those are short-term gyrations around a long-term trend that will almost certainly radically reshape both our lives and financial markets over the next decade or two.

I’m not sure how many people reading this right now are under the age of 25. Probably not a lot. Perhaps more that have kids in that range. I’m really not sure what I’d tell say, a 16yo contemplating college and a career path. I can imagine a world where the value of a college degree is set to decline significantly in the next couple decades. I think I would tell the 16yo that they must fully adopt LLMs and stay at the cutting edge of LLM capabilities. This will be the most formidable skill I can think of in a job market that will likely become extremely tough for entry level positions in the next decade.

I honestly feel sorry for the 16yo’s right now. For a lot of different reasons. Maybe every generation feels this way to some extent about the generations behind them. But looking at Gen Z and Gen Alpha, I feel sorry for them in terms of career stability, earnings outlook, job growth opportunities and upward mobility. When I was 16, there were clear paths that effectively solved for these important variables. You could be a doctor or a lawyer or an accountant or go into finance. By the time I was in my early 20s, big tech was a highly attractive path. If you worked hard and were reasonably smart, the economy provided you a lot of different ways to do well, and you had clarity on what the path looked like.

All of those paths are mostly out the window for today’s 16yo, or at least the clarity is out the window. There really is incredible uncertainty in career path and earnings stability, and I think that’s pretty tragic. Because I can remember back to being that age and deciding what major and career path to choose, and there was a clarity available in evaluating which direction to point your life towards. That clarity made the already massive decision less stressful in the moment. So I feel for young people these days.

That said, perhaps with hindsight, the history books will look sympathetically upon Millennials as the last generation that actually had to work their whole lives, before AI/robotics came and did away with the majority of human labor requirements. So maybe the joke is on us!

“Proof rather than argument.”

-Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2023 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS